Market Segment

November 1, 2023

Plate Report: Nucor’s Plate Price Cut Stuns

Written by David Schollaert

Nucor’s plate price cut notice caught many off guard this week, especially after the company had maintained its pricing position in late September.

This week’s move also came at a time when hot-rolled coil (HRC) prices have been moving higher, spurred on by repeated mill hikes.

US plate prices have been relatively flat this year, especially when compared to sheet products, further underscoring domestic mills’ successful efforts to decouple discrete plate from HRC.

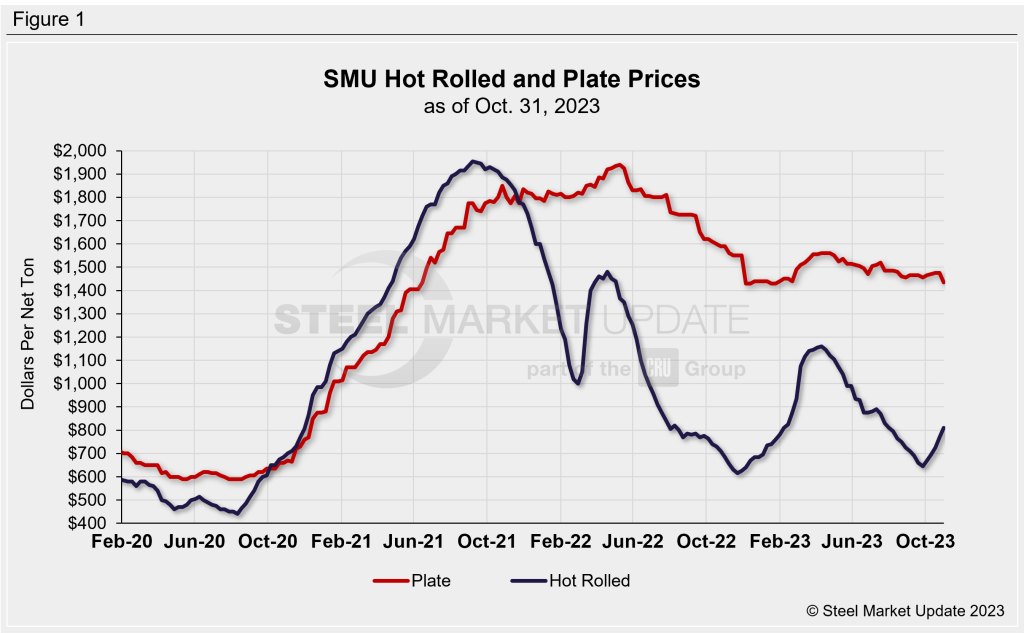

Case in point; SMU’s plate price stands at $1,435 per ton ($71.75 per cwt) on average, down $40 per ton from last week and down $85 per ton from a recent high of $1,520 per ton in mid-July (Figure 1). Our HRC price is at $810 per ton, up $40 per ton from last week and up $150 per ton since reaching a recent bottom of $660 per ton in mid-September.

Market Reaction

The news of lower plate tags was a surprise to most, but sentiment is still mixed on what it means for both the short term and long term.

While prices had been trending lower, mills seemed steadfast in keeping tags unchanged. Most sources expected Nucor to lower prices with the opening of its December order book. The sharp cut was overdue to some, but others believe the aggressive cut helps no one.

Nucor has been the unofficial top end of the range for domestic plate of late, market participants said.

Below is reaction from plate market participants in their own words:

“Yeah… it was a surprise as they didn’t need to cut $140 per ton. It was a bit too much but, whether they like it or not, other mills will have to follow suit to some extent.”

“I think Nucor has been intentionally sending out signals to the market that ‘Nucor is the market’.”

“Many including myself said they should have been incrementally reducing their number and not holding and holding and holding. Everyone can deal with incremental.”

“Too much all at once. Not sure what drove that decision. I expected about a $60 [per ton] max drop so not sure what this will do to the market for the balance of 2023.”

“I was not [surprised] and they were too late to start this process. Resale prices were already approaching or below the new $1390 per ton fob mill. Import is coming in cheap, domestic order books have shrunk, and now panic mode is setting in to fill the mills for year-end.”

