Analysis

November 12, 2024

Final Thoughts

Written by Michael Cowden

President-elect Donald Trump will officially retake the White House on Jan. 20. I’ve been getting questions about how his administration’s policies might reshape the steel industry and domestic manufacturing.

I covered the tumult and norm-busting of Trump’s first term: Section 232, Section 301, USMCA – and that’s just on the trade policy side of things. It’s safe to say that we’ll have no shortage of news in 2025 when it comes to trade and tariffs.

When it comes to current market conditions, however, not all that much has changed. At least not yet. Some of you tell me there has been some post-election improvement in activity. But not enough to really move the needle on prices.

Tee up the tariffs

Trump repeatedly professed his love for tariffs on the campaign trail. He floated tariffs of 60% on imports of Chinese goods and of 10-20% on imports from other nations. Whatever the actual figure and scope is, I wouldn’t dismiss Trump’s comments as bluster.

The president has broad powers, especially when it comes to trade issues. What we learned in Trump’s first term was that those powers could be used not only to make trade deals but to break them too.

Case in point: Trump imposed Section 232 tariffs on March 8, 2018. In some respects, that wasn’t unexpected. There had been rumors that he would take action as early as the spring/summer of 2017. That said, I don’t think anyone – even those in the room when it happened – expected blanket 25% tariffs on steel.

And yet that’s what went down. I remember touring what was then ArcelorMittal USA’s Burns Harbor Works in Northwest Indiana at the time. And I still recall how the move caught everyone, including a company media representative, by surprise.

It was a similar situation when President Trump on Aug. 10, 2018, doubled Turkey’s Section 232 tariff to 50% via tweet over a matter unrelated to steel. I spent that random summer Friday learning that, yes, he could do that. What’s different now? As best as I can tell, only that Twitter is X.

Here’s another point of continuity when it comes to Trump and trade: Robert Lighthizer could have a big role in shaping trade policy in Trump’s second term. Lighthizer served as US Trade Representative (USTR) in Trump 1.0 and was one of the engineers of policies such as Section 232 and Section 301.

Before that, he was a trade attorney at Skadden, where he represented U.S. Steel – including in a landmark trade petition in 2009 targeting what then were rampant imports of Chinese oil country tubular goods (OCTG). To paraphrase Barbara Mandrell, Lighthizer was country when country wasn’t cool. And now that it is cool, why would he (or Trump) change tune when it comes to tariffs, trade, and China?

Take the ‘M’ (and/or ‘C’) out of USMCA?

Another lesson from Trump 1.0 was that “national security” could be invoked to slap tariffs on US foes and allies alike – including Japan, the European Union, and (initially) both Canada and Mexico.

Lighthizer helped negotiate USMCA in Trump’s first term after the president promised in his 2016 campaign to get rid of NAFTA. It went into effect in July 2020 and is up for review every six years.

Cleveland-Cliffs Chairman, President, and CEO Lourenco Goncalves has this year made a talking point about taking the ‘M’ out of USMCA. Could that become a talking point for Trump as well?

It’s worth considering whether Canada might be in the crosshairs too. Nucor Chair, President, and CEO Leon Topalian has vented frustrations about alleged “unfair” trade from both Canada and Mexico. He said that China has been transshipping steel through both countries.

Assuming USMCA remains in place, it will almost certainly have more teeth in 2026 than it does now – especially when it comes to allegations of transshipment.

Demand still lackluster (for now)

Potential trade policies and key Cabinet appointments are sure to grab headlines as the transition to Trump 2.0 gains steam. One thing that might not is the state of demand.

