Analysis

March 23, 2025

Final Thoughts

Written by David Schollaert

Have we hit a bit of a lull when it comes to the recent price bump? Mills certainly capitalized on the threat of tariffs and the unknown, with much that still could unfold.

Prices have been firm but stable over the past couple of weeks after rallying by roughly $265 per short ton (st) over seven weeks starting at the backend of January.

And while uncertainly is still king, is the response to “What might be?” shifting?

The first talk of tariffs in Trump 2.0 seemed to bring on some frenzied – dare I say panic – buying. A lot of buyers looked to max out contracts, exercise options, and there was a heck of a lot of pulling forward.

For many, it was reminiscent of your first experience with air turbulence. That is, you try your best to remember what the flight crew said during those safety instructions you largely ignored.

And then panic sets in. You even grab the seat for safety. The same seat bolted onto the plane flying somewhere between 30,000 to 40,000 feet above sea level you’re worried might fall out of the sky.

You’re a pro, you’ve been here and done that!

But now, after all the twists and turns, ups and downs, ons and offs, of the last two months, you’re a pro.

Heck, you know the difference between blanket tariffs, reciprocal tariffs, sectoral tariffs, Section 232, and even Section 301.

Now, when safety instructions begin, you’re like Kevin McCallister in Home Alone 2 on board a flight to New York City, completely unaware of where you’re going and what might unfold.

“In the event of a sudden loss of cabin pressure, secure your seatbelt, find your nearest oxygen mask…” Cue putting on the headphones, and closing your eyes.

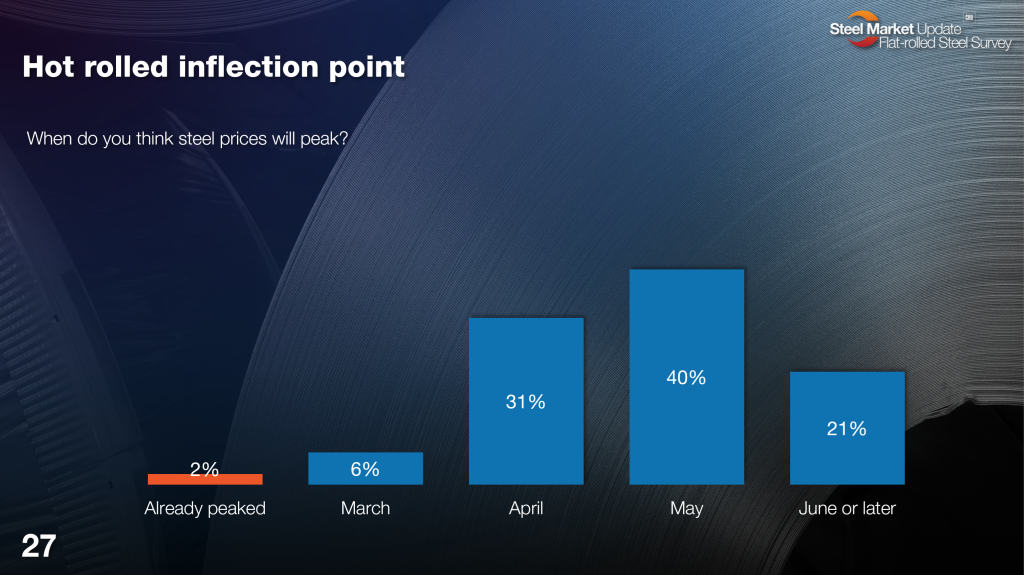

So, while price bumps are still expected as tariff uncertainty looms – more than 90% of survey respondents think prices have yet to peak (see Figure 1 below) – panic buying might not be as much of a driving force as it was at first.

Or will it…? Cue the armrest clutch!

Survey says…

We’ve already covered how Steel Buyers’ Sentiment remains strong despite some ebb and flow, and how lead times – which surged due to tariff-related buying – now seem to be steadying. Also, we’ve noted that despite a modest improvement in negotiation rates from early March lows, steel mills are still holding firm on pricing.

So now let’s give the slides and the survey participant comments a chance to do the talking.

Prices still have room to grow

More than 90% don’t think prices have peaked yet. Most expect that to happen in Q2, but there’s about 5% of you that think it will happen here in the next 10 days.

Here is what some survey respondents had to say:

“Ongoing uncertainty provides an opportunity for price increases.”

“Price rise for another month and a half.”

“Core trade cases and reciprocal tariffs will tighten the steel markets.”

“If tariffs stay, steel will continue to climb until you reach the offset in change plus tariffs.”

“Seems to be running out of steam. Customers are willing to wait until they see prices come down.”

“So many increases so fast have caused panic buying, and I think the mills are in a comfortable spot now to let things plateau.”

“Tariff will be close to resolved and demand is just okay.”

“The weak demand I’m seeing suggests that prices won’t go much higher.”

“I think we are at the top of the mountain. I think it’s stable for a bit from here.”

“I feel tariffs caused a surge of companies buying farther out to get ahead of price increases and to ensure they had product as lead times push out. I don’t feel demand has improved for end goods; mills will be getting hungry again soon for new orders.”

“Demand will not support much more increases.”

“Even though this feels purely “supply-driven,” that doesn’t mean it isn’t real.”

“We have not felt the full impact of the redefined steel tariffs, and the anti-dumping suits are right around the corner.“

“Trade wars create higher prices.”

“Demand fundamentals are still weak, or weaker than before.”

“Think we are close. A lot of steel on order but excitement has died off.”

“No major uptick in real demand.”

“With our forecast weakening, this is when I see the market self-correcting.”

“Tariffs pushing pricing up.”

“The spread between domestic and foreign is too big even after paying tariffs.”

Is the peak in sight?

