Analysis

January 26, 2025

Final Thoughts

Written by Michael Cowden

President Donald Trump on Sunday hammered Colombia with 25% tariffs and threatened to increase them to 50%.

In a post on Truth Social, Trump said he took the action not because of a trade dispute, but because the South American nation had refused to accept planes carrying deported immigrants.

The president also cited “national security” concerns, just as he did to justify 25% Section 232 tariffs on steel in his first term.

Even the 50% threat echoes his first term. Turkish steel, like that of most nations, was assessed a 25% tariff in March 2018. Trump doubled Turkey’s tariff to 50% via a tweet in August of that year over a matter unrelated to steel.

US presidents aren’t like kings on most matters. But as we learned from Section 232 in 2018, they are like royalty when it comes to making or breaking trade deals. And, for better or worse, Trump appears to be intent on expanding such powers in his second term.

The move against Colombia might have a big impact on coffee. Colombia exports quite a lot of it to the US. It will probably have vanishingly little impact on steel. Colombia exported only 7,243 short tons (st) of steel to the US last year, according to Commerce Department figures. That’s less than a domestic sheet mill can churn out in a day.

But the post on Truth Social on Sunday served as a reminder that the president can change international policy via executive order, live TV, or social media whenever he feels like it. And it doesn’t matter whether that’s during normal business hours, in the middle of the night, or on what is for many a day of rest.

So what comes next for steel?

Tariff speculation

US steel market participants expect flat-rolled steel prices to rise in the months ahead on tariffs or other trade protections from the Trump administration. Exactly what the catalyst might be or which mechanism might be used depends on who you ask.

Some of our contacts pointed to potential 25% blanket tariffs on imports from Canada and Mexico – which Trump has threatened to impose as soon as next Saturday, Feb. 1. Others said blanket tariffs against Canada, for example, would be hard to implement in practice. Case in point: US refineries rely heavily on heavy crude oil from Canada. And so any tariff could immediately backfire on the US.

If what comes next remains murky, there isn’t even agreement on what’s happening now. A recent Bloomberg article, for example, said that Mexican mills had stopped shipments to the US.

But an industry source familiar with the matter told me over the weekend that not all Mexican producers had stopped shipping. He said any halt in shipments might be limited to coated products – and perhaps to those from just one mill. And he said any pause might have more to do with the coated trade case than with potential tariffs. He also said another major mill continued to ship sheet to US customers and would continue to do so unless and until tariffs were rolled out.

That said, this much seems clear, the steel industry (and the rest of the world) continues to hang on every Trump utterance.

The revenge of Section 232?

Speaking of Section 232, some market participants said that the measure, a point of pride among Trump’s first administration, might pose a bigger risk to the status quo for steel than potential blanket tariffs. That’s partly because the templates for Section 232 already exist as do the legal precedents justifying it.

Also, the measure was justified in Trump’s first term not only by national security but by a desire to get US mill capacity utilization rates above 80%. SDI CEO Mark Millett in the company’s earnings call last week highlighted the efficiencies that come when mills run at or above that level. And capacity utilization at US mills has been well below 80% for a while now, according to figures from the American Iron and Steel Institute (AISI).

To have a big impact on the steel market, Trump might not need to implement new policies. He could, for example, remove the tariff-rate quotas negotiated between the Biden administration and US allies such as the EU and the UK. Or he could slash exemptions or exclusions. Another option: Reduce quotas or remove tariff waivers for countries that agreed to quotas.

Survey says prices should rise

I’ll turn now to what we do know – the data from the survey we released to our premium members on Friday and the comments that some of you submitted along with your survey responses. (Thanks. We appreciate you taking the time.)

