CRU

February 12, 2025

CRU: US steel prices to jump on new Trump tariffs

Written by Josh Spoores

President Trump has announced he is reinstating the full Section 232 (S232) tariffs on steel. This places 25% tariffs on all steel imports starting from March 12, without any exceptions by country or company. These tariffs are additive to any prior tariffs, such as current antidumping or countervailing duties.

Tariffs will provide renewed support to US-based producers

If these new tariffs come on in full without any country or company-specific exclusions, the price of imported steel will quickly increase to reflect a portion – if not all – of the new 25% tariffs. In the US domestic markets, imports are often the marginal source of supply, so higher-priced imports will set the domestic price of finished steel.

For example, US Midwest HR coil steel is an industry benchmark of steel prices. CRU’s US Midwest HR coil price was assessed at $728 per short ton (st) on Feb. 5 before these tariffs were introduced. A straight 25% increase on this price would lead to a realized mill price of $910/st.

Prices rose the last time Trump initiated widespread tariffs

In March 2018, President Trump announced and implemented new 25% tariffs under Section 232 of the Trade Expansion Act of 1962. These tariffs initially provided some exclusions for key trading partners, and they came about when steel-intensive demand was nearing a cyclical peak

At that time, CRU’s US Midwest HR coil price rose from $661/st in January 2018 to a high of $918/st by July 2018. Prices were initially supported by significantly higher-priced imports as well as increased orders from buyers as they worked to get ahead of future price increases. However, prices then fell back as underlying demand slowed seasonally and exclusions were granted to key trading partners such as Canada and Mexico, as well as for product-specific requests for some manufacturers.

Support for US mills is more than just higher prices

With the implementation of the S232 tariffs as well as the post-pandemic lockdown period where mills earned extraordinary profits, the US has become a primary location for new steel investment.

CRU is tracking approximately 4.6 million metric tons (mt) of new capacity for long products coming online between 2024 and 2026. Sheet products will see an additional 4.5 million mt of new production over that same period with another 3.5 million mt added in 2027-28. For both longs and sheet products, the largest year of new capacity is 2025 where a total of nearly 5 million mt of sheet and longs will be available to run.

These tariffs are very well-timed as they will provide steel mills the ability to effectively ramp up this new production at historically high prices, relative to costs.