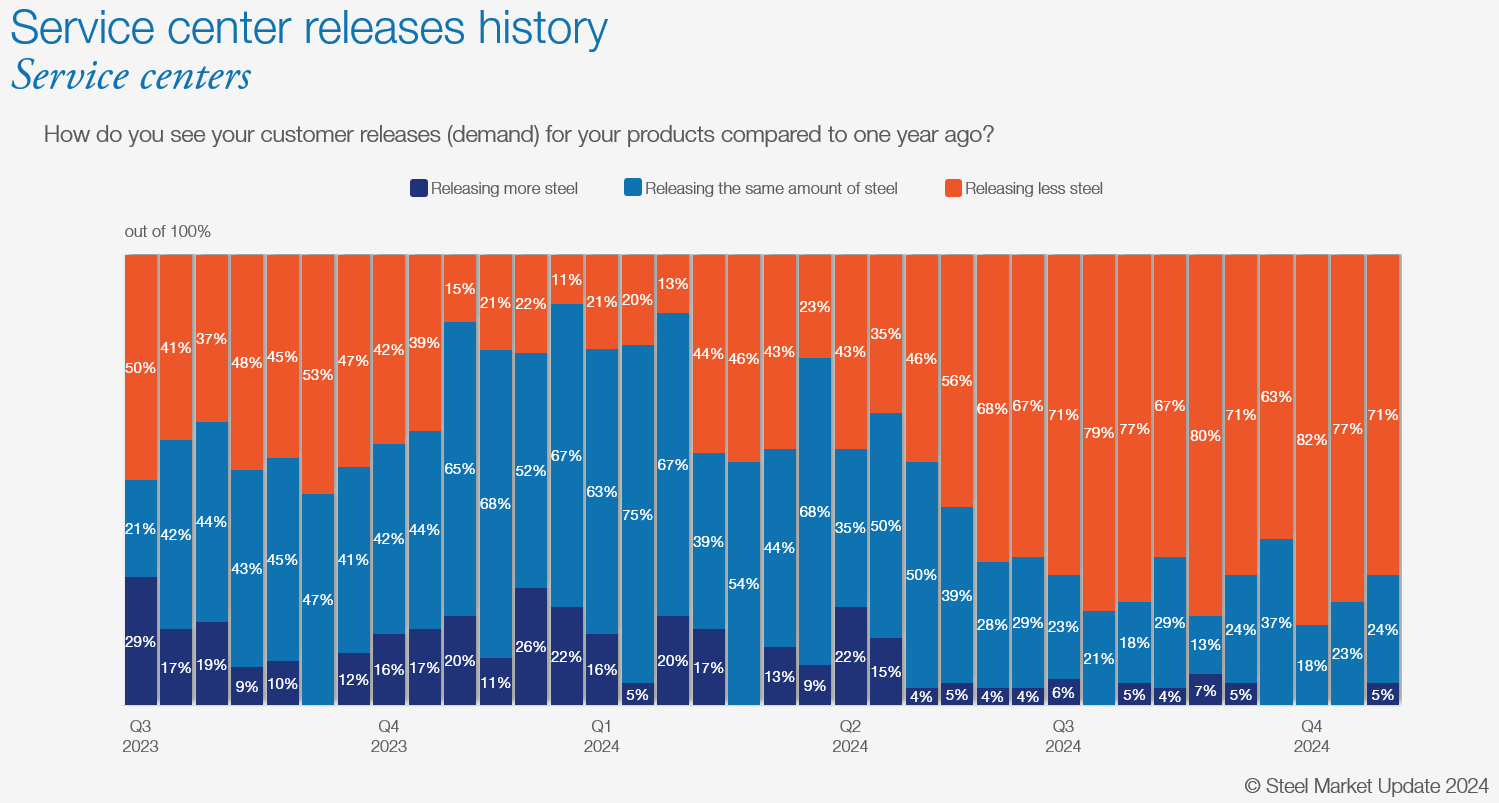

SMU asks service centers in our market surveys whether they are releasing more or less steel than a year ago. The orange line means that centers are releasing less steel. The light blue lines that they are releasing the same amount of steel. And the dark-blue lines that they are releasing more steel.

You can see that since about the middle of Q2, most service centers (and 70-80% more recently) have been releasing less steel than they were in 2023. Can a new presidential administration somehow change that trend?