What Comes Next?

The trend we’ve seen for much of the year is expected to continue: Limited spot activity and mills leaning heavily on contract business.

But some suggest the latest reduction by the Charlotte, N.C.-based steelmaker will place significant pressure on competitors and service centers alike.

“It a bloodbath,” said a source. “Service centers racing to get rid of anything not sold on the floor to make room for newer and cheaper steel.”

“My guess is it will just kill service center margins and everyone will adjust accordingly,” said another source. “Street prices in the upper $60’s will be the point of participation number.”

“All the tons we have coming in plus $1,400 per ton is obviously loser tons,” said a third source. “This drastic drop served nobody in a positive way.”

Despite the added pressure and potentially even lower plate prices in Q4, most agree that the new year will bring about renewed price hikes.

“I fully expect an increase in early Q1. Let’s see what support follows from all directions,” said a source. His sentiment was echoed by others.

“In December they will increase the prices back up for Q1, 2024 delivery orders, saying demand has been improved or something like that.”

HRC-Plate Spread

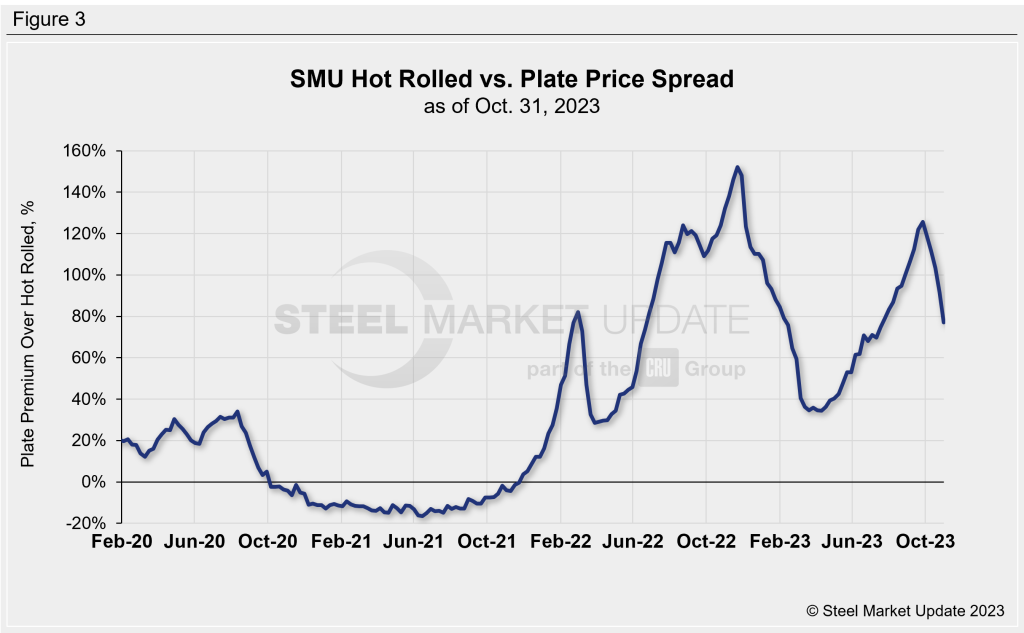

It’s been nearly two years now since plate prices decoupled from HRC (Figure 2). We saw the spread between plate and HRC reach as high as $970 per ton in the summer of 2022. It currently sits at $625 per ton.

As a percentage basis, plate’s premium over HRC had ballooned to 126% in late September (Figure 3), reaching a 10-month and not far from the all-time high of 152% in November 2022. But with HRC prices on the rise and plate tags declining, the premium is down to 77%.

The Takeaway

With plate demand spotty, sellers have been discounting and undercutting published mill prices. With most focused on controlling order books, the recent price cut will likely drive prices lower, cutting in on the big premium over HRC.

Also, imports remain attractive. Offshore product is running between $1,250-1,300 per ton at depots. And plate for early Q1 delivery from South Korea and Thailand is still sub-$1,200 per ton, according to several sources.

It’s important to keep an eye on discrete plate lead times. While they have inched a bit recently, Nucor’s December order book looks to keep them right at or below the five-week mark.