Sheet

March 6, 2025

US HR prices jump higher above imported tags

Written by David Schollaert

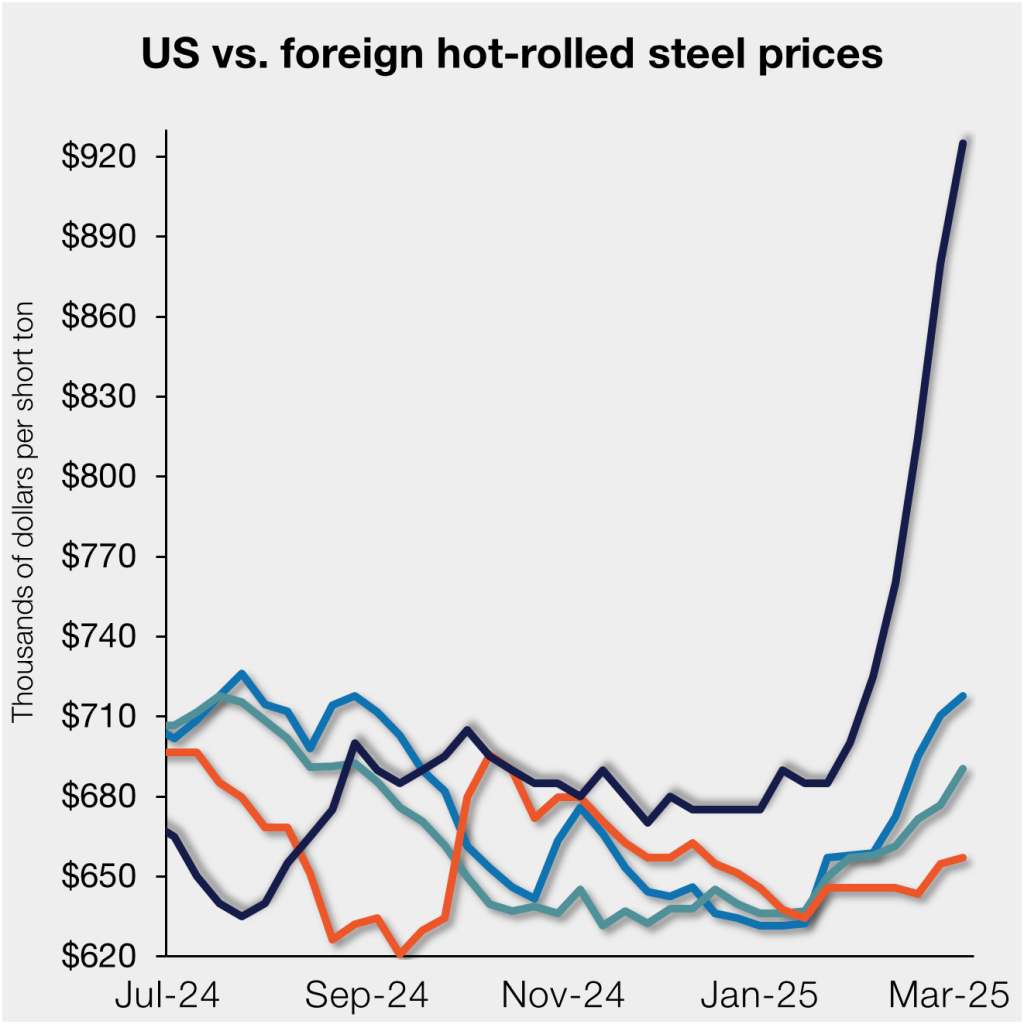

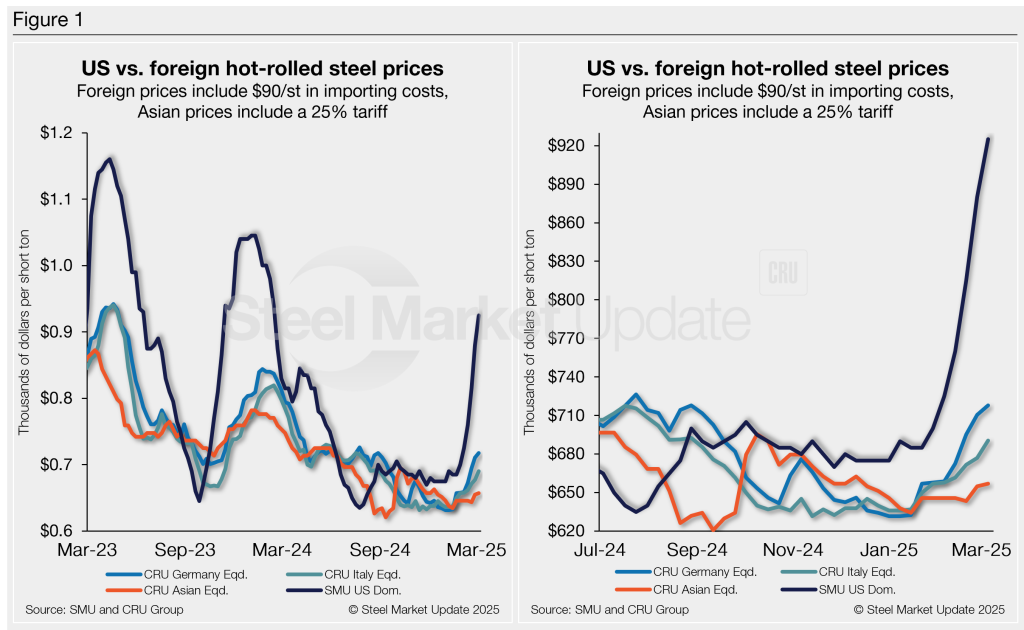

Domestic hot-rolled (HR) coil prices moved higher this week, widely outpacing increases seen in offshore markets. The result: US hot band prices are vastly more expensive than imports on a landed basis. The premium stateside tags have over prices abroad now stands at a 15-month high.

SMU’s average domestic HR price this week was $925 per short ton (st), up $45/st vs. the week before and up nearly $250/st since late January. Mills remain emboldened to move prices higher, supported by threats of tariffs on imports of steel. US hot band prices are at their highest point since February 2024.

Domestic HR is now theoretically 25.5% more expensive than imported material, up from 22.6% last week. That’s the widest margin since December 2023. Recall that US prices were ~12% cheaper than imports just seven months ago.

In dollar-per-ton terms, US HR is now, on average, $236/st more expensive than offshore product (see Figure 1). That’s roughly $37/st higher than the prior week and nearly $310/st above late July when US tags were ~$72/st cheaper than offshore material.

