Market Segment

November 28, 2023

October imports inch higher, but flat rolled at a six-month low

Written by David Schollaert

The increase in steel imports from September to October was higher than license applications had suggested earlier this month.

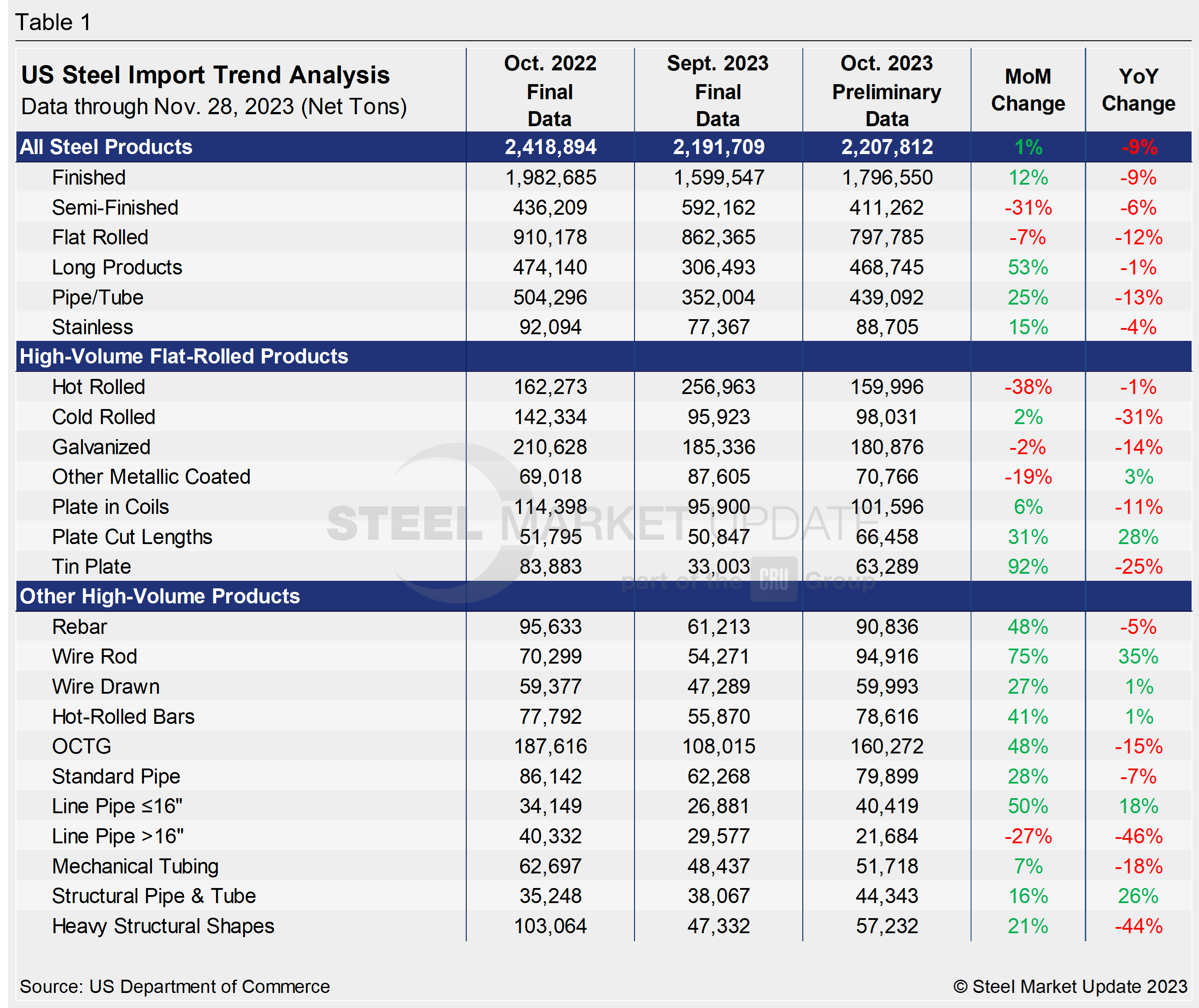

Total steel imports

Steel imports totaled 2,207,812 net tons (2,002,896 metric tons) in October’s preliminary count, according to the US Steel Import Monitor maintained by the Department of Commerce’s International Trade Administration.

October’s total is an increase of 0.7% over September’s imports of 2,191,709 tons but nearly 9% below October 2022’s imports of 2,418,894 tons.

