Market Data

March 6, 2025

SMU Survey: Mill lead times extend, buyers question sustainability

Written by Brett Linton

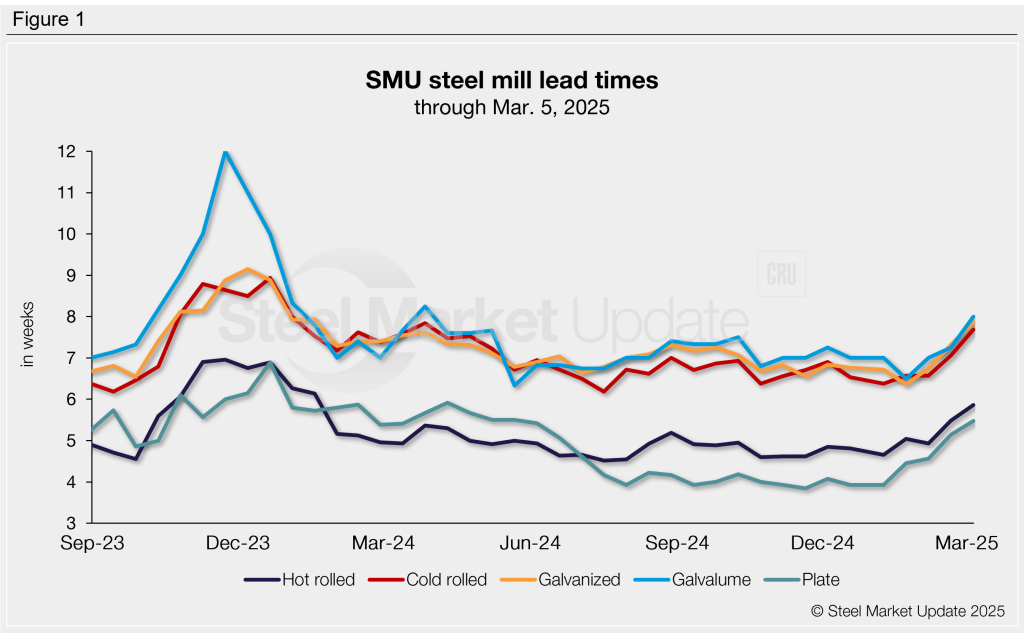

Buyers responding to our latest market survey reported longer lead times this week on all of the sheet and plate products SMU tracks.

Steel mill production times increased by two to five days this week versus mid-February figures. Lead times are currently about a week and a half longer than the lowest levels observed over the past year.

The average lead time for hot-rolled steel is currently just under six weeks. Tandem product production times are between seven and a half and eight weeks. Plate lead times now average five and a half weeks.

Table 1 summarizes current lead times and recent trends.

Compared to our Feb. 19 market check, cold-rolled and coated lead times ranges shifted this week:

- Cold rolled and galvanized: The longest lead time in each range increased from nine weeks to ten weeks.

- Galvalume: Our range widened from seven to eight weeks to six to ten weeks.

Buyers predict gains won’t have legs

The majority of the respondents we surveyed this week (59%) foresee stable lead times two months from now, a moderate increase from the 45% rate seen two weeks prior. Just over a third (36%) expect production times to get longer, a reversal from our prior survey when the majority (54%) predicted extensions. A smaller number predicted lead times would decline (5%), up from 1% in mid-February.

Here are some of the comments we collected:

“Lead times really haven’t extended through this up cycle. Certain mills are in and out of the spot market. But when they return to quoting, lead times are essentially the same by product.”

“Demand is not there.”

“We have not felt an uptick in demand yet.”

“If demand stays stagnant over the next two months, lead times should stay relatively flat.”

“Price increases are artificially created. This is not a demand driven pricing market.”

“Automotive and agriculture are over-inventoried, they will stay slow.”

“Mills will stretch lead times out a little to help justify the increased pricing.”

“Demand is increasing, but not sure how tariffs will affect demand further out in Q2.”

“Utilization rates will increase, causing a temporary demand spike to beat upcoming price increases.”

“Lead times are expected to extend in the short term. The combination of ongoing supply chain disruptions, high demand, geopolitical tensions, and logistical bottlenecks will keep delivery times longer than usual.”

“I think most of the mill lead time growth will already have happened in two months. But if I had to guess one way or another, I’d say that they might still be extending.”

“As pricing has peaked, buyers will push back – and that will reduce lead times.”

Trends

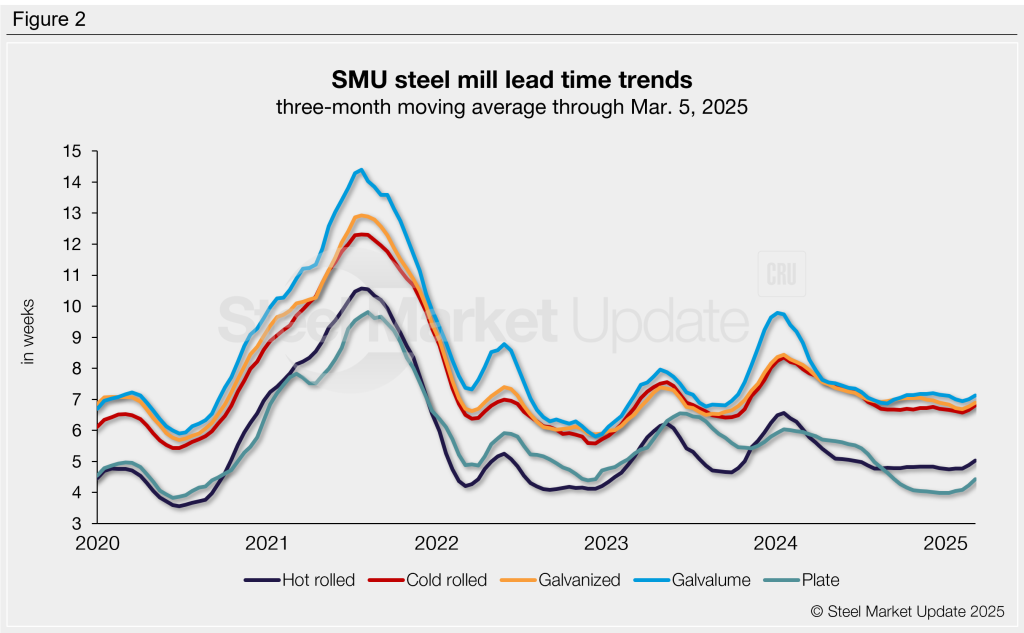

Lead times can be calculated on a three-month moving average (3MMA) basis to smooth out some of the variability seen in our biweekly data and better highlight trends. Through this week, the 3MMA lead times increased for all sheet and plate products we monitor, marking the second consecutive survey-to-survey increase. This follows a year-long decline, during which we saw multi-year low lead times (Figure 2).

Over the past three months, the average lead times by product are as follows: hot rolled at 5.03 weeks, cold rolled at 6.80 weeks, galvanized at 6.89 weeks, Galvalume at 7.13 weeks, and plate at 4.42 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Consult your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.