The charts below compare HR prices in the US, Germany, Italy, and Asia. The left side highlights prices over the last two years and the right side zooms in to show more recent trends.

Methodology

This is how SMU calculates the theoretical spread between domestic HR coil prices (FOB domestic mills) and foreign HR coil prices (delivered to US ports): We compare SMU’s weekly US HR assessment to the CRU HR weekly indices for Germany, Italy, and East and Southeast Asian ports. This is only a theoretical calculation. Import costs can vary greatly, influencing the true market spread.

We add $90/st to all foreign prices as a rough means of accounting for freight costs, handling, and trader margin. This gives us an approximate CIF US ports price to compare to the SMU domestic HR coil price. Buyers should use our $90/st figure as a benchmark and adjust up or down based on their own shipping and handling costs.

If you import steel and want to share your thoughts on these costs, please get in touch with the author at david@steelmarketupdate.com.

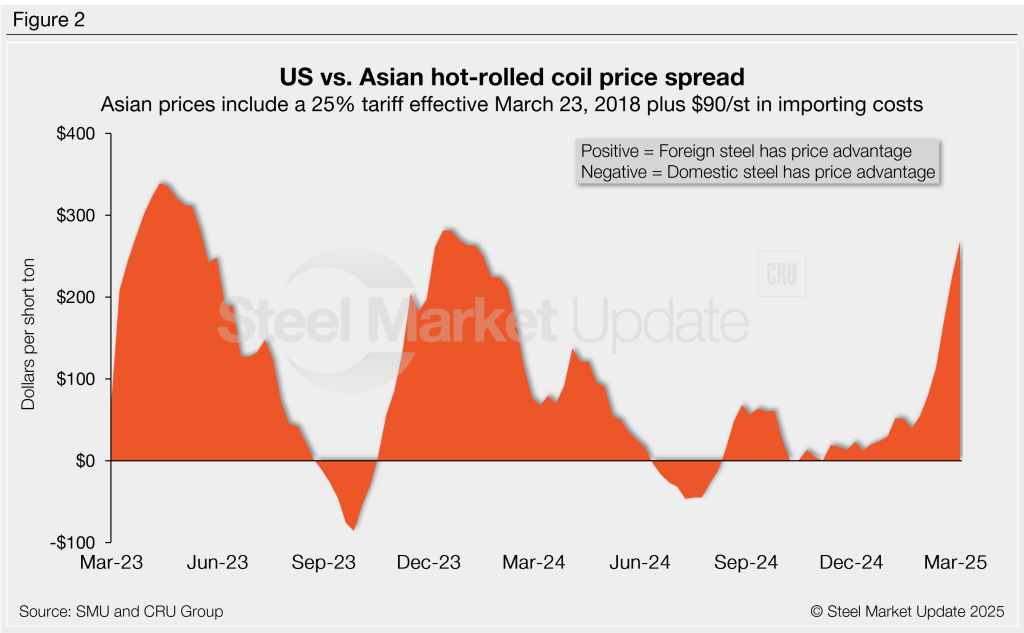

Asian HRC (East and Southeast Asian ports)

As of Thursday, March 6, the CRU Asian HRC price was $454/st, up just $2/st vs. the week prior. Adding a 25% tariff and $90/st in estimated import costs, the delivered price of Asian HRC to the US is ~$657/st. As noted above, the latest SMU US HR price is $925/st on average.

