HR Futures: Rangebound amid muted summer trade

Since the last writing of this article, CME hot-rolled coil (HRC) futures have been largely steady and lifeless, though there’s been some brief bouts of intraday volatility.

Since the last writing of this article, CME hot-rolled coil (HRC) futures have been largely steady and lifeless, though there’s been some brief bouts of intraday volatility.

After a hot start to June, the CME ferrous derivatives complex has cooled down.

A fierce flat price rally started this week that saw the nearby months rally by over $120/ short tons, exceeding the contract highs seen in February ahead of the first batch of tariffs.

Despite the hand-wringing and head-scratching about the impact of President Trump’s tariff policy, the HRC futures market has been relatively subdued since our last writing of this article.

A look at the HR futures market.

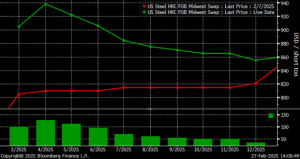

It’s been an event-filled month in US ferrous derivatives markets since my last column for SMU. There’s been no shortage of writings and musing about the ongoing steel and aluminum tariffs proposed by the Trump administration. And steel and scrap futures markets have responded accordingly. CME HRC futures prices have risen, and the curve has firmed. The February 2025 HRC futures contract, now in the pricing period, has added $47 per short ton (st) since its contact lows on Jan. 20 to settle at $767/st today.

US ferrous derivatives markets were largely quiet through the holiday period. Since the new year, however, we have seen a bit of a resurgence in interest as traders and sales staff return to their desks.

After experiencing a rally ahead of the 2024 election, the nearby part of CME HRC futures complex has softened as we approach year-end. Meanwhile, the forward positions (second half of 2025) have remained supported and largely unchanged.

Despite a higher settle today on CME hot-rolled coil (HRC) futures, the pattern over the past four weeks has seen nearby steel futures prices drift lower, while the back of the 2025 curve has remained supported.

It had been a relatively quiet and steady CME HRC futures market since the end of August. That was upended by Thursday’s news that instead of a two-week maintenance outage, Cleveland-Cliffs would hot idle the C-6 blast furnace at its Cleveland Works for an uncertain period of time. The CME October HRC contract, HRCV4, gained $22 per short ton (st) on the day to provisionally close at $744/st on Thursday. The first and second quarter futures strips of 2025 gained $25/st and $24/st to provisionally settle at $823/st and $829/st, respectively.

The front end of CME hot-rolled (HR) coil steel futures contracts had drifted lower when this article was filed on Thursday afternoon. And the back end of 2024 had also come under pressure. Despite staging a late-month rally at the end of July back into the low $700s per short ton (st) range, the lead […]

The CME steel futures complex saw a slight decrease in activity from levels seen at the end of June. This has coincided with a notable decline in flat prices for the nearby futures contract, now August HRC, which is lower by $81 per short ton (st) since last writing on June 13. It settled at $672/st on July 17.

Trading activity for the CME HRC futures contract has been sporadic so far in June, with a few days seeing transacted volumes exceed 25,000 short tons (st), but overall activity remains muted. This follows a pattern that emerged over the course of May.

Sideways and range-bound describes the US steel derivatives market over the past week, though the monthly picture shows a more notable decline in front-end flat prices. Week-over-week saw the June futures contract firm slightly, from $770 per short ton (st) to $780/st as of Thursday, May 23’s provisional close. However, the contract was down by […]

Week-over-week trading activity in US steel derivatives markets was relatively muted, with prices maintaining their downward direction since the beginning of the month. Bids have materialized at the lower end of this range in the May, as the nearby backwardation continues to roll on - just as we saw with April being a premium over May.