Market Data

February 25, 2025

SMU price ranges: The steel rocket ship continues to soar higher

Written by Brett Linton & Michael Cowden

Market participants might disagree over how high flat-rolled steel prices might go and how long they might remain elevated.

But they are in near total agreement on one thing: Prices are up sharply again this week.

The gains come on the heels of waves of mill price increases (for sheet and for plate), expectations that scrap prices will rise again in March, and the threat of tariffs looming over the market.

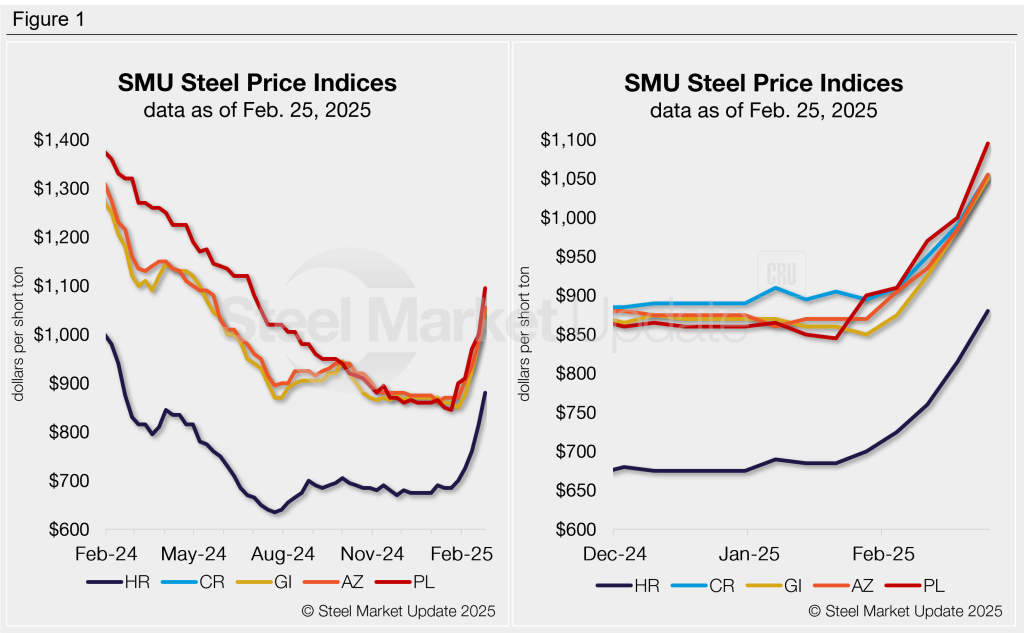

By the numbers

SMU’s price for hot-rolled (HR) coil now stands at $880 per short ton (st) on average. That’s up $65/st from last week and nearly $200/st from a month ago. (Put another way, HR prices are up 28% from $685/st on Inauguration Day.)

Our cold-rolled coil price, meanwhile, stands at $1,055 st on average, and our coated base price is at $1,050/st on average. Both are up $65/st from last week. Galvalume base prices average $1,055/st, up $70/st from a week ago.

Gains on the plate side were even sharper. SMU assessed plate prices at $1,095/st on average, up $95/st from last week.

All our price momentum indicators continue to point higher, meaning we expect prices to continue to rise.

Sticker shock

Unless there is another last-minute reprieve, blanket tariffs of 25% on Canada and Mexico could go into effect on March 4. Sources were mixed on whether that would happen.

But there was a consensus that Section 232 tariffs of 25% on imported steel – given that they are a known commodity – would be enacted as planned on March 12.

On the coated side, meanwhile, preliminary anti-dumping duties are expected to be released by the Commerce Department on April 3. Coated demand, which had been served in large part by imports, is now flowing into domestic mills, market participants said.

And those same US mills are trying to re-establish a roughly $200/st spread between hot-rolled and tandem products. That spread had compressed as HR initially rocketed higher than tandem products. Sharply higher offer prices this week have given some buyers “sticker shock,” sources said.

But for how long?

There is disagreement about how long prices might continue to rise.

Some market participants think that imports could flood in should US prices get too high above those in the rest of the world. That’s especially true with the brakes previously provided by Section 232 quotas now gone.

Some folks in that camp also worry that sheet inventories – which were already high – could become even more bloated by the recent buying frenzy. They might also note that mills could fall afoul of the Trump administration if steel prices are seen as spurring inflation and idled capacity is not restarted.

Others, however, think the administration has domestic steel’s back. They reason that any spike in import licenses could result in Section 232 tariffs going from 25% to 50%. And even the possibility of that happening – combined with Trump’s unpredictability – should keep imports in check, they said.

There are also debates about demand. While most agree that the year is off to a good start, some caution that pricing gains have outstripped improvements in demand.

Refer to Table 1 below for the latest SMU steel price indices and how prices have trended in recent weeks.

Hot-rolled coil

The SMU price range is $840-920/st, averaging $880/st FOB mill, east of the Rockies. The lower end of our range is up $60/st w/w, while the top end is up $70/st w/w. Our overall average is up $65/st w/w. Our price momentum indicator for hot-rolled steel remains at higher, meaning we expect prices to increase over the next 30 days.

Hot rolled lead times range from 4-8 weeks, averaging 5.5 weeks as of our Feb. 19 market survey.

Cold-rolled coil

The SMU price range is $1,010–1,100/st, averaging $1,055/st FOB mill, east of the Rockies. The lower end of our range is up $80/st w/w, while the top end is up $50/st w/w. Our overall average is up $65/st w/w. Our price momentum indicator for cold-rolled steel remains pointing higher, meaning we expect prices to increase over the next 30 days.

Cold rolled lead times range from 6-9 weeks, averaging 7.1 weeks through our latest survey.

Galvanized coil

The SMU price range is $1,000–1,100/st, averaging $1,050/st FOB mill, east of the Rockies. The lower end of our range is up $80/st w/w, and the top end is up $50/st w/w. Our overall average is up $65/st w/w. Our price momentum indicator for galvanized steel remains pointing higher, meaning we expect prices to increase over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,097–1,197/st, averaging $1,147/st FOB mill, east of the Rockies.

Galvanized lead times range from 6-9 weeks, averaging 7.3 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,010–1,100/st, averaging $1,055/st FOB mill, east of the Rockies. Our entire range increased by $70/st w/w. Our price momentum indicator for Galvalume steel remains higher, meaning we expect prices to increase over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,304–1,394/st, averaging $1,349/st FOB mill, east of the Rockies.

Galvalume lead times range from 7-8 weeks, averaging 7.3 weeks through our latest survey.

Plate

The SMU price range is $990–1,200/st, averaging $1,095/st FOB mill. The lower end of our range is up $40/st w/w, while the top end is up $150/st w/w. Our overall average is up $95/st w/w. Our price momentum indicator for plate remains at higher, meaning we expect prices to increase over the next 30 days.

Plate lead times range from 3-8 weeks, averaging 5.1 weeks through our latest survey.

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton