Analysis

August 3, 2024

Final thoughts

Written by Michael Cowden

It might be the dog days of summer. But it’s been a newsy week for steel.

Let’s start on the trade front, where we had a big decision in a case before the Commerce Department about Vietnam’s market status. Ethan Bernard covered the news.

Commerce determined that Vietnam remained a “non-market economy,” or NME, based on factors such as government control over private property, labor conditions, and one-party rule.

What’s also notable, and which Wiley trade attorney Alan Price points out in a good column on the matter, is that Commerce’s decision cannot be appealed.

Why does that matter to your business?

There has been a rumor for a while now that domestic mills have been itching to file a trade case against coated flat-rolled steel from Vietnam. The rumor seems to be strongest among companies that produce or consume galvalume, where recent import volumes have had an outsized impact.

Government data have shown for months that imports from Vietnam have increased dramatically. Case in point: Vietnam shipped 88,840 metric ton of flat-rolled steel to the US in June, according to preliminary data from the Commerce Department. (July data aren’t yet complete.)

That’s down from 114,125 metric tons in May but more than triple the 24,219 metric tons that arrived in June 2023. Almost of all those exports from Vietnam were “other” metallic coated products (47,157 metric tons) – a category that includes galvalume – or galvanized sheet and strip (33,130 metric tons)

My understanding is that two more factors were necessary:

- Lower Q2 earnings, so that US mills could make a plausible case that they’d been hurt by imports

- Commerce determining that Vietnam is an “NME”, which should allow for the calculation of higher duty rates

Both of those conditions have been met. Cliffs barely eked out a profit in Q2. And other US mills, while still very profitable, have reported significantly lower Q2 earnings.

I’ve heard from multiple sources that a trade case could be coming soon. Exactly when remains a matter of debate. That said, we’ve already heard that some offers from Vietnam had already been pulled before the NME.

