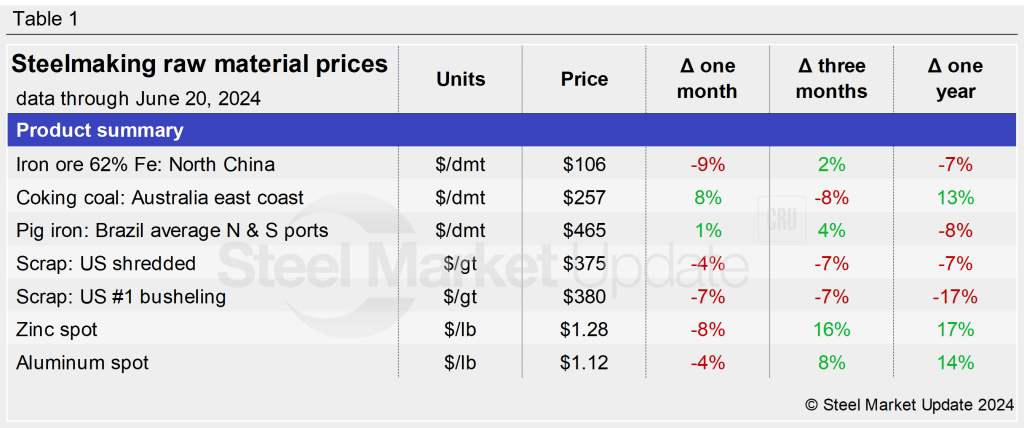

Market Data

June 21, 2024

Majority of steelmaking raw material prices ease through June

Written by Brett Linton

Steelmaking raw material prices have generally declined over the past month, according to SMU’s latest analysis.

As of June 21, prices for iron ore, zinc, aluminum, and steel scrap have all eased by 4-9% month on month (m/m). Pig iron saw a slight increase from May to June, while coking coal prices rose by 8%.

Raw material prices show mixed changes compared to three months prior, with some up as much as 16% (zinc) and others down by 8% (coking coal). Table 1 summarizes the percentage changes from one month, three months, and one year ago for each product.

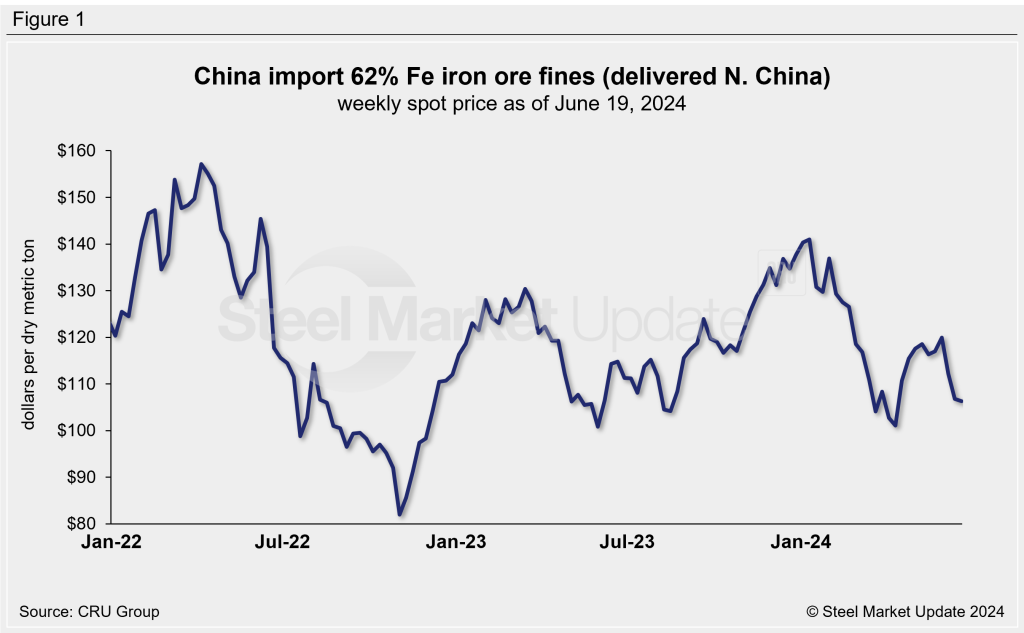

Iron ore

Following April’s rebound, the import price of 62% Fe Chinese iron ore fines have trended downward throughout June. The latest weekly spot price is $106 per dry metric ton (dmt) delivered North China. Iron ore prices have fallen 9% over the past month and are now at a 10-week low, just slightly above the 2024 low of $101/dmt seen in mid-April. Iron ore prices are 7% lower than levels seen this time last year.