License application data for October previously suggested imports were down marginally from September and were more than 12% below the same month last year.

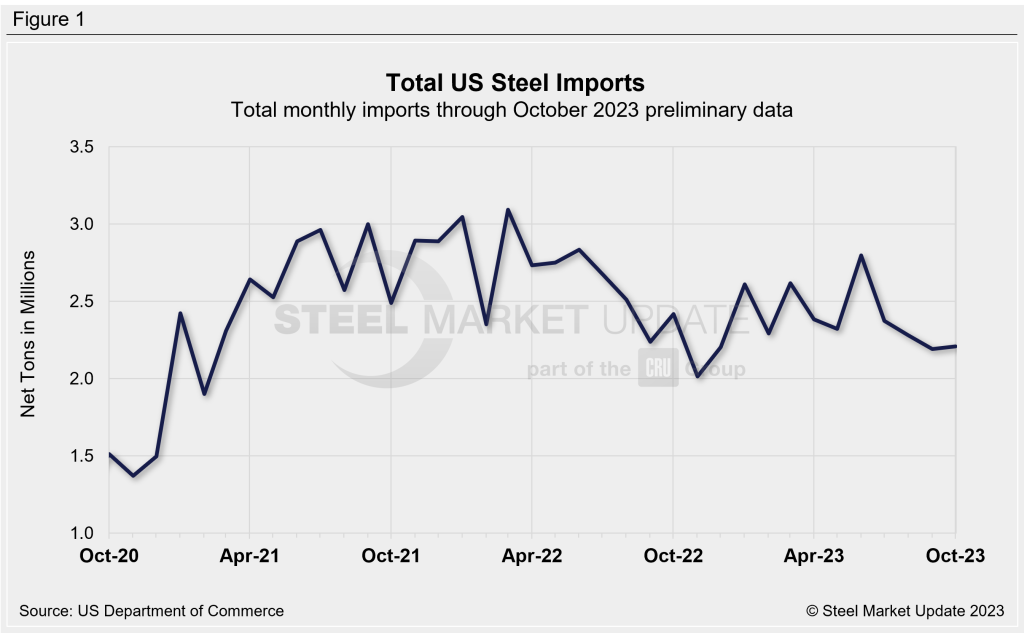

Despite the slight increase vs. the prior month, October was the second slowest month for steel imports year-to-date (Figure 1).

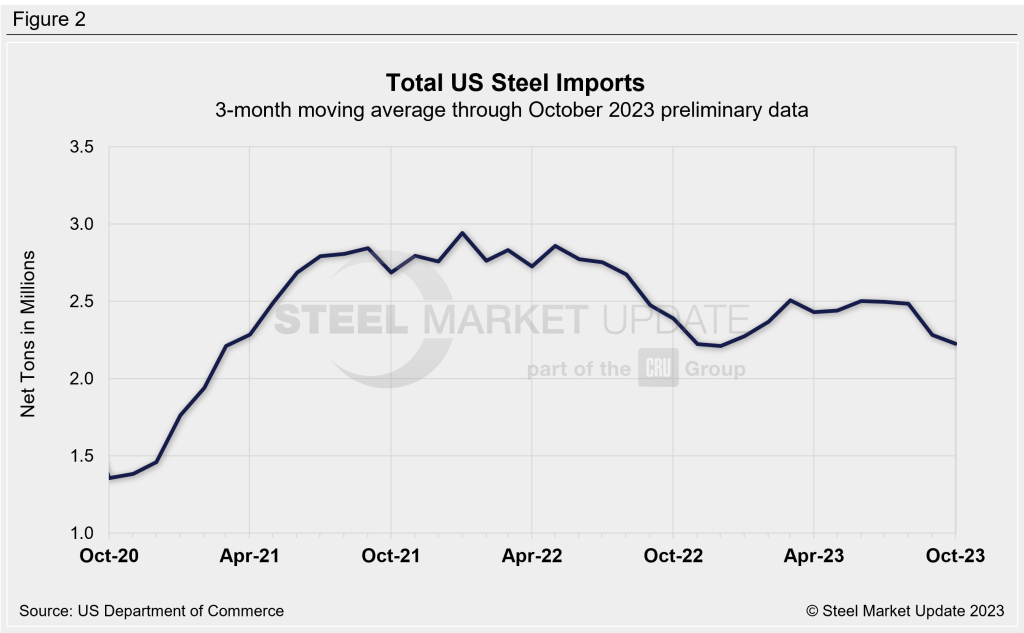

Imports as a 3MMA

Looking at imports on a three-month moving average basis to smooth out the month-to-month fluctuations, we can see that imports had been fairly steady for most of this year but have been trending down since August (Figure 2).