Survey says…

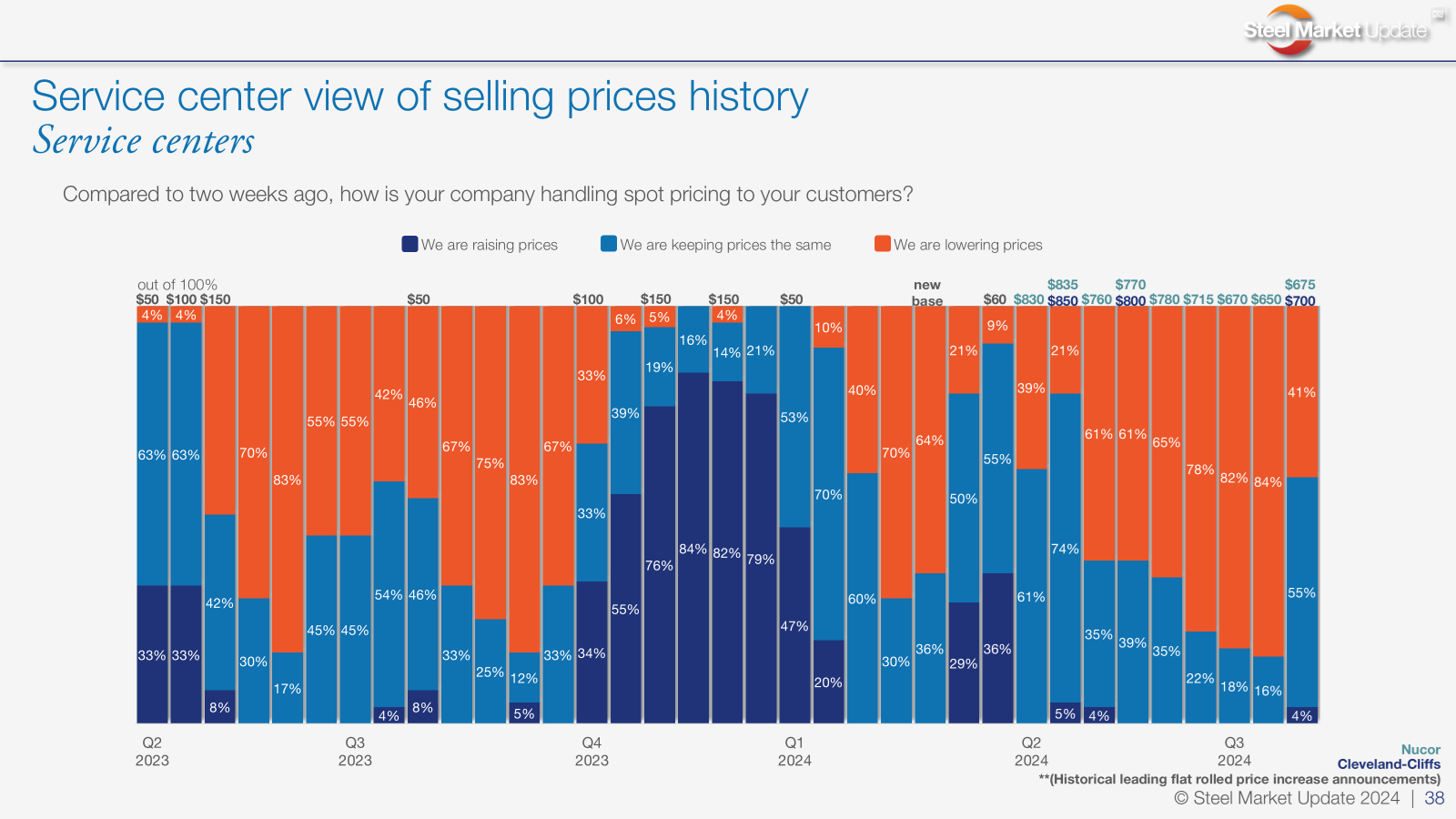

The results of SMU’s latest steel market survey are in. And we now have some data to support that recent price announcements by Nucor and by Cleveland-Cliffs should at least stop the bleeding in domestic sheet prices. Check out the chart below, which is one of my favorites. (Editor’s note: Our premium subscribers have had access to this and other survey data since Friday. Contact my colleague Luis Corona at luis@steelmarketupdate.com if you would like to upgrade your subscription from “executive” to “premium”.)

Recall that Nucor last Monday announced it was at $675 per short (st), up $25/st from $650/st previously. Cliffs then announced last Tuesday that it was at $700/st, up $30/st from $670 the week prior.

I’ve noted in recent webinars and in prior Final Thoughts that when you see ~85% of service centers lowering prices, it’s not uncommon to see mill increase prices shortly thereafter. It is what our founder, John Packard, called the point of capitulation – when buyers are just as eager as mills to see higher prices.

Sure enough, that rule of thumb held true again. In our last survey, 84% of service centers respondents reported that they were lowering prices. A little over a week later, the mill increases started coming.

Sure, only 4% of service center respondents say that they’re increasing prices along with mills. It will be important to watch whether that number increases in our next survey – which would indicate that mill hikes were actually sticking.

But it’s important that 55% of service centers say they are keeping prices unchanged. That’s already a huge change from the last few months, when most centers were lowering prices.

A solid floor, and a lower ceiling

What’s also notable is that most people don’t expect prices to go soaring upward as they have in past upcycles. The chart below shows where survey respondents think prices will be in early October.

The vast majority of those we surveyed (88%) think HR prices will be roughly where they are now or higher in early Q4. Only 8% think they’ll fall below $600/st. And only 4% think they’ll get above $750/st.

Here is what some of them had to say:

“Demand will start to recover a bit. Supply increases over the past couple of years will, however, keep prices low.”

“Imports are basically quelled. Inventories have been recalibrated at the new pricing. And some restocking is expected.”

“Nobody has been buying for months. We’ll see a couple-month bump. It just won’t be very large.”

“I feel we have hit bottom and will see small increases – nothing significant though because demand isn’t strong enough to back it up.”

“It won’t go back up too fast – no demand.”

My question: If we are returning to pre-pandemic era mini-cycles, is ~$600-750/st the new bandwidth for HR?

Also, where did the demand go?

Notice there is a persistent theme of concerns about demand. That’s in the news – whether it’s layoffs at Stellantis, cuts at John Deere, or a lackluster jobs report.

