Analysis

May 28, 2024

Final thoughts

Written by Laura Miller

We trust you had a safe and enjoyable long holiday weekend and unofficial start to the summer.

Sure, sunshine and vacations are on our minds, too. But now it’s time to ground ourselves back into the wonderful world of steel.

Let’s take a collective deep breath ::in:: and ::out::…

And we’re back. But where exactly are we? Are steel prices going up or down? Is demand really decelerating or is it an illusion? How is the market navigating the new mill pricing mechanisms?

The latest results of SMU’s full steel buyers’ survey can help provide some insight here. Let’s take a look at some of the results and responses in each buyer’s own words.

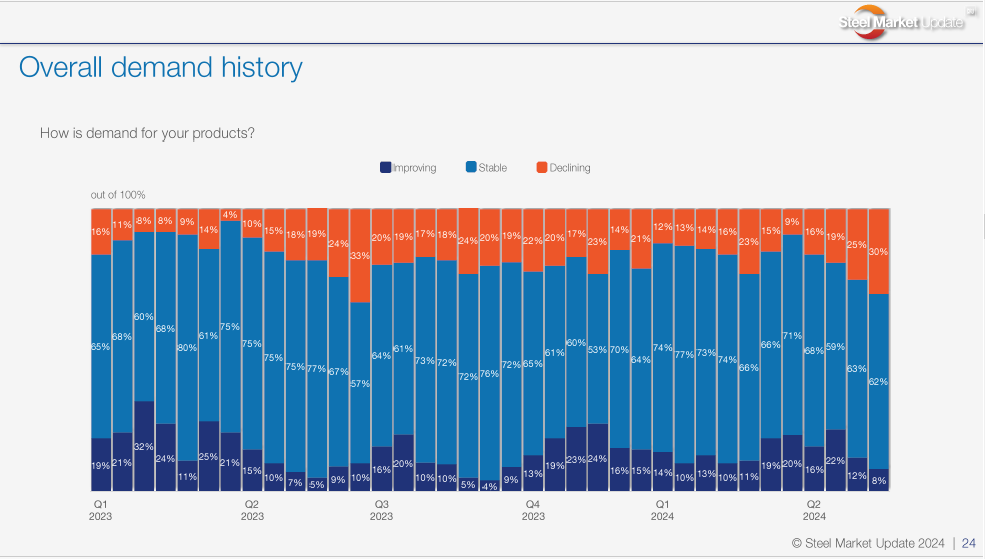

Starting with the driver of it all—demand. While the majority of buyers reported stable demand, nearly a third of buyers are now reporting declining demand – that’s the highest that metric has been since the end of Q2 last year.

How is demand for your products?

“Summer seems to have started early, still waiting for infrastructure money to trickle down, uncertainty with election.”

“Demand is steady but somewhat down.”

“Seeing things very soft.”

“Declining transactionally due to pricing pressure.”

“High interest rates are slowing our demand.”

“Near-term spot buying is dead and expect June to be a tough month on contracts with buyers knowing July will be cheaper.”

“Stable to declining due to falling prices. It’s killing the plate market.”

“Still good on OEM side; slightly offset by spot buyers being cautious and buying small amounts.”

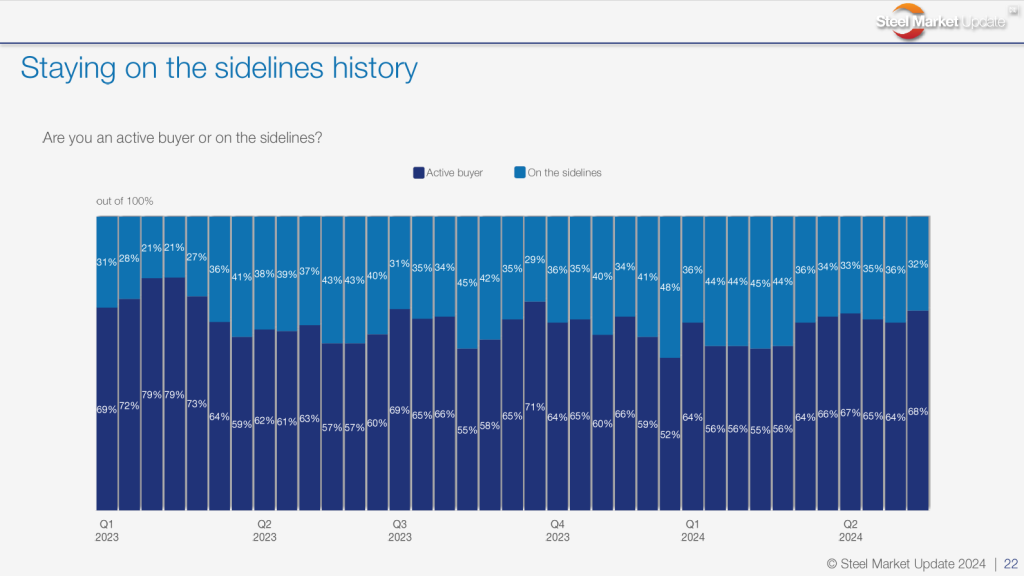

Are you an active buyer or on the sidelines, and why?

