Market Data

January 28, 2025

SMU price ranges: HR, plate rise as momentum builds, coated stuck in neutral

Written by Brett Linton & Michael Cowden

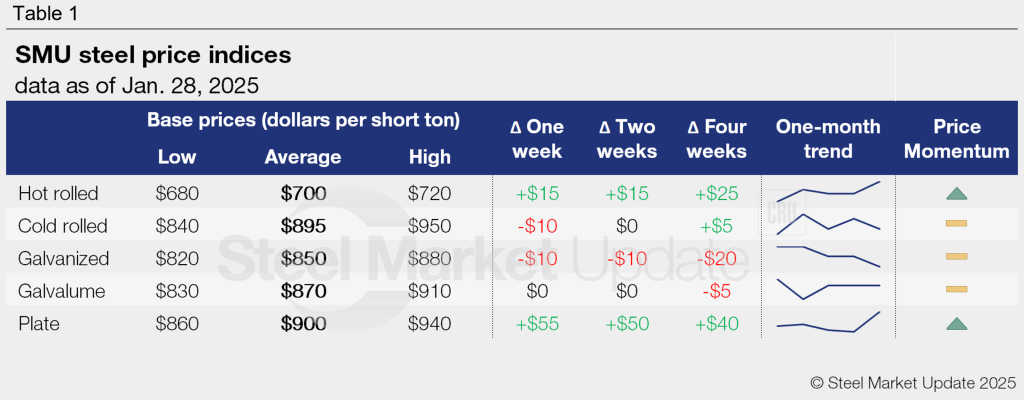

SMU’s sheet prices were mixed this week. Hot-rolled (HR) coil and plate notched gains while prices for coated products stagnated or dipped lower.

Our HR price now stands at $700 per short ton (st) on average, up $15/st from last week and marking the highest level for HR prices since $705/st in early October.

SMU’s plate price is at $900/st on average, up $55/st from last week. That marks the highest level for plate prices since late October. It also marks the sharpest week-over-week (w/w) gain for plate since December 2023, according to our pricing archives.

We saw no such momentum in tandem products. SMU’s cold-rolled (CR) coil assessment slipped to $895/st, down $10/st from last week. Our galvanized base price dropped $10/st to $850/st, while our Galvalume base price was unchanged at $860/st.

SMU has adjusted its HR and plate momentum indicators to “higher.” Note that our HR momentum indicator was at higher for only 42 days in 2024. Most of that occurred in August, when US mills made a concerted push to end a July price swoon. Our CR and coated momentum indicators remain at neutral.

Market commentary

HR prices gained on higher scrap prices in January and expectations of additional gains in February. Bullishness around scrap has increased thanks to a severe cold snap last week that has hindered collection. A modest sheet price increase by Nucor (up $10/st) also helped.

Market participants said HR was in addition benefiting from increased demand and longer lead times at several mills. They said that was being driven in part by increased demand for energy tubulars such as oil country tubular goods (OCTG).

Speculation about trade action – whether it be tariffs or changes to Section 232 – might be playing into it as well, some said. One example: Certain sources speculated that South Korea might lose its Section 232 quota and find its products subject to the 25% tariff that other nations face. That matters because South Korea is one of the largest foreign steel suppliers to the US, especially when it comes to HR, plate, and OCTG.

Plate prices benefited from the same factors as HR and from a substantial price increase ($60/st) that was initiated by Nucor and followed by other mills. Plate’s sharp gain might also result from plate inventories being significantly lower than those for sheet.

Prices for coated products should in theory have benefited from the same as HR factors. And they could see a lift from upcoming preliminary duties in the trade case targeting 10 nations. Preliminary countervailing margins are anticipated Feb. 3 and preliminary anti-dumping margins on April 3.

But some market participants said that imports that arrived late in Q4 continued to weigh down the coated market. And the construction sector – a key end market for coated material – continues to be held back by high interest rates.

Opinion was mixed on whether tariffs or an overhaul of Section 232 might ride to the rescue for coated flat-rolled steel, where a glut of new domestic capacity – and low pricing from certain domestic mills – has also been a drag. But if the White House takes action on trade, things could change quickly, sources said.

