Prices

May 23, 2024

HR futures: Sideways and range-bound

Written by Mark Novakovich

Sideways and range-bound describes the US steel derivatives market over the past week, though the monthly picture shows a more notable decline in front-end flat prices.

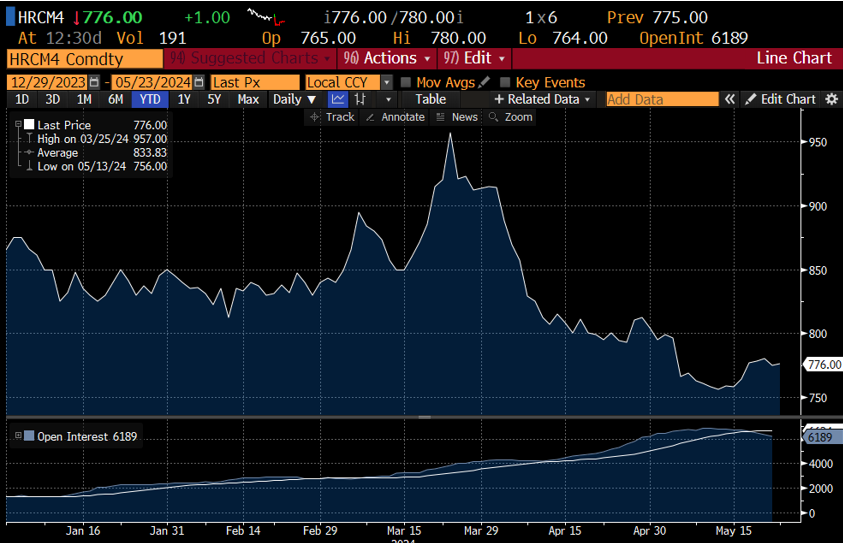

Week-over-week saw the June futures contract firm slightly, from $770 per short ton (st) to $780/st as of Thursday, May 23’s provisional close. However, the contract was down by $45/st from April’s high of $825/st on April 29.

Nucor’s lower CSP on May 13,, at $760/st, weighed on market sentiment but was said to reflect the reality that physical tonnage was trading hands in the low-to-mid $700 range. Lead times were also said to be manageable, with some June capacity still alleged to be available.

A higher Nucor CSP on May 20, at $770/st, provided a brief respite to the bearish futures trend but failed to be a meaningful catalyst to drive futures higher.

Cleveland Cliffs’ July base price, released on May 23 at $800/st, was lower by $50/st from its April price, but early reaction was mixed and inconclusive at the time of this story’s submission.

Overall trading activity in CME HRC futures has been quiet, with daily transacted volumes failing to break 20,000 st since May 9, with the trailing five-day average volume around 15,000 st. Open interest has increased slightly over the course of the month, rising from approximately 500,000 st to 540,000 st. Many commercial participants remain on the sidelines, but financial participants have had interest on both sides of the market.

Base metals, particularly copper and the LME/CME copper arbitrage, have seen historical volatility over the past several weeks. The rally has attracted broader interest from macro- and commodity-focused funds in the metals complex as a whole, including ferrous.

Much of the recent activity has been a large nearby position rolling from June to July, with nominal trading in deferred quarters, though the Q3’24 and Q4’24 succumbed to recent pressure and have declined to flatten the overall futures curve structure, albeit on low volumes.

The beginning of May saw an $80 contango develop from June to December futures, but at the time of this article’s writing, the spread from June to December had narrowed to $50/st and was said to be somewhat unattractive for many cash-and-carry players.

Overall, many market participants are awaiting a catalyst that breaks prices out of their tight, range-bound pattern.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed should not be treated as a specific inducement to make a particular investment or follow a particular strategy. Views and forecasts expressed are as of date indicated. They are subject to change without notice, may not come to be, and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.