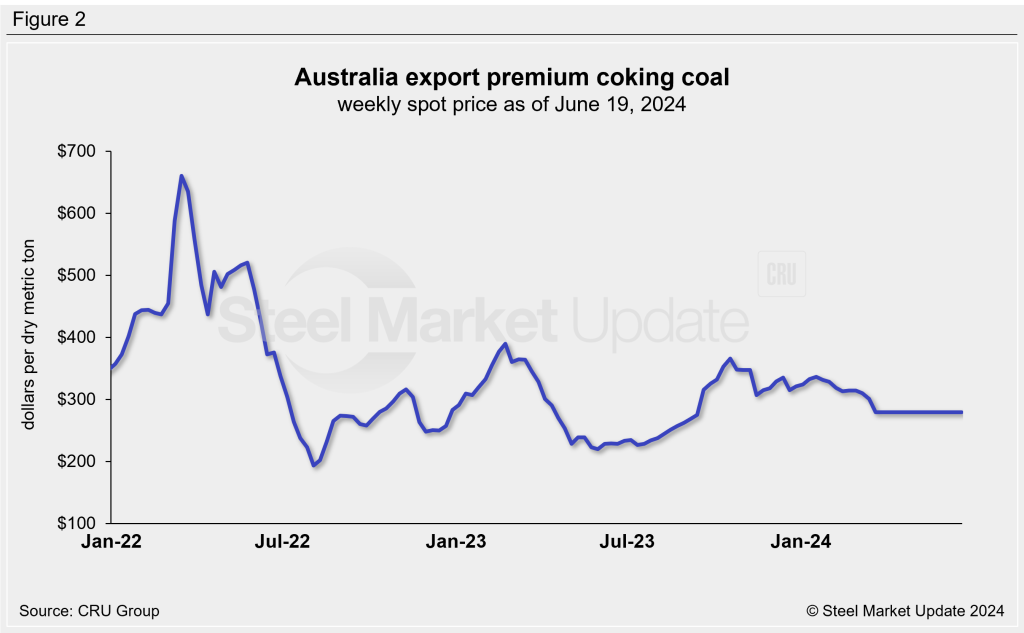

Coking coal

Prices for premium hard coking coal increased over the last month after a decline earlier in the year. The latest weekly price is up to a three-month high of $257/dmt. Coking coal prices have risen 8% in the last month but remain 8% lower than levels three months ago. Prices are 13% higher than they were this time last year.

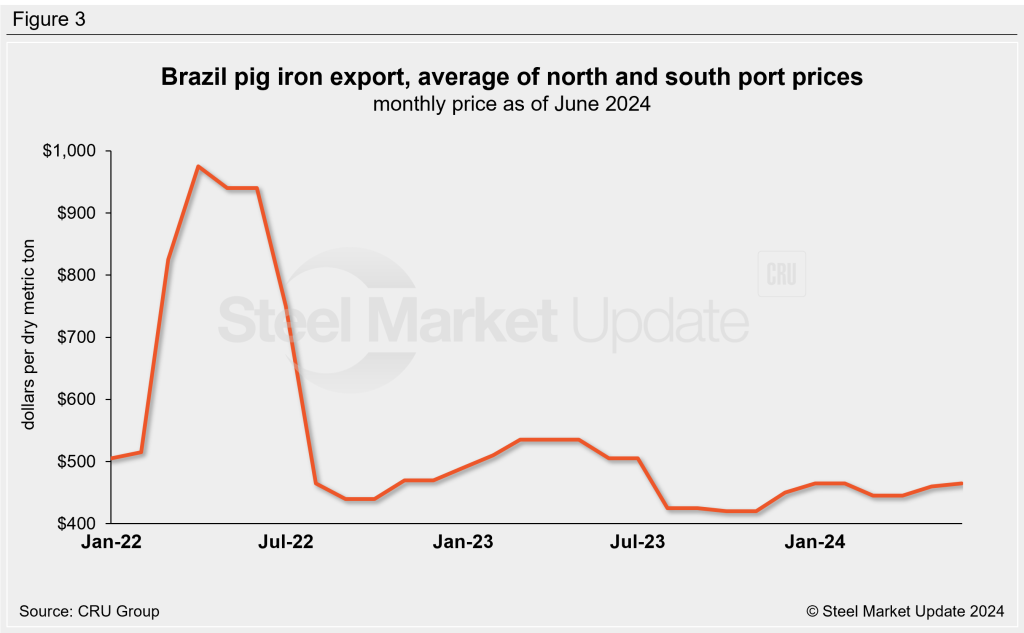

Pig iron

Since stabilizing last August, pig iron prices have been on an upward trend for the past seven months. Prices ticked 1% higher from May to June to a four-month high of $465/dmt. Pig iron prices are 4% higher than three months prior but 8% lower than levels seen this time last year. Recall that pig iron prices had jumped more than 60% in April 2022 following the invasion of Ukraine by Russian forces, reaching a historic high of $975/dmt.

