Prices

April 30, 2024

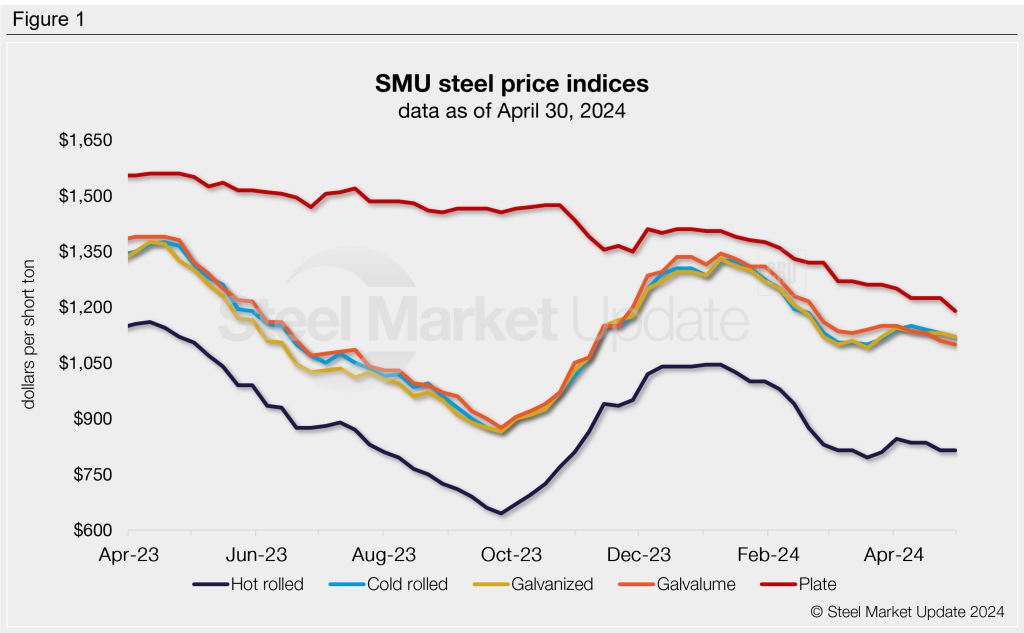

SMU price ranges: HRC flat, other products slip

Written by Brett Linton & David Schollaert

Sheet prices were flat or moderately down again this week – underscoring the shift in momentum we’ve seen over the last month. The exception was hot-rolled (HR) coil, which was largely unchanged from last week.

SMU’s average HR coil price remains at $815 per short ton (st), sideways week over week (w/w). Our average cold-rolled coil price is $1,120/st (down $10/st w/w). Our galvanized base price is $1,120/st on average (down $10/st w/w), while our Galvalume price now stands at $1,100/st on average (down $10/st w/w).

Market participants told us buying was still largely hand-to-mouth, with buyers filling inventory holes only as needed. Outlooks vary. Some sources think that published prices by Nucor and Cleveland-Cliffs will result in less volatile pricing swings. Others think those prices could push prices lower in the near term.

Average plate tags this week dropped $35/st from last week to $1,190/st. The decline resulted largely from a $90/st price cut by Nucor with the opening of its June order book.

SMU’s sheet price momentum indicators remain at neutral. Our plate price momentum indicator has shifted from neutral to lower.

Hot-rolled coil

The SMU price range is $780-850/st, with an average of $815/st FOB mill, east of the Rockies. The lower end of our range decreased $5/st w/w and the top end rose $5/st. Our overall average is unchanged compared to last week. Our price momentum indicator for HR remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Hot rolled lead times range from 3-7 weeks, averaging 5.0 weeks as of our April 24 market survey.

Cold-rolled coil

The SMU price range is $1,080–1,160/st, with an average of $1,120/st FOB mill, east of the Rockies. The lower end of our range is $20/st lower w/w, while the top end was unchanged. Our overall average is down $10/st from the previous week. Our price momentum indicator for CR remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Cold rolled lead times range from 5-10 weeks, averaging 7.5 weeks through our latest survey.

Galvanized coil

The SMU price range is $1,080–1,160/st, with an average of $1,120/st FOB mill, east of the Rockies. The lower end of our range is $20/st lower w/w, while the top of our range is unchanged. Our overall average is $10/st lower than last week. Our price momentum indicator for galvanized remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,177–1,257/st with an average of $1,217/st FOB mill, east of the Rockies.

Galvanized lead times range from 5-10 weeks, averaging 7.3 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,060–1,140/st, with an average of $1,100/st FOB mill, east of the Rockies. The lower end of our range declined $20/st w/w, while the top end was unchanged. Our overall average is down $10/st compared to the previous week. Our price momentum indicator for Galvalume remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,354–1,434/st with an average of $1,394/st FOB mill, east of the Rockies.

Galvalume lead times range from 7-9 weeks, averaging 7.6 weeks through our latest survey.

Plate

The SMU price range is $1,140–1,240/st, with an average of $1,190/st FOB mill. The lower end of our range declined $20/st w/w, while the top end dropped $50/st. Our overall average was down $35/st from last week. Our price momentum indicator for plate has been adjusted to lower, meaning we expect prices to decline over the next 30 days.

Plate lead times range from 4-7 weeks, averaging 5.7 weeks through our latest survey.

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton