AMU

March 14, 2025

Wittbecker on Aluminum: Where are Midwest premiums headed?

Written by Greg Wittbecker

As we go to press, the Chicago Mercantile Exchange (CME) derivative contract on Midwest premiums shows March at $0.411 cents per pound with April/May around $0.397 cents and the second half of 2025 at $0.3750.

All these numbers reflect a discount to what premiums should be trading at under different duty scenarios.

Why is that?

The most plausible explanation is that the leading price reporting agencies are unable to validate physical trade at higher numbers, which would allow them to print higher premiums.

From a seller’s perspective, it’s tempting to take profits after the run we have seen in Midwest premiums in less than two months. Prior to Inauguration Day, Midwest was trading at $0.2385 cents per pound. At current nominal premiums, premium longs stand to make about $0.17 cents per pound. Depending on the size of their long positions, the profit might make their 2025 year. So, it could be expected that some are selling onto the market and fading the published numbers.

Handicapping the different tariff scenarios

To help make sense of this chaos, we want to provide a primer on how to think about premiums under different tariff scenarios.

You can copy and paste this in your own spreadsheets and keep track of where the market is, relative to potential different replacement costs. Let’s start with some basic assumptions to keep in mind:

- You must plug in a value for the London Metal Exchange (LME) cash price which comprises the biggest component of building out the tariff calculation.

- You must incorporate something for the intrinsic value of physical metal CIF (Cost Insurance and Freight) delivered a US port of entry, be it Detroit, Baltimore, etc. Our discussions over the past two weeks have found this is an often-overlooked component of the calculation. For purposes of our models, we are going to use the value of Rotterdam duty unpaid metal as a proxy for the US duty unpaid premium. Why? The main reason is there is not much trade in US duty unpaid, while Rotterdam is an actively trade market. It is also the alternative market that most overseas primary producers are looking at as an alternative to shipping to the US.

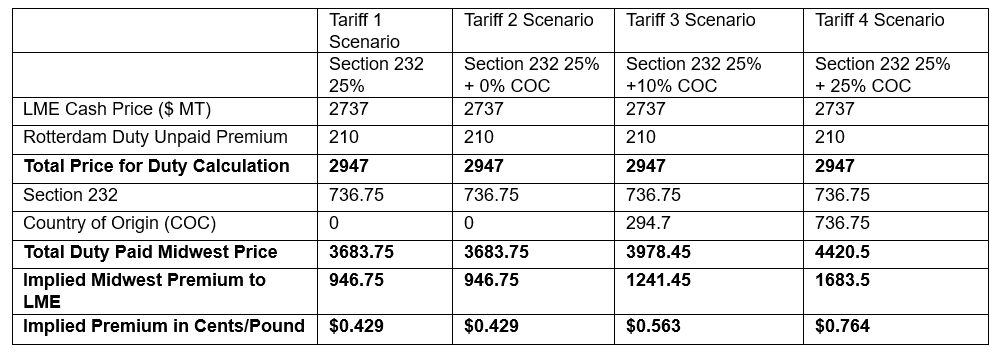

Now the fun begins, laying out the different combinations of duties that may eventually influence the direction of Midwest premiums:

- Section 232 at 25% applied to all origins without exclusions. This is where we are today.

- Section 232 at 25% with Canadian aluminum enjoying full exemption from Canadian country-of- origin 25% that may take effect in April. There is no precedent for this so far. This would be the same as Number 1, but it is important to flag the variable of the country-of- origin.

- Section 232 at 25% with Canadian aluminum at 10% duty on country-of- origin basis treatment as a critical mineral. This is the treatment that Canadian crude oil and potash now enjoy.

- Section 232 at 25% and Canadian aluminum taxed at the full 25% for country-of- origin. This is Canada’s worst-case scenario and one that we believe will NOT get priced in the Midwest premium structure. Why? Despite Canada being the largest single supplier to the US, other origins will have the lower Section 232 duty and enjoy massive competitive advantage vis-à-vis Canada. Eventually other origins will displace Canadian supply to the US. Canada will rotate its exports to the EU or Asia.

So, here is the math as of March 13:

So, comparing our Tariff 1 to the prevailing market, it is remarkably close. The market is doing its job in correlating replacement to current valuation.

Whether the other scenarios happen remains to be seen. We have seen forecasts from other analysts suggesting Midwest could reach $0.65 per pound. We do not know what assumptions they are making about the mix of tariffs to be applied, but based on current LME and duty unpaid premiums, we reverse engineered it to an implied duty structure of 41.5%.

Is there a best-case scenario for Canada not on the board?

Hope springs eternal and there are always people thinking Canada and the US will kiss and make up. But we have talked to many Canadians who think the relationship with the US is terribly damaged. The constant jabs about making Canada the 51st state have united Canadians across the political spectrum. Canada is in no mood to surrender its sovereignty and it is not going to roll over in the face of Trump’s bullying.

The big unknown is what is the realistic ask of the Trump Administration? If Canada could meet the demands, could Canada achieve an exemption from Section 232 again? Maybe. But I think the country-of-origin precedent set on crude oil and potash may still be there.

If, and that’s a big IF, Canada got Section 232 exemption and was left only with country-of-origin exposure – we would argue that Midwest premiums would continue to price clear at the Section 232 tariff of 25%. This would continue the pattern under the old Section 232 regime, where Canada enjoyed exemption from the 10% duty, but the market traded basis on the exposure of the most disadvantaged importers.

Stay tuned for next week’s update. We would be shocked if it did NOT change.

Editor’s note

This is an opinion column. The views in this article do not necessarily reflect those of SMU. We welcome you to share your thoughts as well at info@steelmarketupdate.com.