Analysis

December 20, 2024

Steel: The CRU view on what to expect in 2025

Written by James Campbell & Josh Spoores

This CRU Insight discusses a few key topics our clients have been asking about as 2024 comes to a close and 2025 begins. This piece introduces these topics briefly now before we discuss them in more detail in a webinar in January 2025.

In previous years, we have published a year-end Insight on our ‘Top Ten Calls’ or in other words, our expectations. This year, we have kept our list to four key topics, but presented further detail on each. To engage with our clients in a more in-depth discussion, we will also be hosting a webinar in January. The key topics include the evolution of global steel demand in 2025, how geopolitics will shift steel trade, what may come of global overcapacity, and finally, how decarbonization in steel may move forward, slow, or stall.

Like any topic we discuss, we encourage feedback and discussion with our clients as it always helps us to sharpen our view.

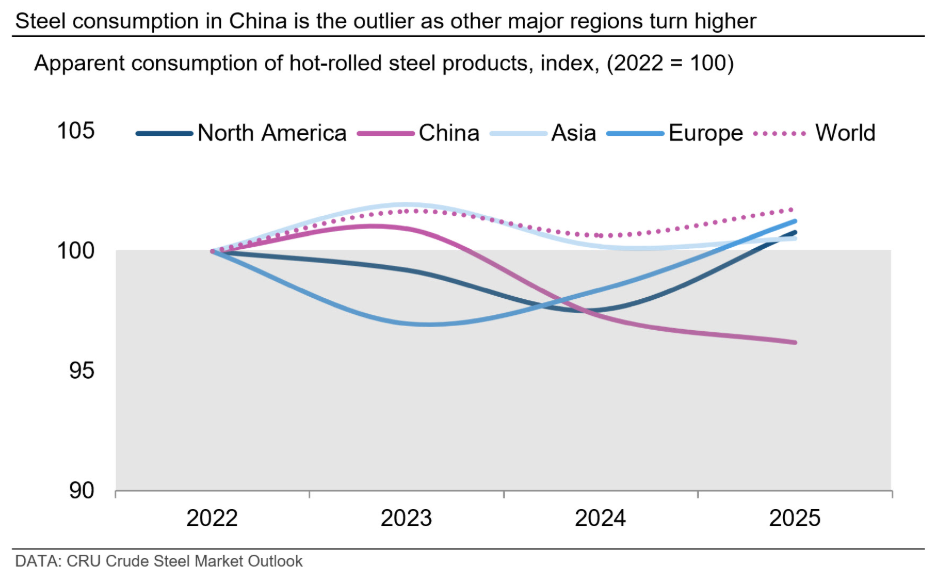

Global steel demand will rebound, even as Chinese demand continues to fall

Steel demand generally follows underlying trends in construction and industrial production. Our most recent Crude Steel Market Outlook (n.b. only available to CRU Crude Steel Market Outlook clients), published earlier in Q4’24, forecasts that consumption of hot-rolled steel products will end 2024 lower by 1.0%, primarily due to weakness in China. However, consumption in 2025 will rebound, supported by rising industrial production activity as well as stronger construction output across most regions. While demand increases, the gain is limited to growth of just 1.1% y/y, equal to approximately 20 million metric tons (mt).

This y/y increase in steel demand is small, yet it is noteworthy when accounting for Chinese finished steel demand falling by 10 million mt y/y in 2025. So even as global consumption appears slow to rise, underlying growth has clearly shifted away from China. A potential surprise here could be a larger-than-expected decline in China, which could keep global steel demand flat, if not lower, y/y.

Geopolitics will drive a change in steel trade trends

In November, we published two Insights on how President-elect Trump may utilize tariffs to influence his agenda. In “Trump tariffs could stimulate steel demand,” we explored how he may use tariffs to support new manufacturing investments in the US. In the second Insight, titled “Trump tariff threat signals early start to trade negotiations,” we focused on how he has already started to use the threat of tariffs to create both leverage and a sense of urgency on US trade partners to negotiate trade deals.

While any new tariffs put in place will likely cover more than just steel, the US has been very aggressive in asking trade partners to implement tariffs on Chinese steel exports. We expect this US-led trade influence to continue, and further barriers will be installed across multiple regions to limit excessive steel exports from China.

In Europe, 2025 is the final year before CBAM arrives. For those buying EU imports, the first decisions for long lead-time coated products will be made in mid-2025. This will drive importers to focus more on carbon emissions to reduce the impact of CBAM. More focus will be put on emissions of individual assets, which are available in CRU’s Steel Emission Analysis Tool. The surprise we expect here is for high-emission imports to continue being ordered in mid-2025 as traders exploit loopholes in the legislation. This is a high-risk game as we also expect some loopholes to be closed by the European Commission. Follow developments closely using our Global Steel Trade Service (request a steel demo here).

The rising trend of Chinese steel exports will end

Stein’s Law postulates that “if something cannot go on forever, it will stop.” This simple yet profound view applies to many things, such as the trend of excessively low interest rates after the Covid-19 pandemic had run its course; or the unsustainably low steel sheet prices in late 2015 and early 2016, as noted in this Insight here.