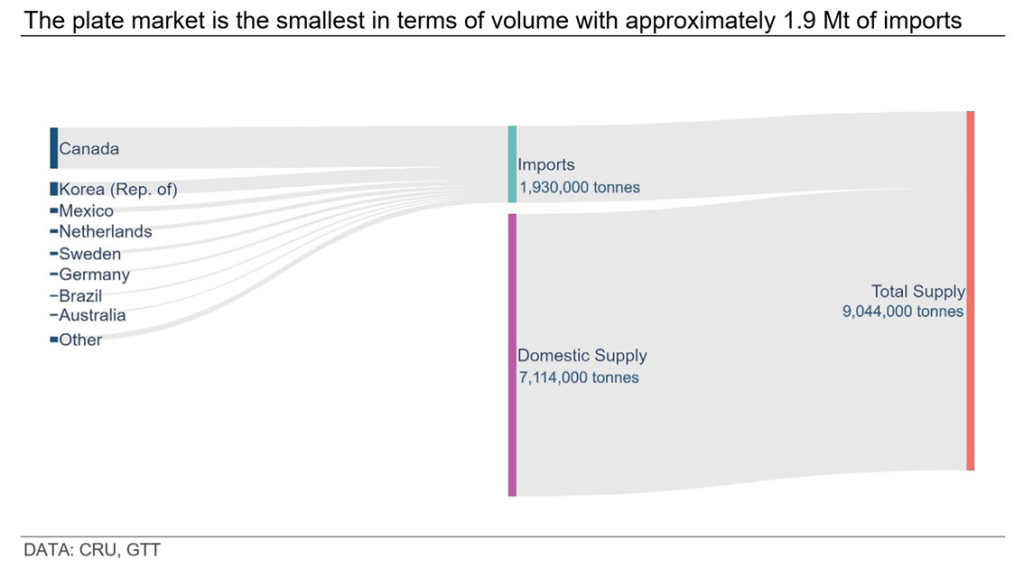

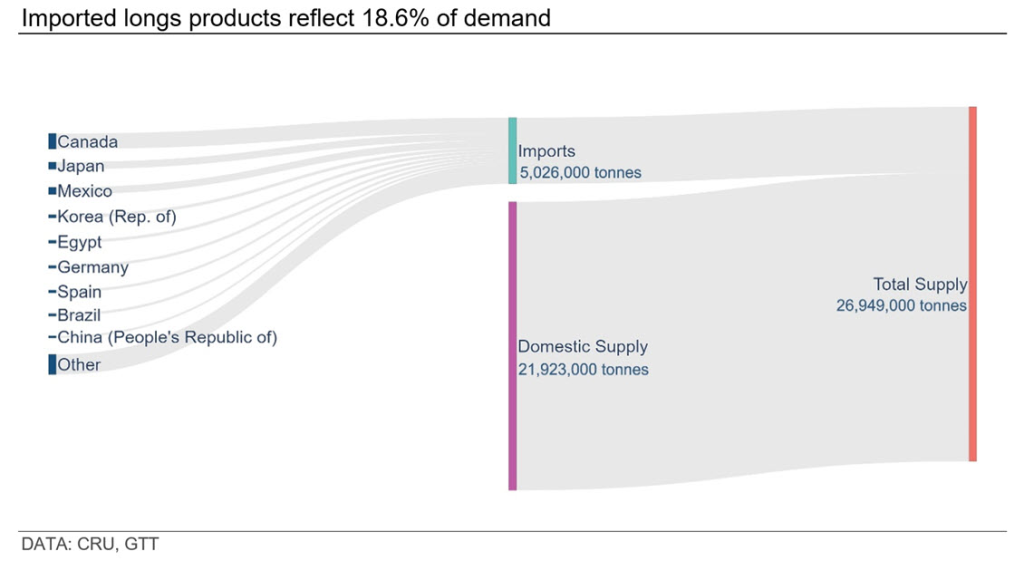

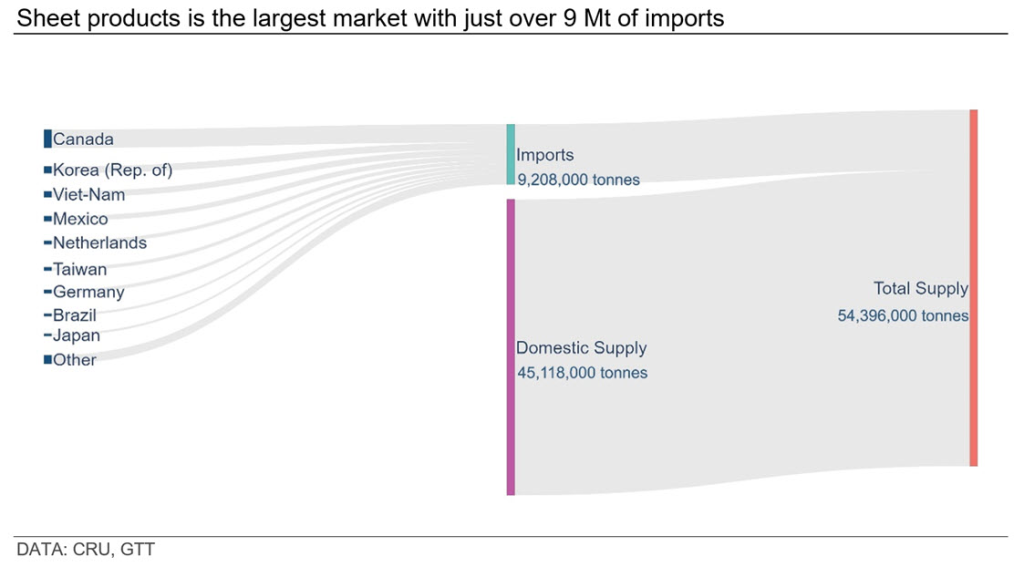

Tariffs target approximately 16 million mt of steel imports

While new capacity continues to be built and ramped up, the US steel market has long required imports to satisfy demand. Today, the US is a net importer of approximately 16 million mt split across plate, longs, and sheet markets. The shares of imports for all three markets are near 20% of overall demand. Plus, while new capacity is being built and ramped up, all three markets will continue to require imports to fully satisfy demand.

Tariffs may lose some pricing power as trading partners retaliate and some demand destruction emerges

We continue to see new tariffs in the US market as either supportive of new foreign investment or as leverage for trade negotiations. Due to this, we expect that some trading partners will negotiate with the US to lower or eliminate these new tariffs. These negotiations will likely come about alongside targeted retaliation.

We also expect that if these tariffs remain in place, some demand destruction will also be seen. While these tariffs are only for steel products, some manufacturers may elect to offshore metal-intensive manufacturing and export manufacturing parts or finished products to the US instead of paying 25% more for their steel. There also may be some manufacturers that opt to look at substitute materials. Yet, these options of offshoring and product substitution are not available to all steel buyers, thus the effect of this on overall demand may be minimal.

Expect higher steel prices in the US market

These new tariffs have been announced and are expected to be implemented quickly. Due to this timing, supply chains have limited options in the very near term to manage these increased prices or change sourcing. Therefore, as long as these tariffs come online with minimal exclusions, we expect that domestic steel prices in the US market will be set by an import product with applicable tariffs and shipping costs. In most cases, this will be a North American-sourced product.

This was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com. Have any questions? Reach out to the author at josh.spoores@crugroup.com.