Analysis

July 18, 2024

Final thoughts

Written by Michael Cowden

I thought we’d have more clarity this week on Section 232, Mexico, and a potential carve-out for steel melted and poured in Brazil.

As of right now, the only official comment I have is from the Office of the United States Trade Representative (USTR).

Section 232, Mexico, and the White House

USTR referred me to the White House press office, which had not responded to me as of Thursday afternoon when I filed this article. Given recent headlines, I am guessing the White House might be a little busy with other things.

I also reached out to the Commerce Department and US Customs and Border Protection (CBP). I haven’t heard back from them, either.

I should add here that it’s highly unusual for USTR to refer a wonky question about steel tariffs to the White House. It reminds me a little bit of my experience covering the early, chaotic days of Section 232 back in 2018.

Remember? Former President Trump sometimes made what turned out to be official policy via Twitter (now X). Given that it’s summer, my mind goes back to the surprise doubling of tariffs on Turkey to 50% on a random Friday morning in August 2018. I then had to backtrack to see whether that was indeed US policy. (It turned out it was.)

Still, I’d be shocked to see President Biden making policy on X. And lately when I call on folks familiar with DC developments, they’re sometimes less interested in 232 than in whether Biden will continue his campaign for re-election.

To assess that latter question, I turned to a trusted source. Namely, gambling markets. Sure enough, current odds are that Biden will not stand for re-election and that Vice President Kamala Harris will become the Democratic nominee.

We’ll see… . I can also remember when consensus among steel market participants was that Nippon Steel’s acquisition of U.S. Steel would close with no major hurdles. Reality had other plans.

I wish I had a gambling market with enough liquidity to quantify what the outcome of this Section 232 business with Mexico and Brazil might be.

As it stands, each side appears confident that it will prevail, or has already. One side might point that out there has been no carve-out for Brazil mentioned in the Federal Register, the official source of US policy. And the White House has also told some sources familiar with the matter that no such agreement has been made.

The other side might say that this is all a “nothing burger,” that discussions are ongoing, and that when the dust settles, trade with Mexico will proceed as normal.

How did Mexico end up announcing a policy that, as far as I know, has not been corroborated by the US? Was there a misunderstanding at the negotiating table? Did the US agree to a policy it is now trying to back itself out of? Does it come down to the exemption process?

How much posturing, double-crossing and triple-crossing might there be before we know the answer? It’s the stuff of a telenovela, albeit one of interest almost exclusively to steel nerds. (Pro tip: Don’t tell your family you can’t go to XYZ because you’re working on something about Section 232. It will only result in the doubling or tripling of items on your to-do list.)