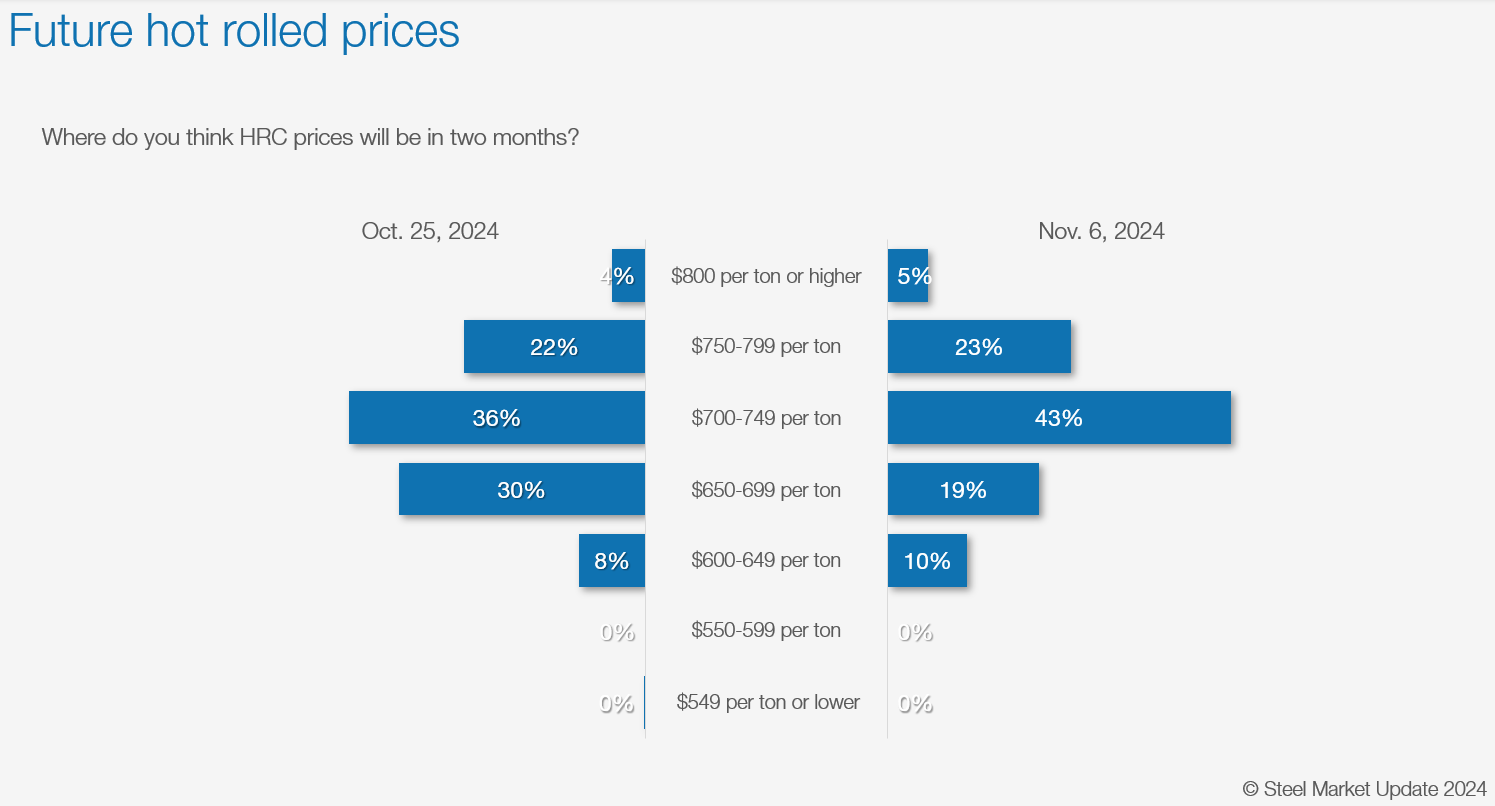

As for steel prices, we surveyed buyers the week of the election. US politics was turned upside down on Nov. 5. The steel market was not.

In fact, steel buyers’ expectations for steel prices barely budged. Most (65%) predicted that hot-rolled (HR) coil prices would be in the $700s per short ton come early January – a little higher than they are now.

You could make the case that the market was being too cautious. US buyers tend to hunker down in wait-and-see” mode ahead of an election. And there probably is more upside risk than downside risk now.

New capacity still coming

That said, Section 232 tariffs – as well as waves of AD/CVD petitions over the last decade – have resulted in a far more protected US flat-rolled steel market. US mills have responded to those protections by investing billions in new, more efficient capacity.

Take Big River 2 (BR2), which will double production at the Osceola, Ark., steel mill from 3 million tons per year to 6 million tons per year. BR2 made its first coil in late October. Qualifications and trials are expected to continue through the end of the year. And the mill is slated to have a bigger commercial presence as it ramps up into Q1.

Those tons will come into the market as SDI Sinton runs more reliably and as North Star BlueScope continues to make progress with a capacity expansion in Ohio. And that’s just a short list of new capacity. (Fun fact: The only major new sheet capacity not yet built is Nucor’s planned mill in West Virginia.)

New duties on coated products might well squeeze out more than 2 million tons of imports out of the US market, a point some mills have been keen to stress. But the deadlines on that case have been pushed back. And, in the meantime, material continues to come in – and might continue to through early Q1.

The coated case should stimulate more domestic buying next year. But there is a lot of new coating capacity in the US. Also, how many tons will come in from Indonesia – which more than a few buyers have turned to as a potential alternate to some of the countries targeted in the petition?

The big picture

Let’s loop back to the logic behind Trump’s tariffs strategy. The tariffs are designed to bring manufacturing back to the United States. How long does it take to rebuild factories – perhaps entire industries – that have been offshored? And how is there not at least some pain in the form of inflation between when those tariffs are introduced and when that reshoring occurs (assuming it does)?

Trump backers might note that the US has a lot of leverage over export-oriented economies such as Germany and South Korea. And they might say that such countries will have no choice but to “eat” the tariffs. Or maybe, as with Section 232, we’ll see plenty of exemptions granted to allies such as Japan. Right now, it’s hard to do more than speculate.

Inauguration Day is not that far away, and so we’ll know – and experience – the answers soon enough!

Tampa Steel Conference

SMU will hold the Tampa Steel Conference on Feb. 2-4, 2025, together with our partners at Port Tampa Bay. It will be a great place to come together with leading industry executives and analysts to assess the market and the initial impact Trump’s second term. You can learn more and register here.

And, in the meantime, thanks to all of you from all of us at SMU for your continued business.