Analysis

January 12, 2025

Final Thoughts

Written by Michael Cowden

I wrote in a Final Thoughts a few years ago that it seemed all the swans were black. More recently, I’ve been asked by some of you what the wildcards are for 2025. You could probably make the case that all the cards are wild now.

Stretching the meaning of “deadline”

Take U.S. Steel. President Biden blocked its acquisition by Nippon Steel. Lawsuits followed. SMU readers howled. And then, just a few days later, the Committee on Foreign Investment in the US (CFIUS) extended the deadline for unwinding the deal from early February to mid-June.

So, has it really been blocked? Or has the can been kicked down the road yet again?

There had also been speculation that either Cleveland-Cliffs or U.S. Steel might idle a furnace pending the outcome of the deal. To date, neither has. And with the deadline extended until June, maybe neither will?

Tariffs galore. But how big and when?

Then there is the matter of trade and tariffs. Some think that President-elect Donald Trump’s tariffs are mostly a negotiating tool – and that they might not be an immediate priority for the incoming administration.

Others say that US trade policy could be revolutionized starting at noon on Inauguration Day. That includes blanket tariffs on both allies and foes, the ending of Section 232 exemptions for some countries, and measures to protect downstream industries. In other words, things that could have a direct impact not only on steel but across global supply chains.

And it’s not just a question of what Trump might do. How will other react? Canada has threatened to retaliate. Also, Jan. 20 isn’t the only date to keep in mind. Here’s another: April 1.

Yep. April Fools’ Day. The truce between the US and the EU over Section 232 expires on March 31. Which means that on April 1, retaliatory tariffs against US goods – things like motorcycles, whiskey, and orange juice – could go back into effect.

Survey says

And yet, as has been the case for a while now, these BREAKING NEWS!!! headlines have been met (so far at least) by a collective “meh” from the steel market.

Take a look at the results of SMU’s latest steel market survey. Lead times haven’t budged. An overwhelming majority of steel buyers report that mills remain willing to negotiate lower prices. And sentiment is below where it was a year ago.