“Slowing down but still buying.”

“If HR gets to $700 with CRU discounts, I think most service centers load up. “

“Actively buying contract tons.”

“Infrastructure growth.”

“Current inventories are in balance and now buying to meet demand.”

“Reorder point.”

“We need to fill the shelves no matter what price.”

“Approaching the sidelines.”

“Preparing for the bottom, which is nearing.”

“No reason to buy, with (1) our focus being on controlling cash and (2) our belief that the market still has room to go down.”

“Riding the decline wave, keeping my Q2/Q3 contracts in my back pocket for later.”

“Demand softening.”

Moving on to the thing that connects us all… steel prices! And where buyers think they are headed in the coming months:

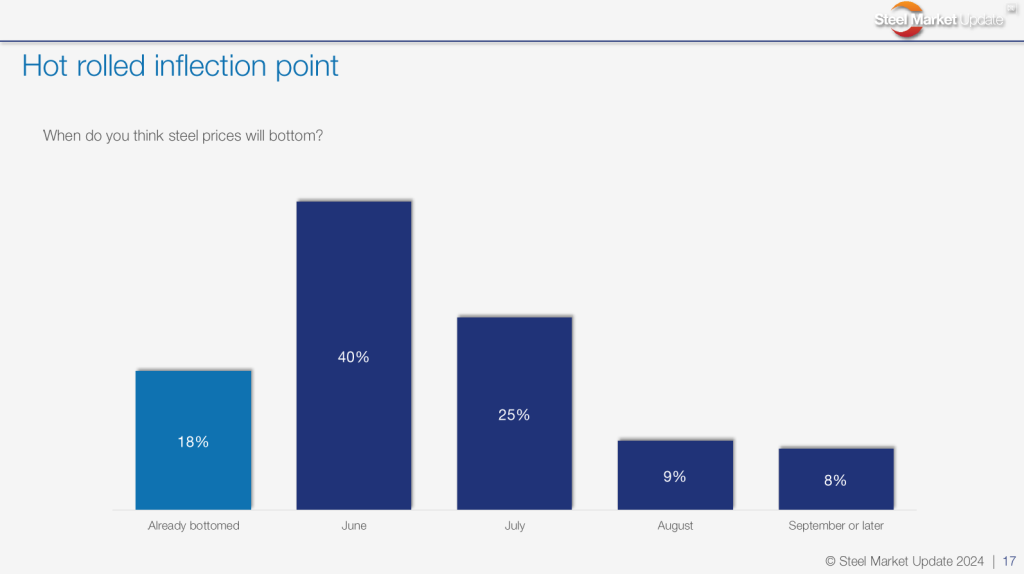

Prices have been moving lower. When do you think sheet prices will bottom, and why?

Already bottomed:

“World prices are starting to increase now. US mills will do the same.”

“I believe we are near the bottom now, and demand should increase for the summer.”

June:

“When the mills announce increases, it will take a few weeks to stop the slide. “

“I don’t think the mills are going to let it get much lower. I suspect (barring catastrophic economic/international issues) that supply will adjust to demand and decrease production to stabilize pricing.”

“Demand is weakening, and then summer doldrums will hit on top of that. Higher interest rates seem to be finally hitting the economy.”

“Demand is weak and supply of inventory is still good.”

“Seems like buyers are still pushing down, and some mills will need to do a deal or two to get through June order book.”

July:

“Still a lot of inventory.”

“Lower prices will influence inventory decisions; anticipation of seasonal incline; what seems to be the common/prevailing industry/economic forecast going into Q4; and it’s an election year.”

“We aren’t expecting anything drastic, but definitely fluttering downward over the next month to somewhere at/slightly below $700/ton.”

“Eventually folks will need to buy more than just what they are to fill holes.”

August:

“Further downward pressure due to economy, will rise ahead of 2025 auto contracts.”

“Slower demand, interest rates slowing purchases.”

September or later:

“Going to be a slower than anticipated summer.”

“Foreign steel is coming in and demand seems relatively stable. Our guess is that prices will bottom in Q4.”