When our analysts view the Chinese steel market, we see a test case to apply Stein’s Law, particularly based on trends seen in 2024. During this year, consumption of hot-rolled steel products in China fell 3.6% y/y and has been down for three of the last four years. Consumption is now down 9.6% or nearly 100 million mt since 2021 and is forecast to fall through the medium term. This recent decline comes alongside the dramatic slowdown of construction activity. However, falling consumption has not yet led to a widespread restructuring of capacity in China. Instead, mills have gotten by with substandard margins by increasing exports.

Our demand forecast in 2025 calls for hot-rolled steel products in China to fall by another 10 million mt. Due to this continued decline, alongside further changes to steel trade, the recent excess of Chinese steel exports must reach a peak and start to reverse course. We expect these exports are at, or near, their peak and an industry restructure will come about to eliminate some of this excess capacity in China in the second half of 2025 or early 2026.

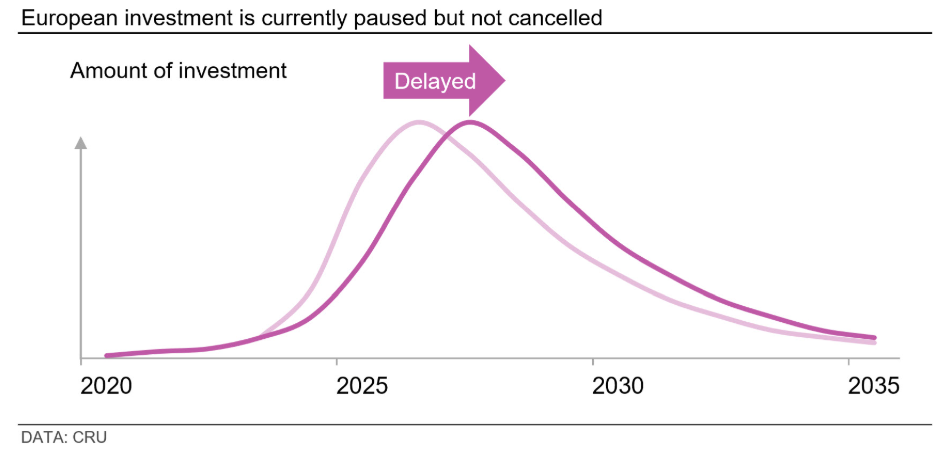

Decarbonization: Green steel investment delays will open the door for mass balanced solutions

The big question surrounding future investment in steel is if interest in steel decarbonization has peaked or just paused. Will the so-called ‘green steel’ investments announced in recent years happen, or will ‘cancel culture’ come to steel?

Most investment announcements so far have been focused in Europe. The steel industry there has embarked on a once-in-a-lifetime technology shift in order to decarbonize an industry that accounts for 5–10% of global CO2 emissions. Significant investment is still needed and will come about, but some investments have been paused. This is partly due to the policy environment but also a function of the steel market today – the European steel industry needs to invest $50–100 billion over the next 20 years, but current cashflow is weak, and steel users’ willingness to pay a ‘green premium’ is low.

We expect some European investments to be delayed or paused for one to three years to wait for a more supportive policy environment and/or for increased government support to be agreed. In particular, steelmakers will be looking for progress in the rollout of hydrogen networks and for country-by-country investments in renewable energy generation and transmission. Without this, we could see some EU ironmaking investments move to other regions, such as the Middle East, where natural gas and energy supplies are in excess and cheap. This could be a big surprise for 2025.

The delay in green steel projects opens the door for those already approved and being built, for example, Stegra. Although it needs to overcome challenges associated with new technologies, the project is in a region where renewable energy supply is more plentiful and cheaper than in other European countries. The delay in investments opens the door for mass balancing to take over as a temporary solution until domestic green steel supply arrives in bulk. Although relatively new to steel, other industries – such as energy, chemicals and paper – already use mass balancing successfully. In 2025, a surprise could be the expansion of mass balanced steel products offered by non-EU sources – including China – ahead of CBAM arriving in 2026.

In summary, 2025 will bring rising demand, disrupted trade, and delays to emission investments

The four topics covered here – rising demand, changing trade flows, lower Chinese exports as capacity there is restructured, and delays to the emissions-related investments in Europe all have the potential to disrupt the steel markets.

If the recovery of steel-intensive economic activities is slower than anticipated, global demand gains may not materialize, particularly considering our expectation of a continued decline in Chinese steel demand. Restricted steel trade is perhaps the most obvious expectation in 2025, with President-elect Trump coming back into office and seemingly ready to use tariffs aggressively.

As for steel trade, the US has threatened to apply blanket tariffs to some countries, which would inevitably have a second-order effect on steel consumption if those tariffs were put in place. We may also see Trump revisit the S232 tariffs on steel as well as alter the various exemptions and quotas surrounding these tariffs. It appears necessary for a restructuring of capacity to take place due to the decline in domestic demand in China and the heightened trade restrictions. However, the process may take longer than initially anticipated.

These are all complex topics with variables that seemingly change from one quarter to the next. As variables and expectations change, CRU will continue to update our forecasts and engage with clients. We will announce a client webinar in late January to discuss these topics in more depth – if you’re interested, feel free to join us.

This analysis was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

James Campbell

Read more from James Campbell