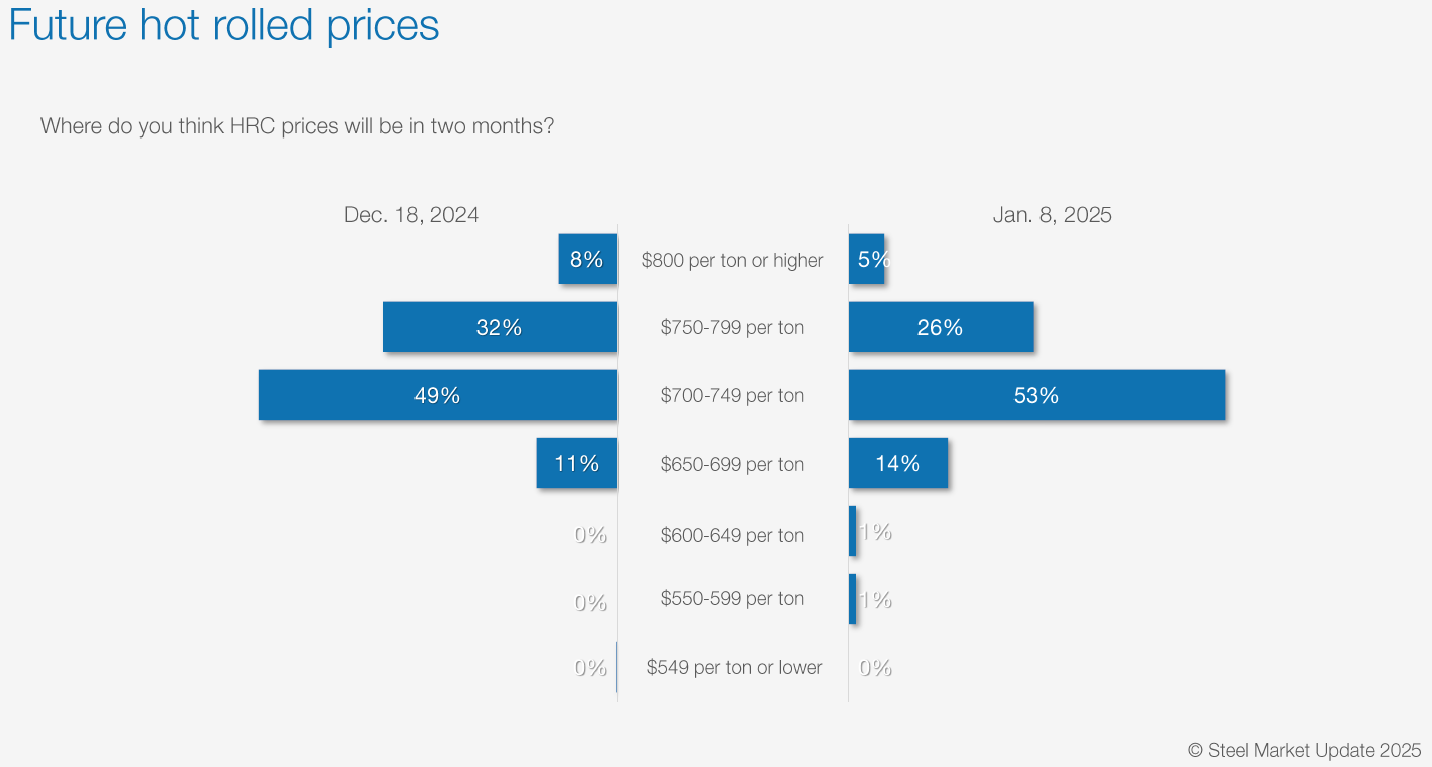

That’s not to say the mood is as gloomy as it was over the summer. When we ask people where they think hot-rolled (HR) coil prices will be in two months, most say in the $700s per short ton (st) – a little higher than where they are now. But few think they’ll crack $800/st.

In other words, almost no one expects a market shock on the scale of Section 232. Despite Trump 2.0 threatening to go a lot bigger on trade than Trump 1.0.

Below is what some survey respondents had to say about why that might be:

“The general trend is that Q1 will be flat.”

“Soft demand and plenty of capacity.”

“Demand seems to be slowly picking up, and there are slight signs of optimism for early 2025. I don’t think there will be drastic movement, but I do expect some solidification of prices.”

“Does not seem like the market has much strength. … Demand could start to come back this week or it could be early February, once industries have a better understanding on the looming tariffs – if they happen at all.”

“Once the new government takes shape, the economy will pick up in the 2nd quarter.”