October’s 3MMA slid 2.4% from September to 2,226,862 tons.

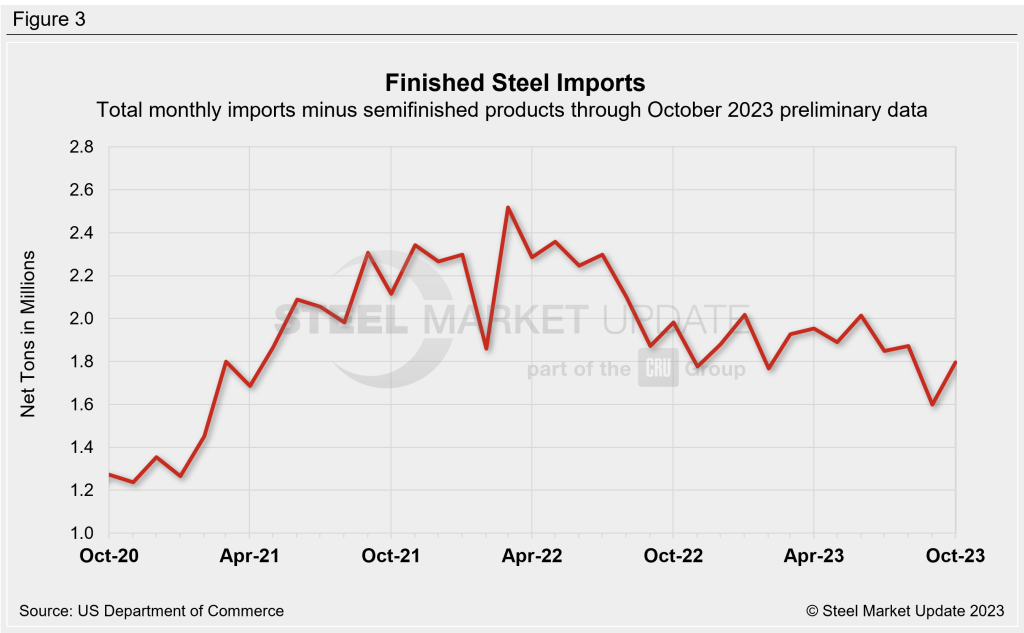

Semi-finished and finished steel

Recall that semi-finished steel imports hit a 23-month peak of 783,911 tons in June, and have since fluctuated. After bouncing back slightly in September, October’s semi-finished steel imports fell back again to 411,262 tons, down 31% vs. September.

Accounting for the bulk of the decline, slab imports from Brazil fell by 68% MoM to just 96,668 tons, according to the government data.

Finished steel imports, meanwhile, saw a 12.3% boost from September, totaling 1,796,550 ton in October. Despite the MoM increase, it was one of the slower months for finished steel imports in 2023 (Figure 3).

Long products and pipe and tube imports both improved in October after slowing notably the month prior (see Table 1 below), still accounting for some of the lower totals in finished steel imports.

