CRU

May 31, 2024

CRU: Sheet price stability seen in most regions outside of the US

Written by Ryan McKinley

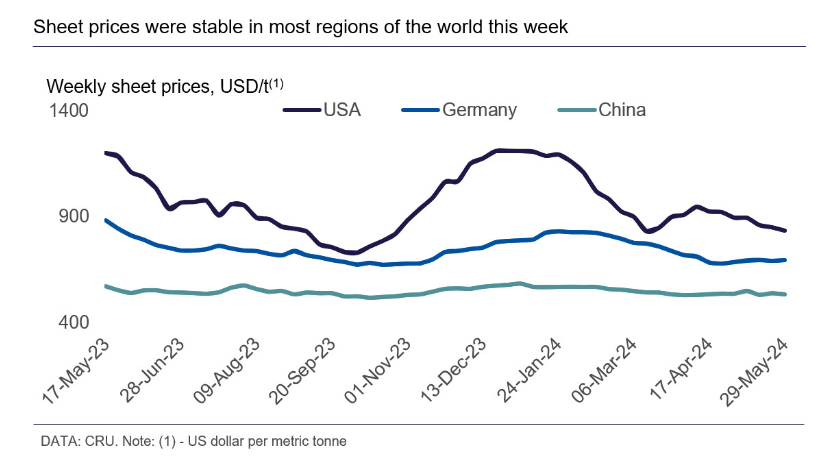

Steel sheet prices across most regions of the world were little changed this week.

European buyers remain cautious regarding their outlook towards end-use demand and largely remained out of the market. A similar trend was seen across Asia, although skepticism on real estate stimulus measures in China led to w/w price falls. In the US, relatively weak end-use demand in combination with plentiful supply have led to a seventh straight week of price falls.

USA

US HR coil prices have now declined for seven straight weeks after falling by $14 per short ton (st) this week to $758/st. Submitted volumes fell this week, and the price range narrowed on both the high and low ends. Value-added product prices were also down, with CR coil and HDG coil (base) prices falling by $18/st and $30/st to $1,099/st and $1,032/st, respectively.

End-use demand is not particularly strong, while supply is in a visible surplus. This surplus comes from rising capacity at domestic mills while import arrivals remain high. Due to limited demand growth, service centers are also trying to destock, leaving mills to become more aggressive in placing tons, often cutting deals much lower than their public offers.

Meanwhile, overseas shipping delays mean that imports are still arriving at a relatively high level for May, with total volumes looking like they will be near those reached in March and April. Market participants also report that this imbalance between supply and demand is forcing some mills located in the Midwest to target markets further afield, like the West Coast, to fill in order books.

Europe

European sheet prices remained rangebound this week due to a lack of trading activity and weak demand. German and Italian HR coil were assessed at €640 per metric ton (mt) and €648/mt, up €4/mt and down €2/mt, respectively.

Buyers are cautious about how much material they want to order due to doubts over end-use demand in the coming months. Current European lead times are short at around one month for Italian HR coil and 5–6 weeks for German HR coil.

Interest in imports from Asia remained low due to safeguard-related risks and long lead times. This week, HR coil import offers from Japan were quoted at $600-630/mt CFR, while Japanese CR coil was heard to be offered at $720–730/mt CFR. These offers would be for July–August shipment, and arrival in September–October.

China

Domestic Chinese sheet prices fell slightly this week, with the most significant price decrease occurring for HR coil. The general market optimism on real estate stimulus has faded, leading to a downward correction in HR coil futures prices. The knock-on effect in the spot market was then felt this week, with 3mm HR coil falling by RMB30/mt w/w. This, together with steady steelmaking raw materials prices, caused a decrease in mill margins for HR coil. However, steel mill operating rates remain elevated. Underlying demand for downstream sheet products remains healthy, given a continuous strengthening in auto and home appliance sales. Increased purchases for downstream products over the past two weeks also led to a slight w/w fall in sheet inventories.

Asia

Prices of imported sheet products in Asia were either stable or rose slightly over the last week.

Several deals of HR coil SAE1006 rerolling material were heard to have been concluded at $555-560/mt CFR Vietnam. According to market contacts, the total volume sold by Hoa Phat and Formosa to their domestic customers were ~300,000 mt for July shipments. Therefore, unmet demand will have to come from imports, and Chinese material remains the most competitive for now.

A Japanese mill was also heard to have sold 30,000 mt of HR coil rerolling grade at $580/mt CFR Vietnam for June shipment, while offers for July shipments were heard at $600/mt CFR Vietnam.

CRU assessed HR coil at $560/mt CFR Far East, flat w/w. CR coil and HDG coil prices were up by $10/mt w/w to $700/mt and $720/mt, respectively.

India

Indian sheet prices rose slightly by INR200–400 ($2–5)/mt w/w on the back of reduced supply due to recent maintenance shutdowns and higher input costs. Real demand is still modest in India due to a heatwave that has impacted construction activity. Also, most buyers continued to withhold fresh purchases until the elections conclude next week. Meanwhile, spot iron ore prices rose over the past couple of weeks and steelmakers attempted to pass through this cost rise to customers.

Most market participants believe that a revival of pent-up demand from next week on will provide some support to sheet prices in the coming weeks, but the upside will be limited by both low demand during the monsoon season and continued import arrivals. An upside risk to near-term sheet prices is an upswing in export sales, particularly to the EU.

To learn more about CRU’s services, visit www.crugroup.com.