Prices

April 10, 2025

HR Futures: Traders' views mixed as market navigates tariffs

Written by Mark Novakovich

There’s been a lot ink spilled over the past several weeks regarding US tariffs. And the overall macro environment and news cycle have weighed on trade volumes and prices in the US ferrous derivatives markets.

While the backwardation structure that materialized beginning in February continues to roll forward, flat prices across the curve are lower. Market participants remain largely focused on nearby shipment periods. They are said to be purchasing tonnage on a hand-to-mouth basis, weighing on futures activity.

HRC

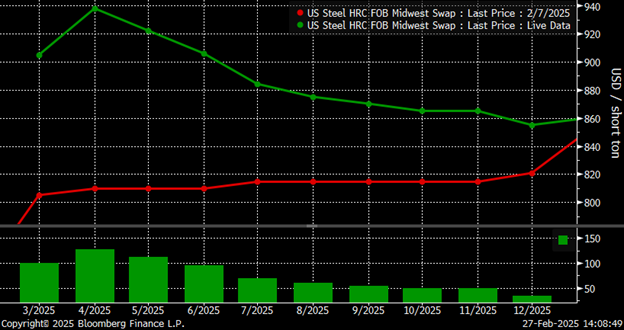

Prices on the front-end of the CME hot-rolled coil (HRC) futures curve, in the Q2 months, have fallen the most dramatically since the run-up that began in earnest in January.

May’25 HRC futures reached a contract high on March 4 at $945 per short ton (st). Since that time they have retreated by over $100/st, settling at $829/st as of today.

The drop in June’25 HRC futures is even more pronounced. They have fallen by $150/st from a contract high at the end of February ($930/st), to close at $791/st today.

Open interest (OI) across the HRC complex has also fallen. After reaching nearly 840,000 st in HRC towards the end of Q1, total open interest now sits at nearly 700,000 st. Nearly 78% of open interest rests between April’25 and July’25, with minimal interest in forward positions in the second half of 2025.

The lack of physical activity in forward positions, delayed by recent events/news, is thus reflected in lower volumes and declining open interest.

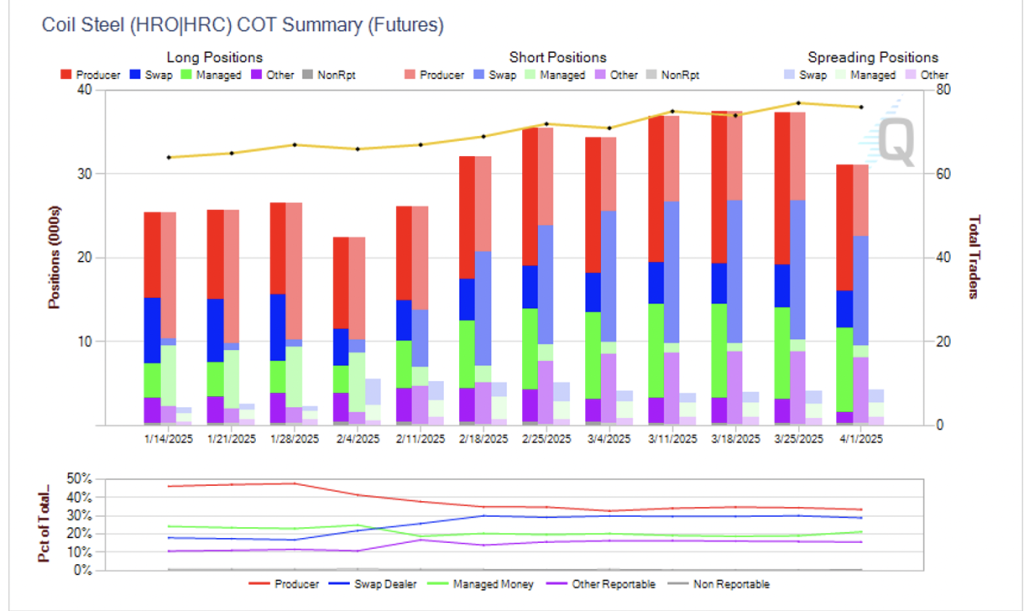

The CME’s Commitment of Traders chart below shows the decline in commercial market participation during the first quarter of the year.

After reaching nearly 50% of total positioning in January, the producer (commercial) category of OI has fallen to nearly 30% as of last week. And the swap dealer category (financial participants) has gained and made up a portion of the difference.

It is interesting to note, however, that the producer category had flipped from net short to net long in mid-February, as Section 232 tariffs looked imminent. They’ve retained their long bias since.

Traders’ views are decidedly mixed at the moment. Some see supportive catalysts in the market owning to expectations of reduced sheet imports, and as of now, still decent manufacturing demand. Other traders view the overall business climate as being too uncertain, and potentially leading to longer-term demand destruction.

Busheling contract

The CME’s Chicago busheling scrap contract has also seen prices decline in conjunction with HRC values.

The second month, May’25 futures have fallen by $75 per gross ton (gt) from contract highs on March 5 at $520/gt, to close at $445/gt today.

Overall trade in the scrap futures contract has been muted, as steel prices have fallen. However, open interest remains largely unchanged, just shy of 50,000 gt across all months.