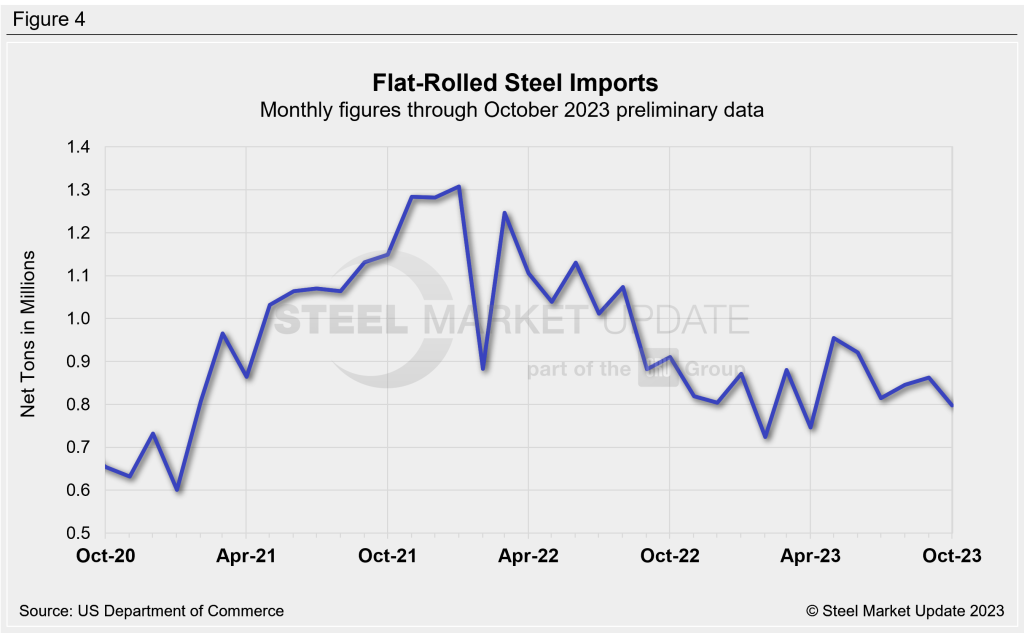

Flat-rolled steel

Flat-rolled steel imports had reached a three-month high in September but fell 7.5% in October to 797,785 tons (Figure 4).

Hot-rolled sheet imports slumped 38% MoM to 159,996 tons, likely coinciding with lower domestic prices that bottomed out at $645 per ton in late September. The lower total in October is largely in line with the norm, which typically sees imports from Japan, South Korea, and Brazil spike in the final months of the quarter, as importers seek to fill quotas in place for those countries.

Hot rolled imports from South Korea were at a recent high of 85,612 tons in September but fell to just 6,292 tons in October. A similar trend was seen for imports of the same product from Brazil and Japan, which were down 60% and 22%, respectively, from September to October.

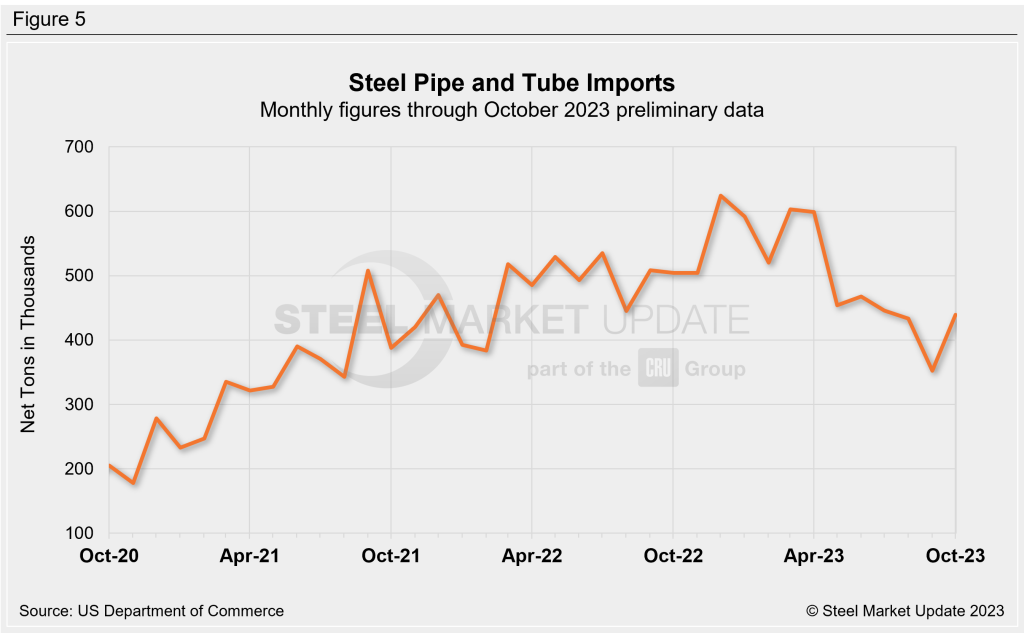

Pipe & tube

Pipe and tube imports saw a 25% MoM boost in October after hitting a 25-month low of 351,168 tons in September (Figure 5), mostly due to a slowdown in imports of OCTG. October’s pipe and tube imports count reached 439,902 tons.

In April, OCTG imports hit a recent high of 341,595 tons, but in October they were just 160,272 tons and not far from the 31-month low of 108,015 tons seen the month prior.

Imports by product

The chart below provides further detail into imports by product, highlighting high-volume steel products.

Note the significant decline in flat-rolled and pipe and tube imports, with cold rolled, tin plate, galvanized, and OCTG showing some noticeable MoM, but especially YoY declines. Line pipe and heavy structural imports decreased drastically vs. a year ago.