Quote of the week

“We still have more (sheet) inventory than we’d like, and our toll processing customers have even more – so the system has to be cleared out,” one service center source said. “But at some point, depending on what Trump does and who it impacts – there could be a dramatic shift. And if the mills get the wind at their backs, they’ll show no mercy.”

Hot-rolled coil

The SMU price range is $680-720/st, averaging $700/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is up $10/st w/w. Our overall average is up $15/st w/w. Our price momentum indicator for hot-rolled steel has been adjusted to higher, meaning we expect prices to increase over the next 30 days.

Hot rolled lead times range from 4-6 weeks, averaging 5.0 weeks as of our Jan. 22 market survey.

Cold-rolled coil

The SMU price range is $840–950/st, averaging $895/st FOB mill, east of the Rockies. The lower end of our range is down $30/st w/w, while the top end is up $10/st w/w. Our overall average is down $10/st w/w. Our price momentum indicator for cold-rolled steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Cold rolled lead times range from 4-8 weeks, averaging 6.6 weeks through our latest survey.

Galvanized coil

The SMU price range is $820–880/st, averaging $850/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $20/st w/w. Our overall average is down $10/st w/w. Our price momentum indicator for galvanized steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $917–977/st, averaging $947/st FOB mill, east of the Rockies.

Galvanized lead times range from 4-8 weeks, averaging 6.4 weeks through our latest survey.

Galvalume coil

The SMU price range is $830–910/st, averaging $870/st FOB mill, east of the Rockies. Our range is unchanged w/w. Our price momentum indicator for Galvalume steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,124–1,204/st, averaging $1,164/st FOB mill, east of the Rockies.

Galvalume lead times range from 4-8 weeks, averaging 6.5 weeks through our latest survey.

Plate

The SMU price range is $860–940/st, averaging $900/st FOB mill. The lower end of our range is up $60/st w/w, while the top end is up $50/st w/w. Our overall average is up $55/st w/w. Our price momentum indicator for plate has been adjusted to higher, meaning we expect prices to increase over the next 30 days.

Plate lead times range from 2-6 weeks, averaging 4.5 weeks through our latest survey.

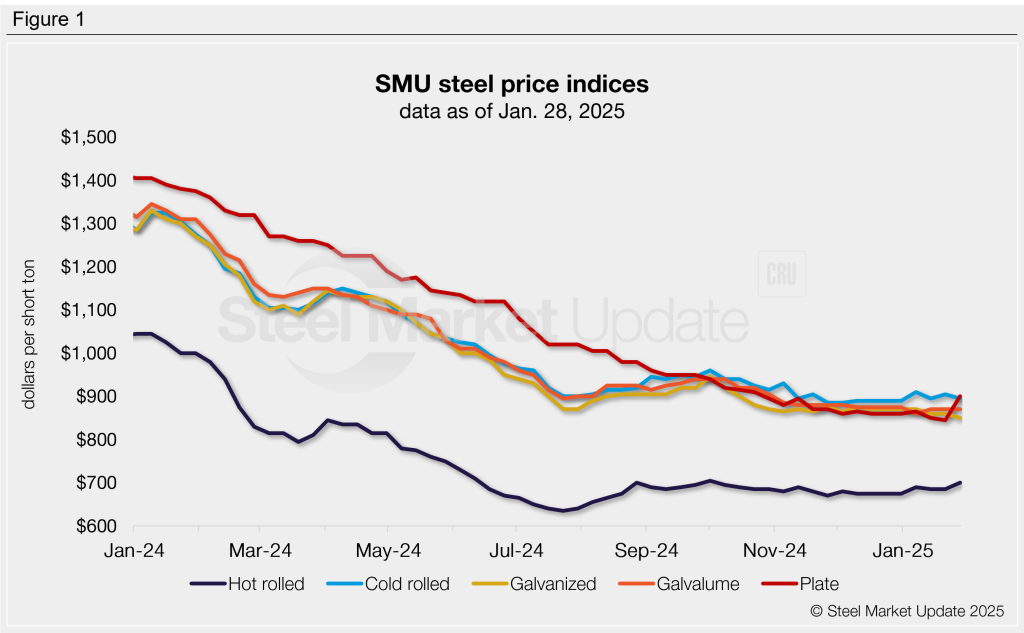

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton