Plate

March 8, 2024

Plate report: Price cuts slow buying activity

Written by David Schollaert

The US plate market has been largely quiet over the past week since Nucor’s $90-per-ton price cut at the close of February.

Sources have categorized demand as stable at best. And Nucor’s latest price notice did little to spur business, sources told SMU. While the price gap between hot-rolled coil (HRC) remains well below recent highs, buyers seem willing to hold out in the hope of further decreases.

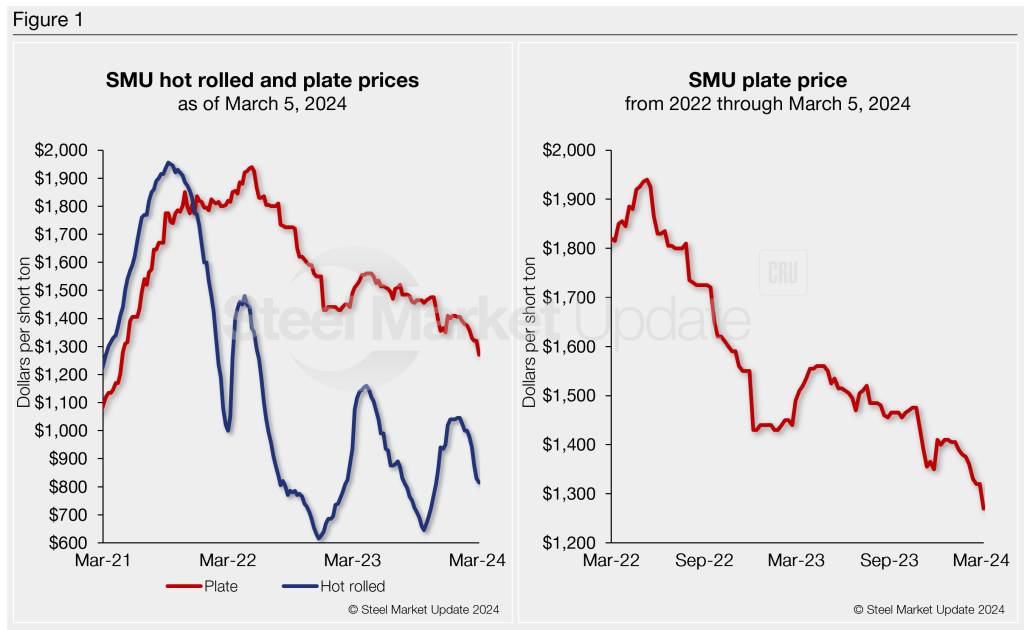

Case in point: SMU’s plate price stands at $1,270 per short ton (st) on average, down $50/st from last week and down $140/st from a recent high of $1,410/st in late December. (Figure 1, left-side chart). Our HRC price is $815/st, down $15/st from last week and down $230/st since reaching a recent high of $1,045/st at the start of the year.

But even though plate prices have seen less volatility swings vs. HRC, plate tags have been largely trending down since peaking at $1,940/st back in May 2022 (Figure 1, right-side chart).

Market reaction

The lack of stability has slowed the market because buyers are waiting for the decreases to stop while trying to run through high-cost inventories.

With little in the way of spot demand, some expect the next plate pricing announcement could be down again – a trend that could be supported should scrap settle lower in March.

SMU spoke with several plate market participants about the current state of the market.

“The announcement killed the market,” a distributor source said. “Nucor is getting the blame from everyone. But they were just responding to what the other mills were doing and what the street price is from some service centers.”

“All [the mills are] guilty parties for driving the discrete plate prices down,” said a source. He predicted that the downtrend could continue “for too many reasons to list.”

“I don’t think anyone is buying at $1,290/st FOB mill,” said a steel buyer. “There’s more supply than demand at the moment. So unless something changes, it looks like spring will be tough sledding, and then the typical summer slowdowns.”

More of the same?

So, what’s ahead? In the interim, most suggest more of the same: Limited spot activity and mills leaning heavily on contract business. Service centers and distributors, meanwhile, are cutting prices – which could continue the downward cycle.

Some speculate that as other plate suppliers have followed Nucor’s move, the next 60-90 days are likely to be challenging.

“What I thought would be a better year over 2023 by 8-10% is now looking to be the exact opposite to me and probably down 10-15% year over year,” another steel buyer said. “We’ll see, but the cards are starting to stack up against the market with each passing month and announcement.”

The takeaway

With spot plate demand limited, sellers have been discounting and undercutting published mill prices. That trend is expected to continue. And service centers need to work down inventory after ending 2023 on the high side relative to last year’s high watermark.

Most are still focused on controlling order books; another price cut could highlight that trend. But if lower tags don’t ultimately attract some buying, mills could turn back output and then raise prices to draw in buyers.

Imports aren’t as attractive as they had been, but offshore product is still running well below domestic levels, presently $1,140/st at depots. Plate for early-to-mid Q2 delivery from South Korea and Thailand is sub-$1,100 per ton, according to several sources.

It’s important to keep an eye on discrete plate lead times. While they had been a bit inconsistent earlier in Q1, the latest data suggest they are nearing the five-week mark on average and trending lower – nearing four weeks or less in some cases.