Note: Most of the pig iron imported to the US had come from Russia, Ukraine, and Brazil. This report uses Brazilian prices and averages the FOB value from the north and south ports.

Scrap

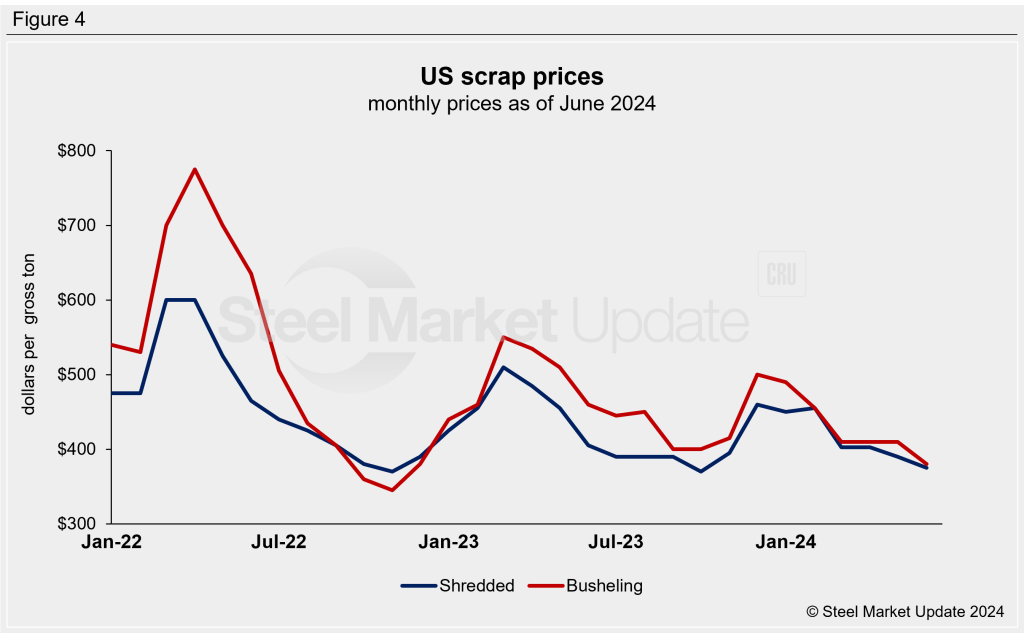

Steel scrap prices have eased throughout 2024 following their peak last December. SMU’s busheling scrap index eased 7% m/m in June to a 1.5-year low of $380 per gross ton (gt). Shredded scrap also eased by 4% in June, now sitting at an eight-month low of $375/gt. Scrap prices are down 7% compared to levels three months ago and are 7-17% lower than tags seen this time last year.