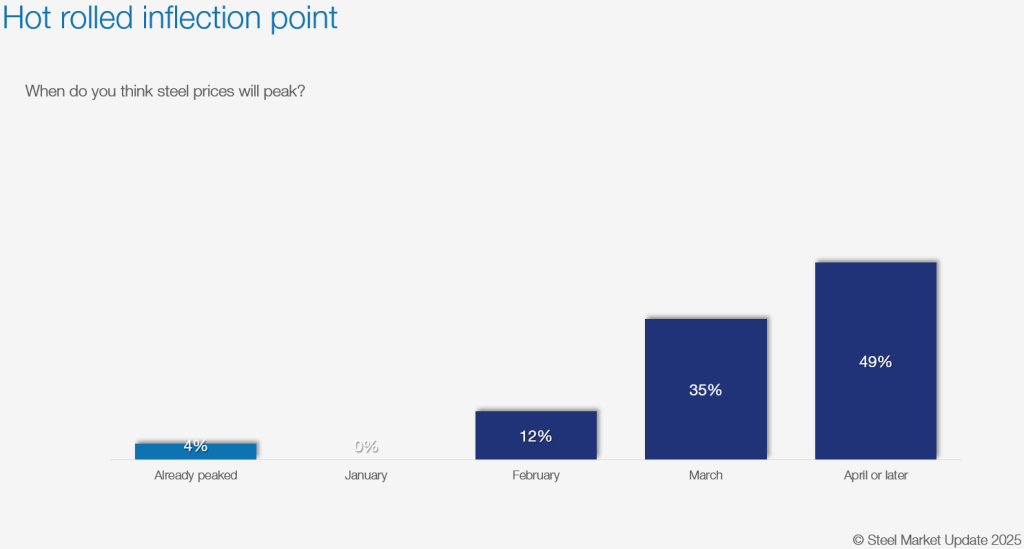

No one we surveyed thinks that hot-rolled (HR) prices will peak this month. And few expect that prices will peak in February. Thirty-five percent think prices will peak in March. And nearly half think HR prices won’t peak until Q2:

Here is what some respondents said about why prices should move higher into late Q1 and Q2.

“Impending tariffs will drive pricing higher.”

“Tariffs, consolidation, and higher scrap/raw material prices”

“Tariffs, if announced February 1st, will supercharge orders and prices will shoot up.”

“Tariffs will drive prices up.”

“I guess I’m hoping that Trump’s tariffs will cause some activity or price increases in steel.”

“Trump policy impact will begin to kick in.”

“Tariffs and increased demand – economic data continues to surprise to the upside.”

“Limited offshore commitments in late Q1, early Q2 will lead to increased mill demand.”

“After President Trump takes some tariff action.”

“Government action. Restocking.”

“Demand should increase in Q2 and Q3 and will put pressure on pricing as tariffs will reduce offshore inventory.”

Pricing volcano? Meh.

While people expect sheet prices to rise on tariffs, few think they will explode higher.

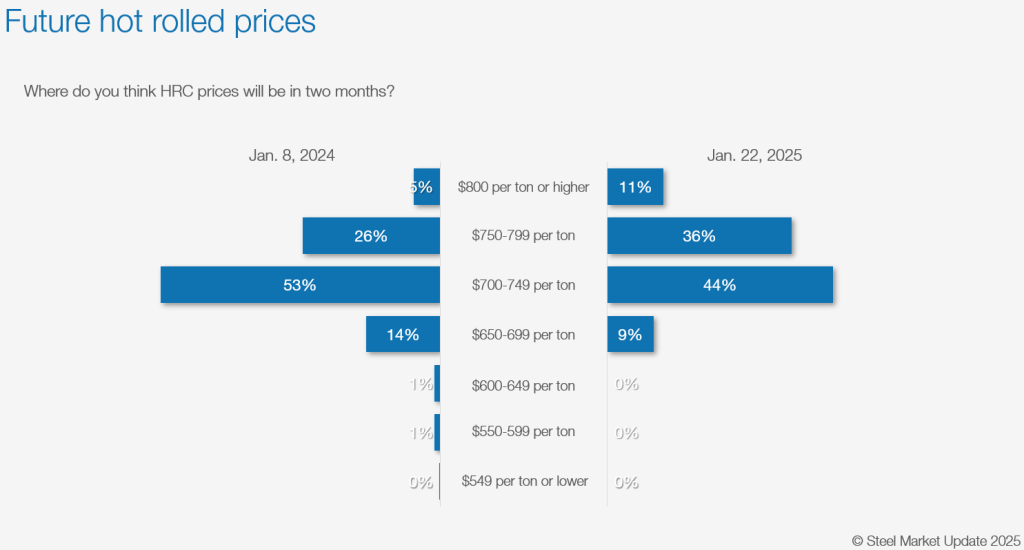

SMU’s HR price currently stand at $685 per short ton (st). It has been at that level, give or take $20/st, since mid-August, according to our pricing tool.

Most survey respondents (80%) think that HR prices will be in the $700s/st, or slightly above where they are now, at the end of the second quarter. Only a small minority (11%) think HR prices will move above the $800/st threshold:

Here is what they had to say:

“I think we have some changes coming our way that will shift the current supply chains.”

“Flat to moderate increases as economy is slowly recovering.”

“Excess capacity and lower manufacturing.”

“The move in pricing that I thought Trump’s tariffs would cause may not be as strong as I thought.”

“Maybe some more drops, some ‘Trump bumps’, and then some actual upward momentum in Q2/Q3? Demand is just too crappy right now.”

“I feel we will see a slow and steady increase in pricing due to demand improving. I don’t feel tariffs will cause a rapid spike.”

Where’s the demand?

Remember Wendy’s “Where’s the beef?” commercial in the 1980s? If we translate that to today’s steel industry, it might be “Where’s the demand?”

