Prices

April 3, 2025

Market pressures trigger HR futures reversal

Written by Joshua Toney

Market dynamics are shifting rapidly, with futures pricing diverging from physical fundamentals, creating a complex landscape for steel traders.

Import arbitrage opportunities are under increased scrutiny as forward curves signal potential shifts. Volatility in the CME US hot-rolled coil (HRC) spread market is intensifying, mirroring broader market uncertainties.

Current conditions highlight a widening disconnect between spot market realities and futures valuations. Until Wednesday’s index print, tariff levels offered little apparent support. A key observation: June 2025 futures were trading nearly at pre-tariff parity, raising a critical question: Is the physical HRC market set for a sharp decline, or are futures experiencing an oversold scenario?

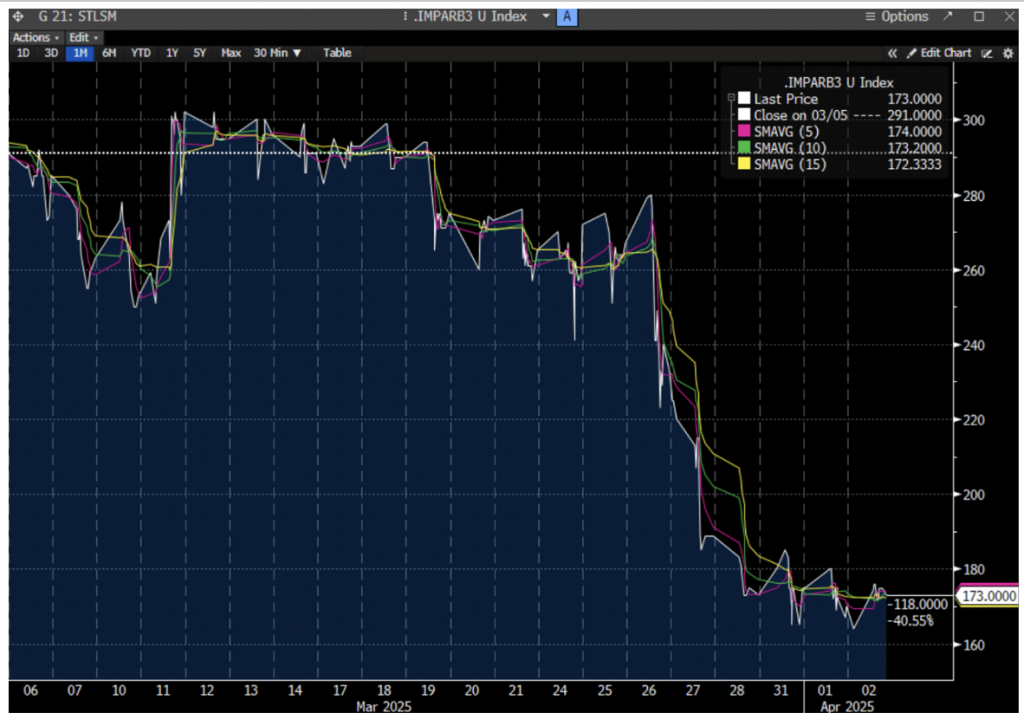

June 2025 HR candlestick with technicals (last six months)

Source: Bloomberg

Buying on blocks in Wednesday’s session finally provided some market support. However, policy clarifications from “Liberation Day” add another layer of uncertainty. Beyond import restrictions, it remains unclear what exactly the steel market is being “liberated” from.

March 2025 flat product license data shows only a modest 100,000-metric-ton (mt) decline (Source: Department of Commerce International Trade Administration), suggesting limited immediate impact.

Thin trading volumes across platforms reinforces the uncertain backdrop. Block trades in HRC and busheling (BCH) have slowed compared to last month’s surge. Import arbitrage spreads, while historically elevated, are narrowing. This suggests that if forward curve projections hold, imports may become less viable amid weakening demand.

The idling of Cleveland-Cliffs’ Dearborn, Mich., steelmaking operations further underscores this bearish outlook, particularly as additional tariffs on imported vehicles and components come into effect.

Raw materials and mill margins: signs of pressure

On the raw materials side, iron ore prices remain stable but uninspiring. Potential impacts from the Simandou Mine in Guinea, expected to start commercial production by the end of the year, remain a 2025 consideration.

Meanwhile, US mill margin spreads present emerging positioning opportunities, as scrap appears poised for pressure in the April trade cycle.

Turkish importers face heightened risk of EU-imposed scrap export protections, adding another layer of uncertainty. Turkish mills have remained largely inactive. This is partly due to the Eid holiday, but also in anticipation of tariff outcomes and geopolitical instability following the arrest of Prime Minister’s Erdogan’s opposition.

As Q2 begins, the market finds itself at a crossroads. Participants await clarity on tariffs while grappling with a weakened demand environment. The intersection of policy uncertainty and deteriorating fundamentals suggests continued volatility. Special attention should be paid to global spread relationships as a gauge for potential arbitrage plays.

June 2025 US HRC – EU HRC spread (short ton/mt differential not factored)

Source: Bloomberg

With futures and physical markets diverging, the critical question remains:

Which side will yield – and at what cost?

Disclaimer: This report was approved and issued by Marex Financial, a company within the Marex group. Marex Financial is incorporated under the laws of England and Wales (company no. 5613061 and VAT registration no. GB 872 8106 13), is authorized and regulated by the Financial Conduct Authority (FCA registration number 442767) and is a member of the London Stock Exchange. Marex Financial’s registered address is at 155 Bishopsgate, London, EC2M 3TQ. Nothing in this report constitutes (i) an offer of services, (ii) an offer to purchase or sell investments or any other product or (iii) investment, tax or legal advice. The report has been approved and issued on the basis of publicly available information, internally developed data and other sources believed to be reliable. It has been prepared for the general information of Marex’s institutional clients, is not directed at retail customers and does not take into account particular investment objectives, risk appetites, financial situations or needs. Recipients should make their own trading decisions based upon their own financial objectives and financial resources. This report is a marketing communication. It is not investment research and has not been prepared in accordance with legal requirements designed to promote investment research independence. The report is not subject to any prohibition on dealing ahead of the dissemination of investment research. Whilst reasonable care has been taken to ensure that facts stated are fair, clear and not misleading, Marex does not warrant or represent (expressly or impliedly) their accuracy or completeness. Any opinions expressed are those of the author of the report as at the date of the report and not necessarily those of Marex and, in any event, may be subject to change without notice. Marex accepts no liability whatsoever for any direct, indirect or consequential loss or damage arising out of the use of all or any of the data or information in this report. This report is not intended to be an offer to buy or sell any securities of any company referred to herein nor any other transaction or investment. This report is not intended for use by any other person than the addressee. If you are not the addressee, please delete it and immediately notify the Group Compliance department at Marex. This report may not be distributed in any jurisdiction where its distribution may be restricted by law. Additional material relating to any security, transaction or investment referred to in the report may be made available on request. No part of this report may be redistributed, copied or reproduced without the prior written consent of Marex. You must not distribute any part of this report to any other person without attaching a copy of this information.