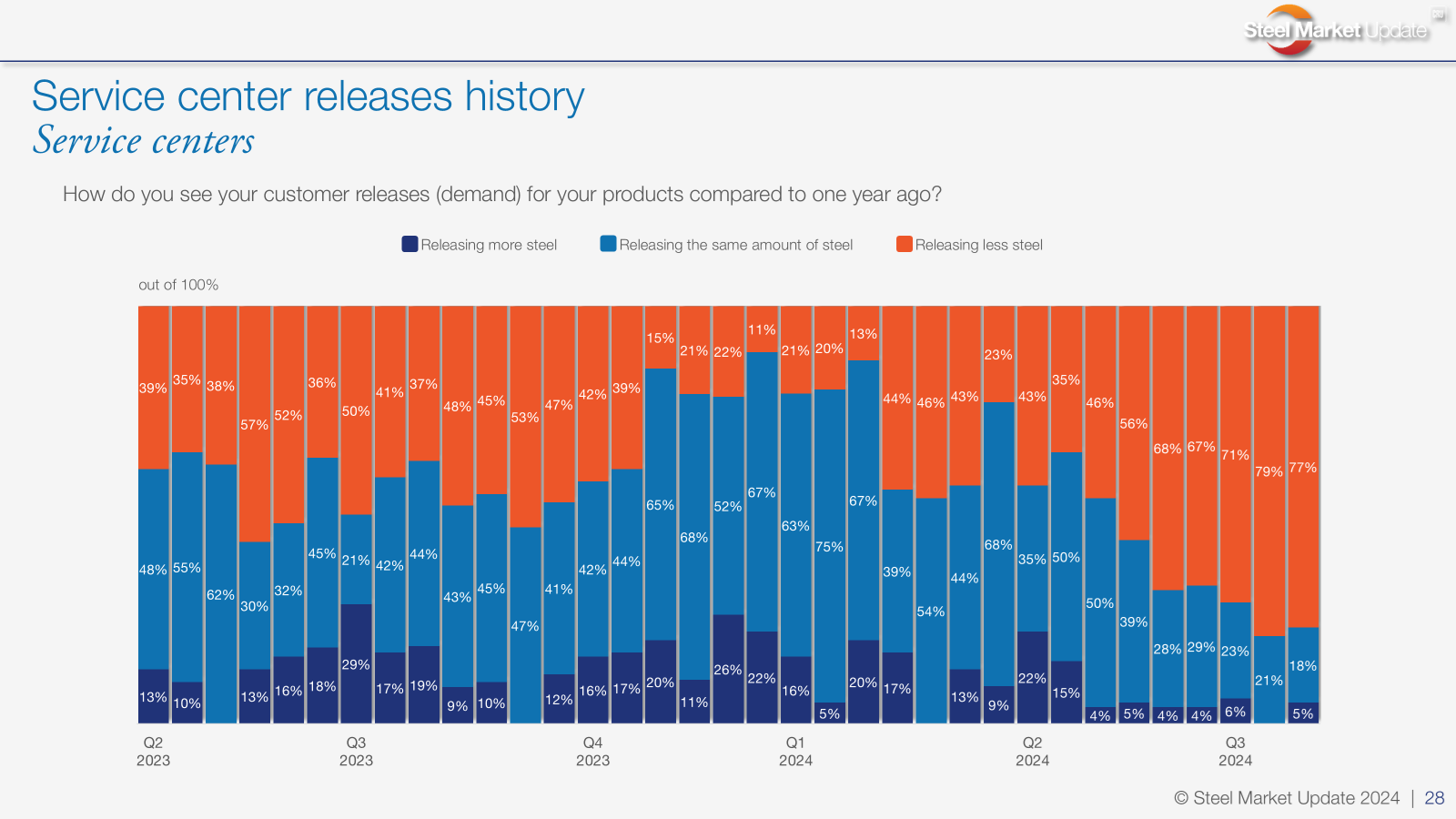

We also see it on our data too. Check out the chart below:

True, most service centers are keeping prices steady or increasing them. But nearly 80% report that they are releasing less steel than a year ago. And that trend hasn’t changed (or hasn’t’ changed yet) despite recent mill price increases.

What do you think might turn that trend around? Or is it more about learning to live with lower demand for the time being? Let us know your thoughts at info@steelmarketupdate.com.

SMU Steel Summit – almost 1,300 and counting

Nearly 1,300 people have registered for Steel Summit on Aug. 26-28 at the Georgia International Convention Center (GICC) in Atlanta. That means we remain on track to meet (maybe exceed?) last year’s record attendance.

If you’re not familiar with Summit, Brett Linton, whose has been with SMU since the beginning, wrote a good history of the event. It’s a testament to what Packard, the SMU OGs, the current SMU staff, and our CRU colleagues have accomplished.

It’s also testament to the support so many of you have provided to us over the years – in strong markets, weak markets, and even when the pandemic forced Summit to go virtual. You can learn more about Summit here and register here. And to everyone who is already going – THANK YOU. We look forward to seeing you soon!