Analysis

October 29, 2024

Final Thoughts

Written by Michael Cowden

Nucor said it is seeking $740 per short ton (st) for hot-rolled (HR) coil this week, up $20/st from last week. USS, meanwhile, is shooting for up $30/st for sheet products in general. (USS did not announce a target price for HR.)

We haven’t seen a consolidated push by domestic mills to push sheet prices higher since July/August. That round of price hikes sparked a mini-rally that brought HR prices from as low as $600/st to approximately $700/st. (You can follow along with our price announcement calendar.)

Does HR get to approximately $750/st this time around? It’s probably too early to say whether these increases from Nucor and U.S. Steel will stick. But let’s consider a couple of possibilities.

On the one hand

Sheet prices have been sliding recently and HR has dipped back into the $600s/st. We saw ~90-100% (depending on the sheet product) of respondents to our last steel market survey saying that mills were willing to negotiate lower steel prices.

Was that a case of last-minute deals before mills try to hold the line? Or maybe these increases represent an attempt to get buyers off the sidelines and stop the bleeding – especially amid contract talks.

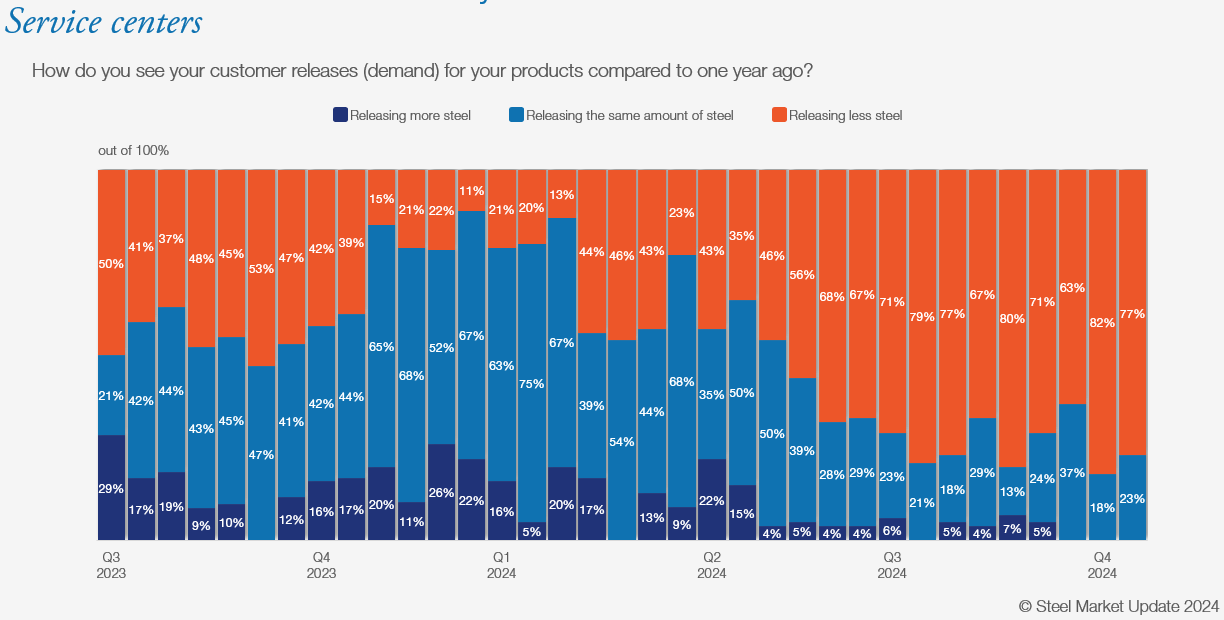

It probably doesn’t help that some have lead times as short as 4-5 weeks not only for hot-rolled products but for coated as well. And on a very basic level (see chart below), how can you increase prices when roughly 80% of service center respondents to SMU surveys say that they’re releasing less steel than they were a year ago?

I know some larger buyers don’t give these latest price hikes much credence. They’re seeing certain mills willing to match or come close to matching South Korean offers of approximately $620-630/st. And they think domestic mills will get to $600/st or even into the $500s/st before the year is out. They are saying they’re going to stay on the sidelines a little longer in anticipation of that happening in November or December.

