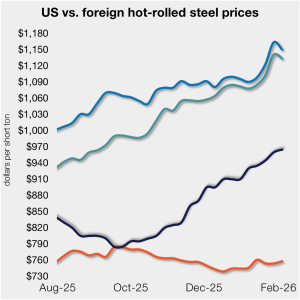

Spread between US HR prices and imports narrows

The price gap between US hot-rolled coil and landed offshore product narrowed this week, as price movements stateside and abroad diverged.

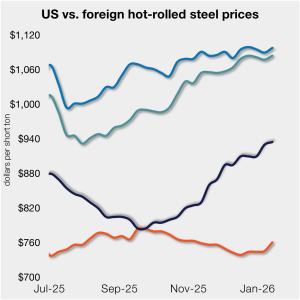

The price gap between US hot-rolled coil and landed offshore product narrowed this week, as price movements stateside and abroad diverged.

One third of the steel buyers responding to our market survey this week reported that domestic mills are negotiable on new spot order pricing. Mills began to hold a firmer stance on prices towards the end of last year, tightening their grip in early January and holding it since.

Steel mill lead times marginally declined on sheet products this week but edged higher on plate, according to responses from SMU’s latest market survey. Overall, lead times remain one to two weeks longer than levels seen three months ago.

Flat-rolled steel prices inched upward again this week as mixed demand appeared to be offset by limited supplies.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $970 per short ton, up $5/st from last week.

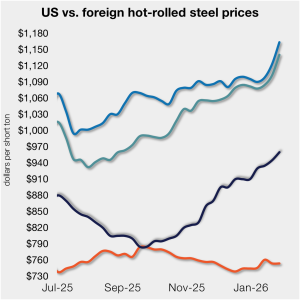

The price gap between US hot-rolled coil and landed offshore product inched higher, even as prices stateside and abroad mostly moved in tandem vs. last week.

What do SMU's latest survey results show about the current market take on tariffs and where HRC prices are going?

Sheet prices mostly continued their uneven but steady march higher this week, according to SMU’s latest check of the market.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $965 per short ton (st), up $5/st vs. the prior week.

The price gap between US hot-rolled coil (HR) and landed offshore product has been relatively flat to begin the year.

SMU’s sheet price indices climbed to new multi-month highs this week, while plate prices marginally declined.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $960 per short ton (st), up $10/st vs. the prior week.

US service centers’ flat-rolled steel supply recovered in December, after trending lower from September to November.

The price spread between domestic hot-rolled coil and prime scrap widened for a fourth consecutive month in January, based on SMU’s most recent pricing data.

The majority of SMU’s sheet and plate price indices rose this week, with multiple products climbing to new multi-month highs

Nucor’s consumer spot price (CSP) for hot-rolled coil remains unchanged at $950 per short ton (st) for the fourth consecutive week.

Sources in the domestic hot-rolled sheet market say they are standing by for an uptick in customer demand. These service center market participants, located in various regions of the US, expect to handle an influx of customer orders this month.

Mill spot price negotiation rates have tumbled across all products SMU tracks, according to our latest survey data.

Steel sheet and plate prices rose across the board to start the year on limited spot availability at some mills, expectations of higher scrap prices, and hopes of stronger demand in 2026.

Nucor kept its consumer spot price (CSP) for hot-rolled coil unchanged at $950 per short ton (st) for a third week.

Nucor kept its consumer spot price (CSP) for hot-rolled coil unchanged at $950 per short ton (st).

Nucor raised its weekly hot-rolled coil spot list price by $10 per short ton (st) this week, marking the company's ninth consecutive increase.

US Midwest sheet prices continued to rise alongside continued mill prices increases as lead times remained extended.

The price gap between stateside hot band and landed offshore product continues to narrow, inching closer toward parity. The premium is now, on average, at its lowest level since July.

Following last week’s pause, SMU’s price indices were overall steady to higher this week, holding at or near multi-month highs.

Flat rolled = 50.6 shipping days of supply Plate = 52.8 shipping days of supply Flat rolled US service centers’ flat-rolled steel supply declined for the fourth straight month, reaching 50.6 shipping days of supply on an adjusted basis at the end of November, according to SMU data. Flat roll supply is at its lowest […]

Nucor increased its weekly hot-rolled coil spot list price by $10 per short ton (st) again on Monday, Dec. 15. This was its eighth increase in as many weeks, moving up $65/st over that span.

Participants in the domestic coil market hope producer price increases indicate strong market conditions entering the new year.

Less than half of the steel buyers who responded to our market survey this week reported that domestic mills are willing to talk price on new spot orders

The price spread between hot-rolled coil and prime scrap has widened for the third consecutive month in December, based on SMU’s most recent pricing data.