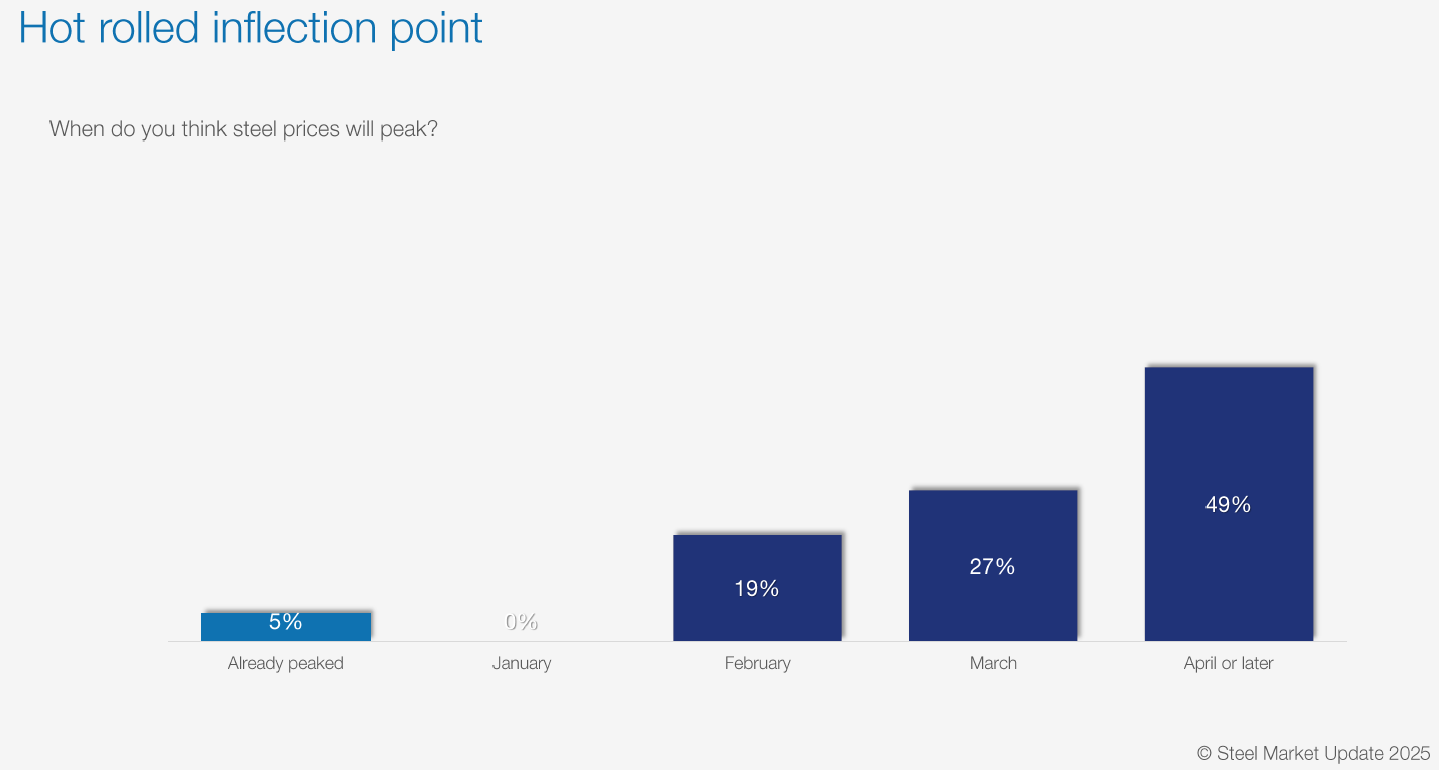

That last quote is worth highlighting. Because our survey results also show that steel market participants expect prices to continue to gain ground into Q2. No one thinks HR prices are peaking this month:

Here is what respondents who think prices will continue to rise into late Q1 or Q2 had to say.

“It all depends on The Donald, really. I don’t expect demand to all of a sudden reverse course.”

“Price is at the bottom now. It will continue to increase past the middle point of the year, especially if there’s a tariff applied and business demand increases.”

“My hope and belief is that we are approaching the bottom now and that we will see some gradual increases throughout the first half.”

“Too much destocking may allow mills to gain momentum once the masses run to place orders. Demand is improving, and the market is going to need steel (and at a time when import volumes are expected to taper).”

“Tariffs (if they come to pass) + CORE dumping investigation.”

Let’s say most buyers assume that prices will increase thanks to Trump’s policies – whether they be tariffs or more pro-business when it comes to issues like taxes and regulations. Why aren’t they buying now to get ahead of those tariffs?

Uncertainty causes market pause

One theme that emerges from our survey, and in channel checks with some of you, is uncertainty around the scope and impact of the tariffs. You can buy ahead of something with a known timeline and quantifiable impact (the CORE trade case, for example). But taking a position on something as fuzzy (to date) as tariffs is not worth the risk.

Another issue that keeps coming up is uneven demand, abundant supply – and low prices.

Yes, scrap will probably rise modestly. But newer capacity is coming into the market at low prices, as new capacity tends to do. Meanwhile, certain integrated producers appear to be offering big discounts to some of their bigger buyers. (We’ve heard there might have been some reallocation of automotive tons.)

And then there is the issue of service center inventories. They remained high in November. We’ll be releasing December data this week to our premium subscribers. (If you would like to upgrade to premium – which gives you access to that data as well as our steel market surveys – please reach out to us at info@steelmarketupdate.com.)

December is typically higher than other months, mostly because of the impact of the holidays. So it’s not a good, apples-to-apples comparison to other months. But I will be curious to see how December 2024 stacked up against prior Decembers.

Imports remain elevated, for now

There is an expectation that steel imports will decline on the coated AD/CVD case, Trump 2.0 tariffs, and other trade measures. But in the meantime, it looks like companies might be bringing in more steel ahead of those actions.

Case in point: The US imported 2.41 million st of steel in December, according to Commerce Department data. That’s down from a 2024 high of nearly 2.85 million st in May of last year. But it’s up from 2.07 million st in November and back in line with the 2024 monthly average of 2.43 million st.