The result: Prices for US-produced HR are theoretically $268/st higher than steel imported from Asia – roughly $43/st higher week over week (w/w). The premium is now in line with recent highs seen in 2023 when stateside tags were ~$300 /st more expensive than Asian products.

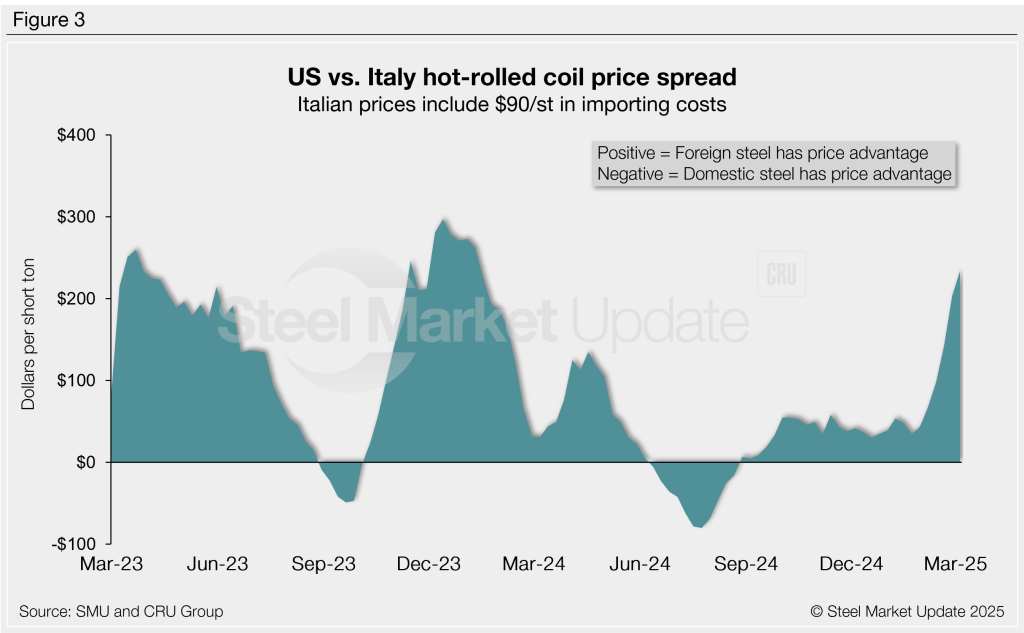

Italian HRC

Italian HR prices were $14/st higher this week at $601/st, according to CRU. After adding import costs, the delivered price of Italian HR is, in theory, $691/st.

That means domestic HR coil is theoretically $234/st more expensive than imports from Italy. With Italian tags up just $33/st over the past month, stateside prices have surged further ahead. The spread is $31/st higher w/w and at its widest margin since January 2024.

German HRC

CRU’s German HR price was up $7/st to $628/st this week. After adding import costs, the delivered price of German HR coil is, in theory, $718/st.

The result: Domestic HR is theoretically $207/st more expensive than HR imported from Germany, up $38/st from last week. Stateside hot band was at an $18/st discount about five months ago. At points in 2023, in contrast, US HR was as much as $265/st more expensive than imported German hot band.

Notes: Freight is important when deciding whether to import foreign steel or buy from a domestic mill. Domestic prices are referenced as FOB the producing mill. Foreign prices are CIF, the port (Houston, NOLA, Savannah, Los Angeles, Camden, etc.). Inland freight, from either a domestic mill or from the port, can dramatically impact the competitiveness of both domestic and foreign steel. It’s also important to factor in lead times. In most markets, domestic steel will deliver more quickly than foreign steel. Effective Jan. 1, 2022, Section 232 tariffs no longer apply to most imports from the European Union. It has been replaced by a tariff rate quota (TRQ). Therefore, the German and Italian price comparisons in this analysis no longer include a 25% tariff. SMU still includes the 25% Section 232 tariff on prices from other countries. We do not include any antidumping (AD) or countervailing duties (CVD) in this analysis.