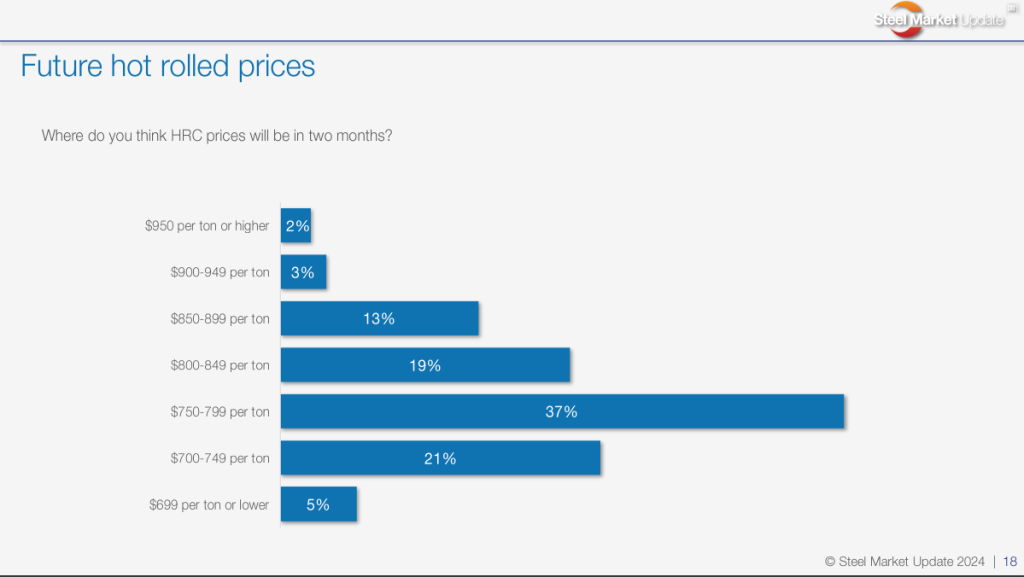

Hot rolled coil prices averaged $775 per short ton in our last market survey. Where will prices be in two months?

$850-899/st:

“Demand will remain soft overall for the remainder of 2024. I don’t see mills getting numbers above $900.”

“Imports will be soft coming to the US over the summer and prices should increase.”

$800-849/st:

“We seem to be hovering at the bottom.”

“Outages and lack of imports. Demand is still solid.”

“That seems to be the new ‘normal.’”

“Although I think Cliffs will aim for a higher number, Nucor may ultimately try to eliminate a large run up with their CSP.”

$750-799/st:

“Labor costs and other operational costs are too high.”

“I think inventories are low enough to keep customers buying, yet supply and demand seem in balance.”

“Seasonality and excess inventory.”

$700-749/st:

“We will be starting to come back up from the bottom due to restocking.”

“Mills will try to make money on volume not margin and will look to buy demand.”

“I see it coming down a bit more before it rebounds.”

“Offshore orders are still coming in and demand is weak.”

$650-699/st:

“Slowdown across the board.”

“Demand has slowed down a bit. “

And like it or not, the industry is still chattering away about the new mill pricing mechanisms announced by Nucor and Cleveland-Cliffs last month. They’ve taken us on quite the ride, and it doesn’t appear to be stopping anytime soon.

What are your thoughts on Nucor’s weekly public HRC price?

Neutral:

“I don’t think it has much of an impact. Other mills have offered lower numbers. “

“Still too early to tell, has seemed to be more of a ‘monthly’ range so far.”

“Not sure how long that will last. Seems to go against the grain. Will service centers reduce inventories to avoid getting ‘caught’ by the CSP rollercoaster? 3-5 week lead times are great, but is it sustainable?”

“We will see if mills start needing to undercut themselves.”

“Too early to tell what their objective is. They have definitely created headlines.”

“Still like it but for it to be successful volume will need to be readily available.”

“’Neutral’ for us, but it has certainly stunted any upward mobility in the coil market.”

“I like that the mill is being transparent with what you can actually buy at, but I am struggling with what their goal is.”

Negative:

“CSP being taken as a price index while it’s a mill price. It is having too much influence on the market. Creating more fluctuation while it was designed to remove it or said to remove it.”

“Been a total decline in prices since it started.”

“This will only further commoditize our market.”

“I believe it is negative because it causes more speculation than certainty among buyers on a weekly basis.”

“This week’s increase seems to be contrary to what everybody is saying, and there is no transparency to how they are coming up with their numbers. If they were trying to be a better market indicator than the CRU, they are failing.”

“It has served to create more volume volatility (not less as they suggested) and more price variability and speculation thus far. And we do not believe that their sales people have effectively communicated to buyers either.”

What are your thoughts on Cliffs’ monthly public HRC price?

Positive:

“I believe a monthly price is more accurate than a weekly price.”

Neutral:

“Still too early to tell, has seemed to be fairly irrelevant so far.”

“It’s a mill price. Nothing new here.”

“We will see if mills start needing to undercut themselves.”

“Assume they will update weekly in the future to stay relevant.”

“I like them being transparent, but a monthly number vs. a weekly number is meaningless most of the time.”

Negative:

“This will only further commoditize our market.”

“Either do it at the same periodicity to Nucor and the CRU or get rid of it.”

“When they do what they say, then maybe we’ll believe it.”

I must express my gratitude to the steel universe, but mostly to the buyers regularly participating in SMU’s surveys. Thanks for sharing your insights and for enlightening the SMU community!

Wednesday’s Community Chat

On Wednesday, SMU Managing Editor Michael Cowden will connect with Spencer Johnson, head of ferrous trading at StoneX, to talk about the steel futures markets. Register here and don’t miss what’s sure to be an interesting conversation.

Join us for steel’s unofficial end to summer

Meditating is the answer for many things, but I’m not sure meditating on steel prices is the answer to where prices are heading. So before you take off and get lost in your summertime fun, remember to secure your spot for the SMU Steel Summit. North America’s largest meeting of the flat-rolled steel industry will provide valuable insight into pricing and the industry as a whole. We hope you’ll join us in Atlanta in August!

As always, thank you for allowing Steel Market Update to be a part of your journey navigating the great mystery of steel!