Price floor

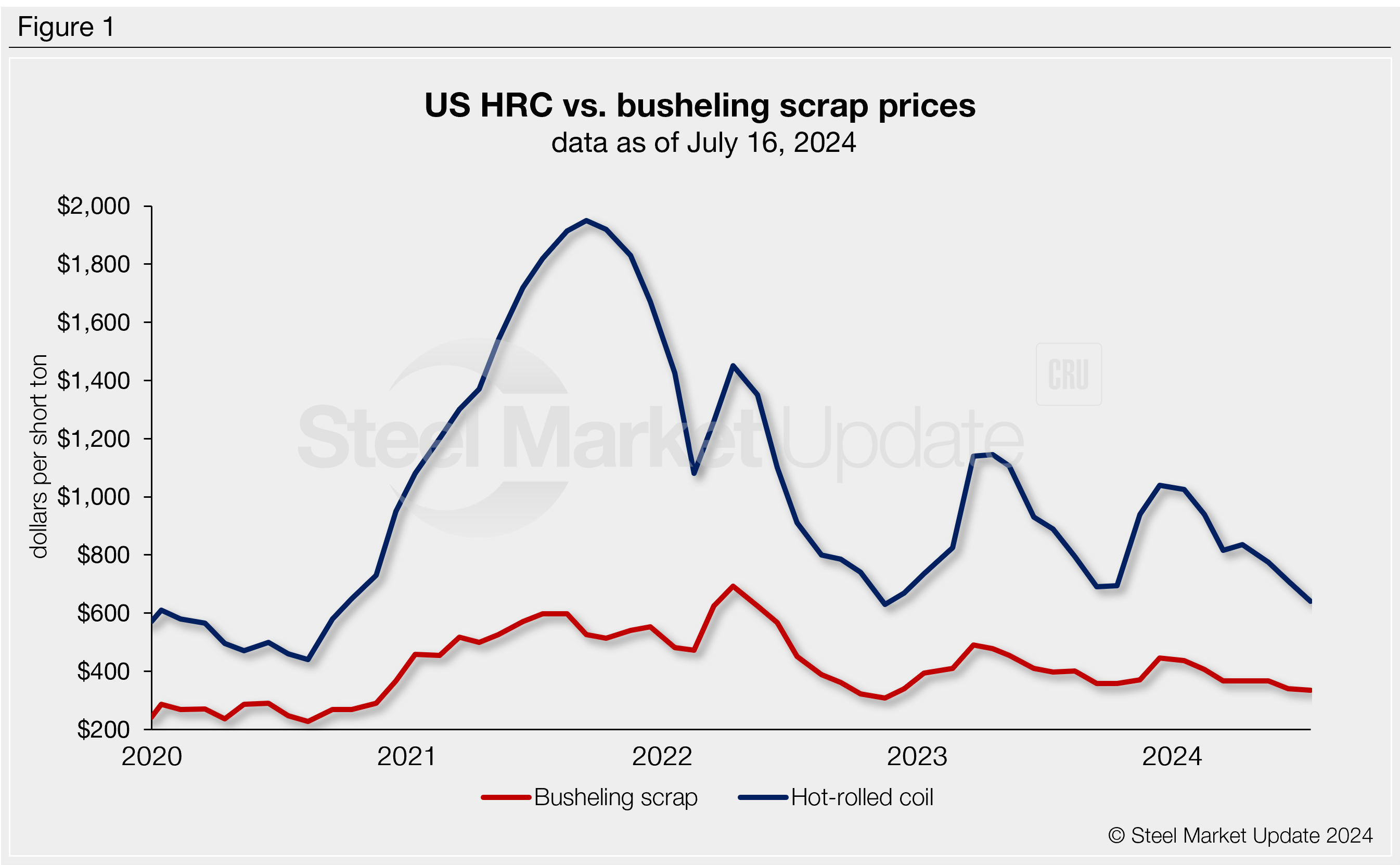

Let’s in the meantime touch on something closer to home. Have US hot-rolled (HR) coil prices finally found a floor?

Ethan Bernard wrote a good analysis of the tightening spread between HRC and scrap yesterday. That spread is the lowest it’s been since August 2020.

Note that everything in that chart is displayed in short tons (i.e., we converted gross tons, which scrap is usually priced in, to short tons).

When spreads got tight last September, we saw price increases. Ditto in November 2022, per our price announcement calendar. (If you want to pull the numbers yourself, check out our interactive pricing tool – which allows you to compare finished steel and scrap prices in a common unit of measure.)

Another potential sign of a bottom: as David Schollaert notes, the spread between US HR prices and those abroad has inverted. That has been a reliable sign of a sheet price floor in the past.

And as Brett Linton reports today, lead times for sheet products appear to have stabilized at low levels. So perhaps the declining trend that we saw for most of the second quarter has ended.

Meanwhile, SDI Chairman and CEO Mark Millett makes a convincing case on why the market should improve from here on out. (If I have any quibbles there it’s that Millett almost always has a convincing case on why that’s so.)

Or trap door?

But I don’t know that the case for a price floor (let alone an increase) is a slam dunk. According to the research of Estelle Tran, prices lead at CRU, service center inventories remain elevated. That information is available to our premium-level subscribers.

And we continue to hear mounting concerns about demand from many of you. In fact, 39% of respondents to our most recent steel market survey said they would not meet forecast his month. That’s the highest it’s been since we started consistently asking that question in January 2022. (Editor’s note: We’ll release full survey results to our premium members on Friday. If you’re interested in upgrading to premium, contact us at info@steelmarketupdate.com.)

Did I mention that things look bleak in plate? Lead times there continue to slide along with prices. Why is that, and what might it take to get US plate mills running at higher capacity utilization rates?

SMU Steel Summit

It’s against a backdrop of unprecedented – that word again – political developments that we’ll meet in August at Steel Summit. An assassination attempt on former President Trump. Questions around Biden’s re-election bid. The inevitable partisanship that comes in the final months of a presidential campaign.

We want you all to know that we welcome you all. To paraphrase Teamsters union President Sean O’Brien at the Republican convention earlier this week in Milwaukee, it doesn’t matter if you’re a D, an R, or an I. I think what he forgot to add is that’s because we’re all in this same bucket, like DRI in an EAF – coming together to make better steel.

Seriously, though, I look forward to seeing you all – more than 1,000 and counting – at the Georgia International Convention Center (GICC) in Atlanta. I also look forward to having a respectful discussion around issues of interest to an industry we all care deeply about.

You can find the latest agenda here and register here.

Your moment of chicken

Amid all of these serious developments, I wanted to leave you with a “moment of zen” – a long-running feature on The Daily Show.

But since that’s probably been trademarked, the SMU staff suggested that I leave you with something I hope you’ll find peaceful and cute in equal measures.

Namely, the newest addition to Brett’s family, these chicks. Did you know that chicks can be delivered by the US Postal Service?

And so there you have it, my friends, your “moment of chicken.” We appreciate you, all of you, for your continued support of SMU. And we can’t wait to see you next month in Atlanta.