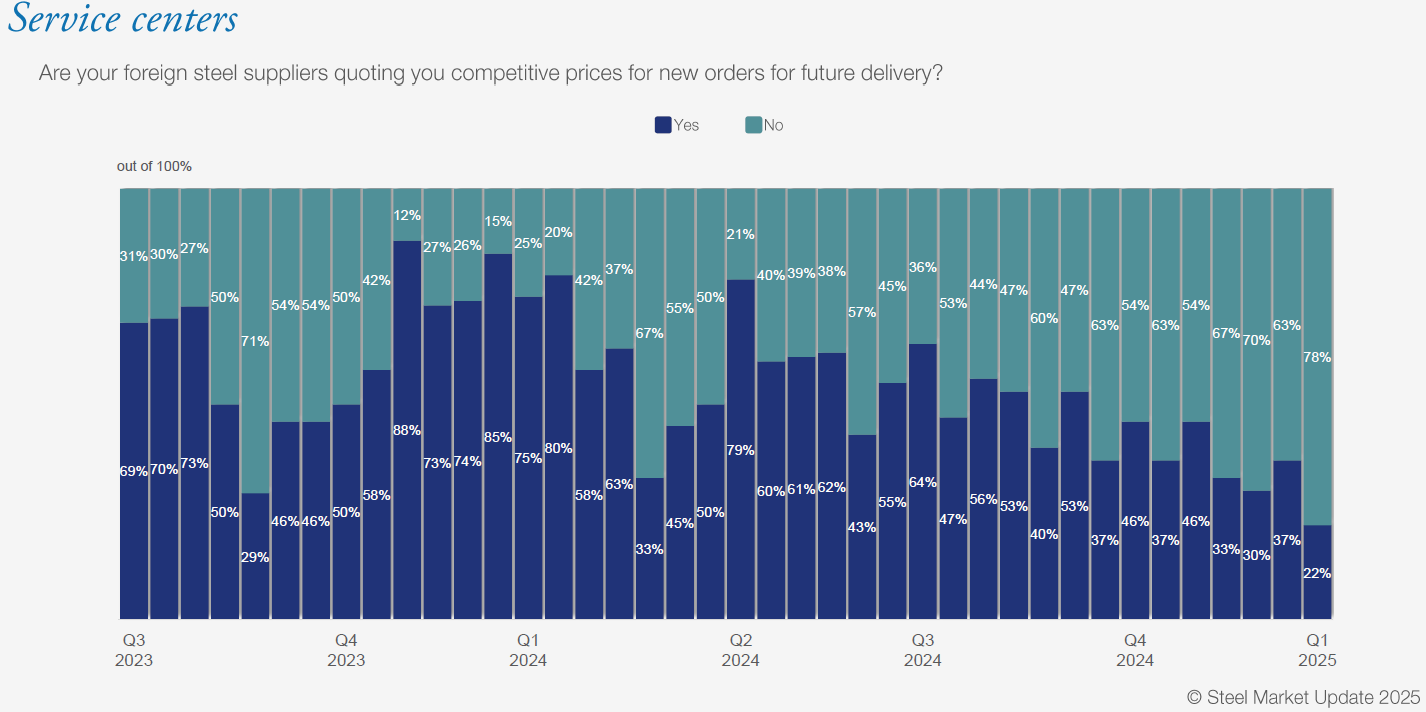

That said, nearly 80% of service centers tell us that current import prices are not attractive:

That number has been increasing steadily since Q3’24. So I think it is fair to assume that import numbers will slide later in 2025. But, again, it’s not happened just yet.

And here’s one to consider looking a little further out than Jan. 20. Yes, trade policy could effectively shift import market share over to domestic mills. You could make the case that that process has been happening for the better part the last decade.

But with so much new capacity out there, would a big shift in sourcing have an equally big impact on prices?

Another wave of new capacity?

One more thing to consider: On the sheet side, almost all new flat-rolled capacity expansion projects that have been announced in recent years have been completed – or at least construction is underway.

But could there be a new wave of new capacity coming in the years ahead? I ask that because I think the news about South Korea’s Hyundai building a new, $6-billion sheet mill in Louisiana deserves more attention.

Where Hyundai goes, POSCO – its chief South Korean rival – typically isn’t far behind. And we already know that there are other sites available. That includes Brownsville, Texas, where other mills – including Ternium and Big River Steel – have previously considered locating a new mill.

After all, the point of recent trade policy has been not only to reduce imports but also to encourage manufacturing activity in the US. It’s not been very successful on the aluminum side. But it’s been very effective on the steel side – where billions have been invested in newer, more efficient capacity.

And if the Nippon-USS deal shows that acquisition is a tough road, maybe we should expect more greenfield projects. Because you can build a new mill for a lot less than the $15 billion it would take to buy U.S. Steel.

Tampa Steel Conference

We’ll be discussing these subjects and more at the Tampa Steel Conference on Feb. 2-4, 2025.

We should also have a better understanding by then of what Trump’s trade policies will be. And it will be a good chance to discuss what they mean for the steel market.

More than 400 of you have already registered. You can see the latest agenda here, the companies attending here – and register here!

PS – The conference hotel, the JW Marriott Tampa Water Street, was close to sold out the last I checked. You can find nearby alternatives here.