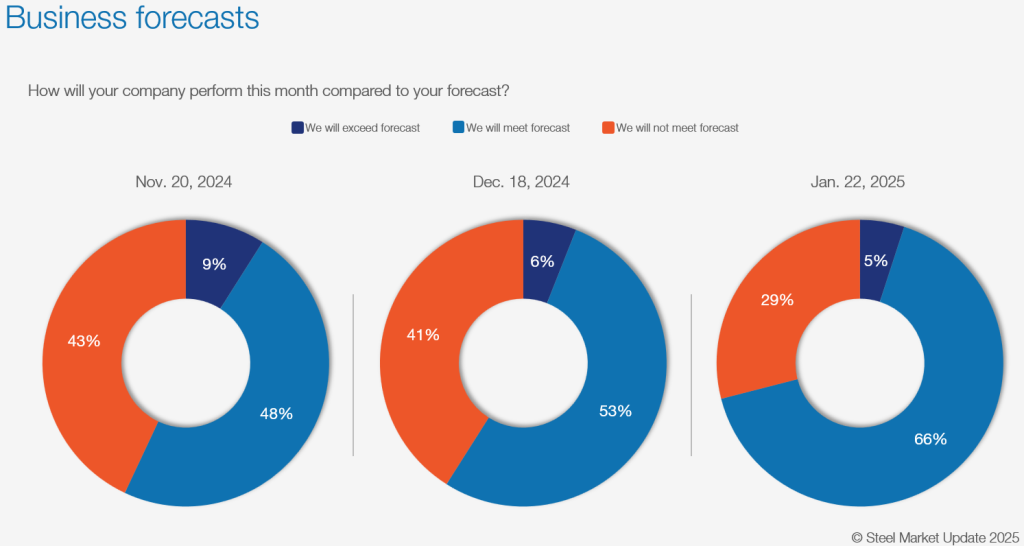

More people told us that they met forecast (66%) this month. That’s better than prior months. And fewer (29%) said they missed forecast. That’s good. But, yet again, very few said that they exceeded forecast:

Here is what some of them had to say:

“Met forecast. Though the bar is set low.”

“Meager forecast.”

“Our business conditions are in a downturn.”

“I have to imagine that sales are down, but we’ll do alright.”

“Too much uncertainty and lack of commitments by customers.”

“For the third month in a row, I think we’ll miss forecast, which is awful.”

“Remaining conservative.”

My takeaway

From what I can tell, most steel market participants expect that Trump will act aggressively on trade. Many also think that those actions should be good for their businesses.

But with demand still uneven and so much still unknown, few are willing to predict an upsurge in prices or to change buying patterns.

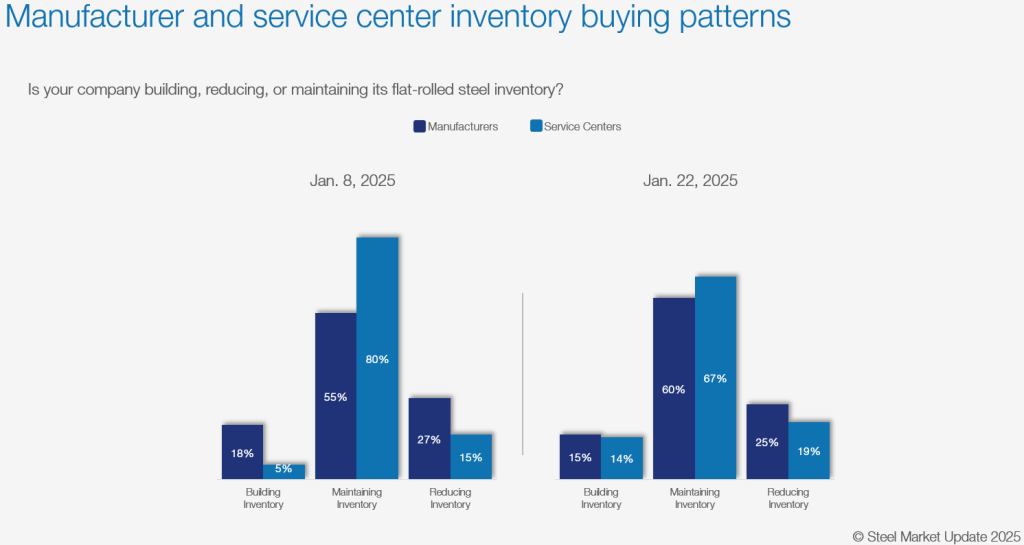

Indeed, most steel buyers we survey continue to maintain inventories – which is what they were doing before Inauguration Day. Few are building stocks, even with the threat of tariffs now turning into reality (at least in the case of Colombia).

Tampa Steel Conference

More than 500 people have registered to attend the Tampa Steel Conference. And we’re on track to break last year’s record of about 550 people.

Some of you have asked me whether it’s too late to register. Definitely not! Our room blocks are sold out. But you can find a list of nearby hotels here. Meanwhile, check out the latest agenda here. Finally, you can register here. Me and the rest of the SMU team look forward to seeing you next week in Florida!