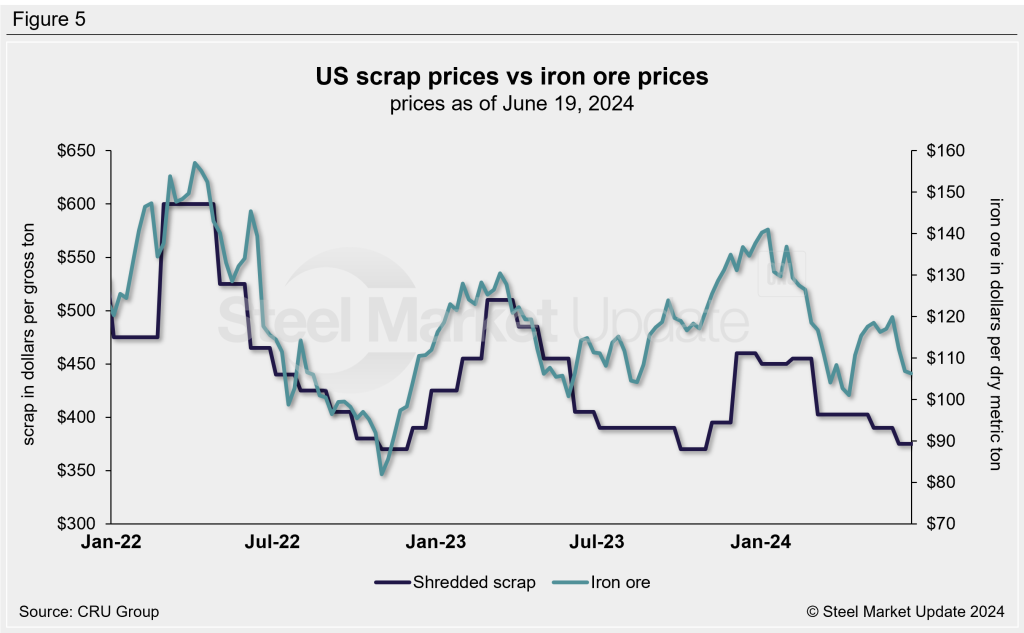

Changes in the relationship between scrap and iron ore prices offer insights into the competitiveness of integrated mills, whose primary feedstock is iron ore, compared to mini-mills, where the primary feedstock is scrap. Figure 5 shows the prices of mill raw materials over the past three years.

To compare these two feedstock materials, SMU divides the shredded scrap price by the iron ore price to calculate a ratio. A high ratio favors the integrated producers and a lower ratio favors the mini-mill/EAF producers (Figure 6).

Integrated producers had mostly held the cost advantage from late-2021 through mid-2023. The advantage then briefly shifted to EAF producers, but began moving higher last December. The ratio as of June 19 is currently in relatively neutral territory at 3.52.

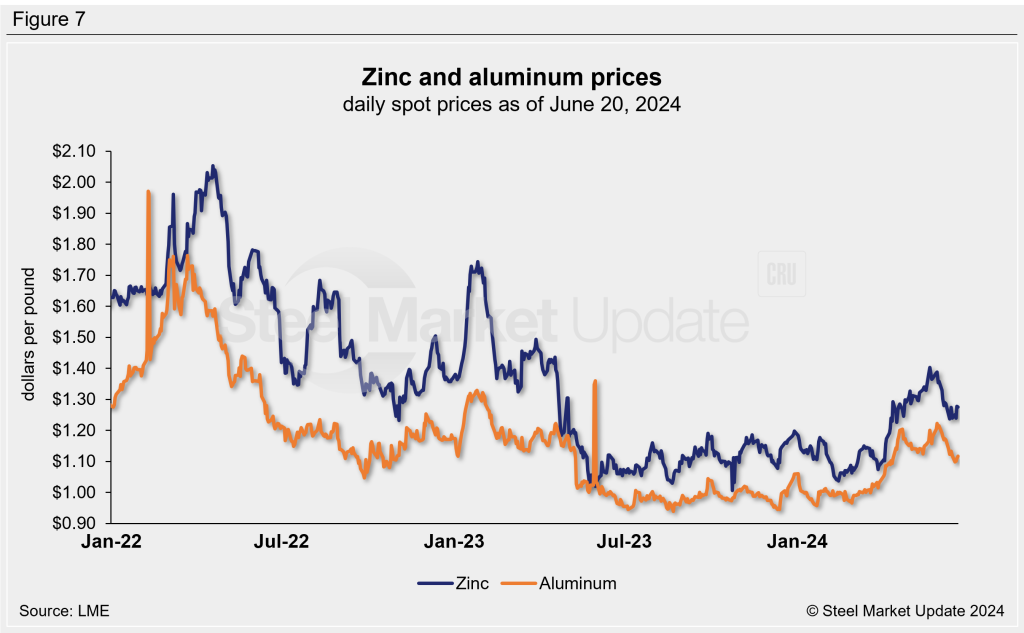

Zinc and aluminum

Zinc is used in galvanized and other coated steel products. Following the multi-year lows seen last summer, spot prices leveled out around this time last year and were relatively stable through mid-April. After surging in late April to reach a 13-month high in late May, the latest LME cash price for zinc has eased 8% m/m to $1.28 per pound. The April/May surge had prompted some mills to increase their galvanized coating extras. Zinc prices are 16% higher than levels three months prior and up 17% from June 2023.

Aluminum prices, which factor into the price of Galvalume, had also stabilized in mid-2023. Prices began to pick up steam in late-March and climbed to a one-year high of $1.22/lb in late May. The latest LME cash price has eased 4% m/m to $1.12/lb. Aluminum prices are 8% higher than tags three months prior and 14% greater than levels this time last year. Note that aluminum spot prices sometimes have large swings and return to typical levels within a few days, as seen in Figure 7.