On the other hand

Mills could be raising prices based on some good fundamentals. Lead times are close to (or into) 2025 at some mills. Q1 is typically busier. And the impact of the coated trade case should be felt more in earnest by next year. Let’s say imports and service center inventories tick lower too. Why shouldn’t mills start positioning themselves now for a potentially better new year?

For every sheet buyer who says HR will fall to $600/st again, I know another who thinks prices are already near a bottom. They think the market should improve once uncertainty around the election has cleared and as lead times stretch into (or further into) 2025.

How to square these divergent viewpoints? I think some of our other data is worth sharing here as well.

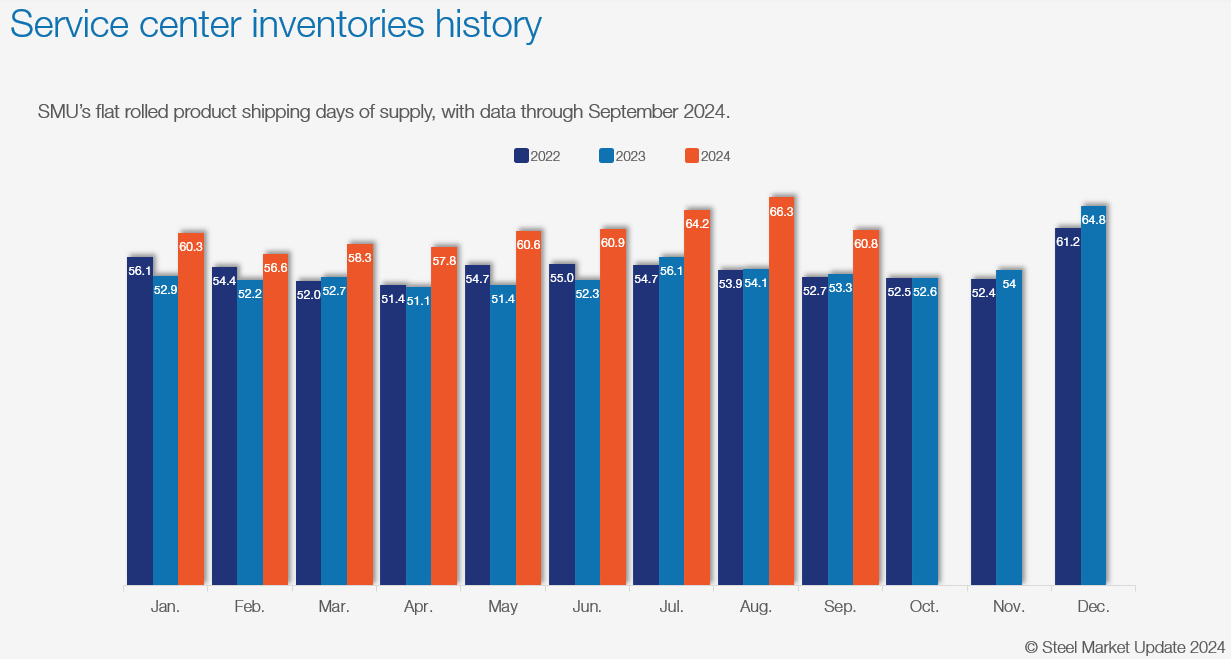

For starters, sheet inventories are still high compared to 2022 and 2023. But they moved lower in September vs. August.

We won’t have October inventory data available until mid-November. But take a look at the chart below:

Very few buyers are restocking. So I would not be surprised if we saw inventories drop in October and perhaps again in November. (December is a little squirrely because of the holidays. So I wouldn’t read too much into that.)

September marked the lowest point for steel imports this year. October import license data aren’t complete yet. But it wouldn’t be shocking if imports moved lower again.

Yes, new capacity will fill some of that void. Still, let’s say demand is better in 2025 than it is now. Maybe, just maybe, instead of the slow slide in prices that we’ve seen this year, we’ll see slow but steady gains – a melt up, if you will – next year.

It’s worth thinking about. In the meantime, thanks to all of you from all of us at SMU for your continued business.

SMU Community Chat

Don’t forget to tune into the Community Chat on Wednesday at 11 am ET with trade attorney and SMU columnist Lewis Leibowitz. You can register here.

We’ll talk steel, trade policy, the election, geopolitics – and we’ll take your questions too. It should be a good chat. And, with any luck, my internet connection won’t cut out this time. (And if it does, Dave Schollaert will capably fill in for me as he did with Barry Zekelman on Oct. 16.)