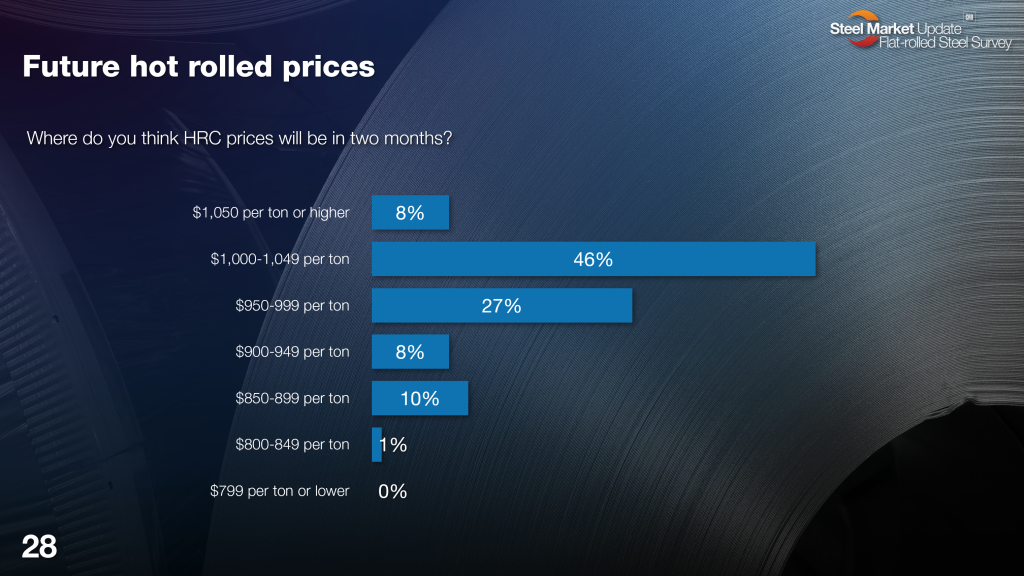

Next up: How high might HR prices rise over the next two months? While spot buying is not what it was, with uncertainty on how tariffs play out, wisdom of the crowd says we have at least another $100/st to go.

More than 50% of survey respondents think HR price will be over $1,000/st two months from now. Rewind to the beginning of the year; only 5% thought we’d be above $800/st come early March.

Here is what some survey respondents had to say:

“Up, up, up. Higher costs and decent demand.”

“Prices will continue to rise slightly.”

“They will peak in late April or early May and then drop off a bit through May. Larger drop in June.”

“This is the goal I feel the mills want.”

“Domestic mills have been waiting for the opportunity to push pricing up. The tariffs give them the chance to make it stick.”

“High-end of this range, close to $1,050. Domestic coated prices are much of a discount from imports.”

“Mills will push it until the market will not support.”

“Lack of demand.”

“We are anticipating a bit more of a run. We are also expecting a pretty epic collapse heading into the summer months, too…”

“Mills grabbing all they can…”

“I believe mills will attempt to exceed $1,000/ton for HR, but I don’t think it averages above that.”

“Unsettled trade wars.”

“I understand we’ve reached a price at which cheaper foreign steel will cause domestic mills to stop raising prices and maybe even lower prices.”

“Demand, Demand, Demand, and Demand.”

Up, up, and away

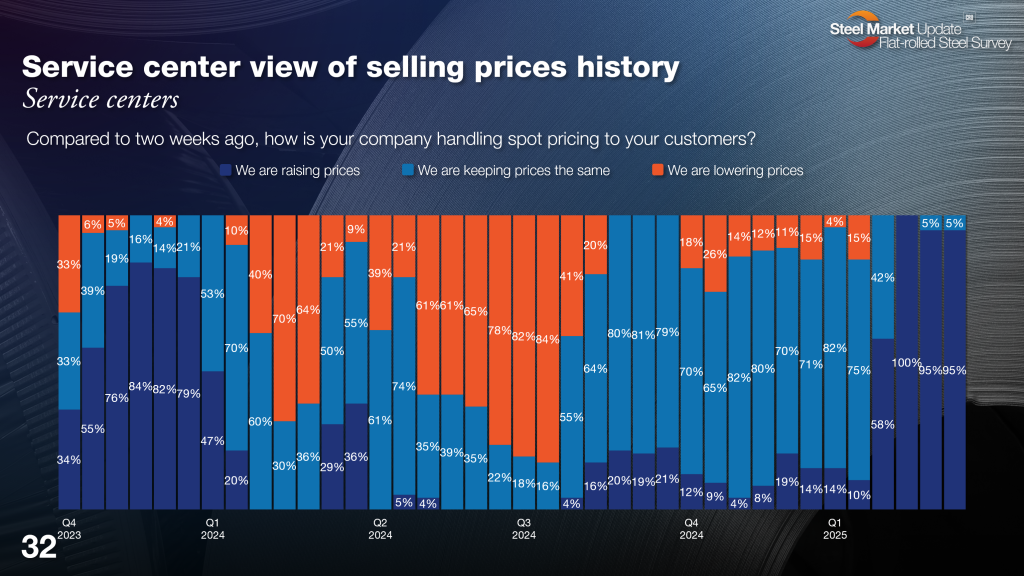

What does seem certain is prices still have some upward momentum in them. For three straight surveys—something we haven’t seen since March 2021—nearly 100% of service centers report they are still raising prices.

Much more to unpack

Well, there you have it. Just a quick peek at some of our latest flat-rolled steel survey data. Be sure to check it out.

Also, stay tuned for more SMU scrap coverage – especially ahead of next month’s settlement – or if you’re willing, we’d love for you to participate in our upcoming April ferrous scrap survey! Reach out to me at david@steelmarketupdate.com to learn more.

And, as always, all of us here at Steel Market Update truly appreciate your support.