Market Data

September 10, 2024

SMU price ranges: Sheet momentum indicator shifts to neutral in mixed market

Written by Brett Linton

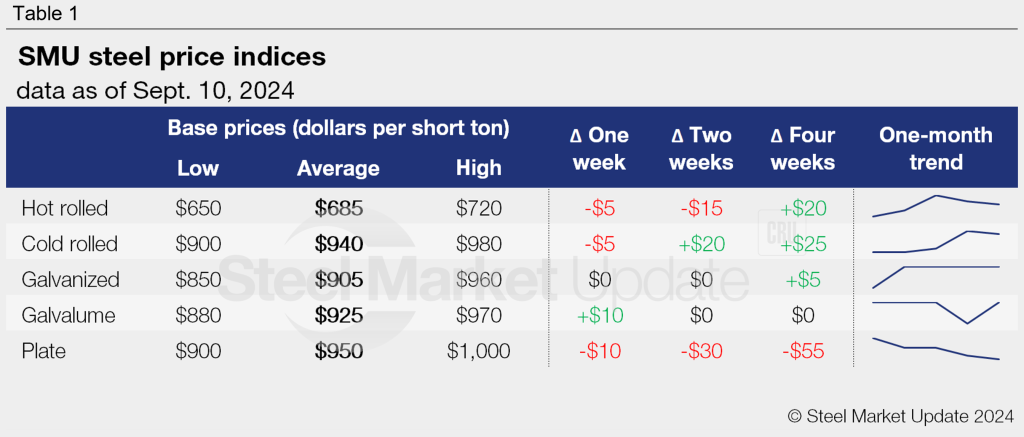

SMU’s steel price indices showed mixed signals for a second consecutive week. Our hot rolled, cold rolled, and plate prices inched lower from last week. Galvanized prices, meanwhile, held steady. And Galvalume ticked higher.

While mills push for price increases, concerns about bloated inventories and weak end-market demand have made buyers cautious. It is also not yet clear how the coated trade case filed last week will impact the market.

In light of this, we have adjusted the SMU sheet price momentum indicator from higher to neutral. Our plate price momentum indicator remains at lower.

Hot-rolled steel prices eased for a second consecutive week, declining $5 per short ton (st) to an average of $685/st. Despite the recent declines, HR prices are still up $20/st from a month ago, according to our Interactive Pricing Tool.

Cold-rolled sheet prices also shifted lower, down $5/st week over week (w/w) to $940/st. Prices are still $25/st higher than four weeks ago.

While our price range for galvanized sheet widened, our average galvanized price did not budge this week, holding steady at a nine-week high of $905/st. Galvalume prices ticked back up $10/st w/w to $925/st, reverting back to the average price reported in the last three weeks of August.

Our plate index dropped $10/st to $950/st this week. Plate prices have fallen $55/st over the last month and have trended downward since last November.

Hot-rolled coil

The SMU price range is $650-720/st, averaging $685/st FOB mill, east of the Rockies. The lower end of our range is down $10/st w/w, while the top end is unchanged. Our overall average is down $5/st w/w. Our price momentum indicator for hot-rolled steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Hot rolled lead times range from 3-7 weeks, averaging 5.2 weeks as of our Aug. 28 market survey. We will publish updated lead times in this Thursday’s newsletter.

Cold-rolled coil

The SMU price range is $900–980/st, averaging $940/st FOB mill, east of the Rockies. The lower end of our range is unchanged, while the top end is down $10/st w/w. Our overall average is down $5/st. Our price momentum indicator for cold-rolled steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Cold rolled lead times range from 5-9 weeks, averaging 7.0 weeks through Aug. 28.

Galvanized coil

The SMU price range is $850–960/st, averaging $905/st FOB mill, east of the Rockies. The lower end of our range is down $10/st, while the top end is up $10/st w/w. The overall average is thus unchanged. Our price momentum indicator for galvanized steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $947–1,057/st, averaging $1,002/st FOB mill, east of the Rockies.

Galvanized lead times range from 6-9 weeks, averaging 7.3 weeks through our Aug. 28 survey.

Galvalume coil

The SMU price range is $880–970/st, averaging $925/st FOB mill, east of the Rockies. The lower end of our range is unchanged, while the top end is up $20/st w/w. Our overall average is up $10/st w/w. Our price momentum indicator for Galvalume sheet has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,174–1,264/st, averaging $1,219/st FOB mill, east of the Rockies.

Galvalume lead times range from 7-9 weeks, averaging 7.4 weeks through our latest published survey.

Plate

The SMU price range is $900–1,000/st, averaging $950/st FOB mill. The lower end of our range is down $20/st, and the top end is unchanged w/w. Our overall average is down $10/st w/w. Our price momentum indicator for plate remains pointed lower, meaning we expect prices to decline over the next 30 days.

Plate lead times range from 3-5 weeks, averaging 4.2 weeks through our Aug. 28 survey.

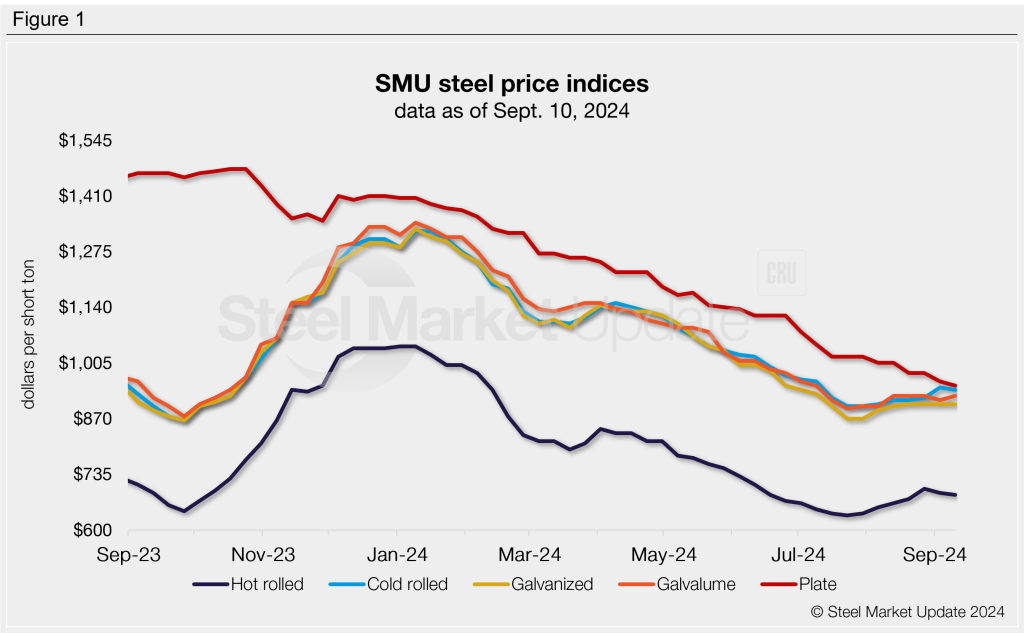

SMU note: The graphic above shows our hot rolled, cold rolled, galvanized, Galvalume, and plate price indices for the last year. For more historical data, check out the Interactive Pricing Tool on our website. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.