Prices

March 6, 2025

HR Futures: Major trade developments lift the ferrous complex

Written by Joshua Toney

Headline risk has returned to the ferrous complex, with both hot-rolled coil (HRC) and busheling ferrous scrap (BCH) markets surging in response to fresh trade restrictions.

After the imposition of 25% tariffs on imported steel and aluminum, curves have caught a steady bid, driving prices higher. US mills have added further momentum with aggressive price hikes, reinforcing bullish sentiment.

Latest datapoints: Nucor consumer spot price (CSP) now at $900 per short ton (st) as of Monday. Meanwhile, Apr’25 futures have breached $970/st as of the close on Tuesday.

The curve, however, dips sharply into Q3’25 by approximately $100/st. This raised the question: Are these price levels a reflection of a structurally weakened import market, or simply a symptom of short-term peak demand?

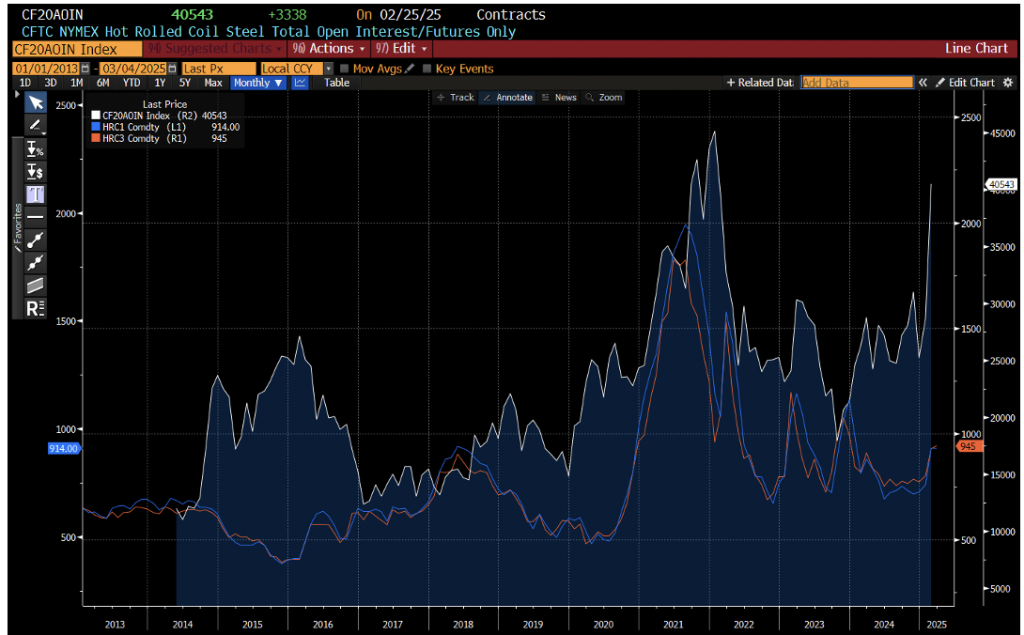

At this juncture, it’s worth revisiting net positioning on CME HRC. According to the Commitment of Traders report from Feb. 25, there are 40,543 lots (810,860 st) of open positions on HRC flat price – an increase of 66,760 st week over week.

Historically, the last time the market carried this level of exposure was in Q4’21-January 2022, when HR futures were trading near $1,900/st before a swift collapse to $1,052/st by the end of February 2022.

CFTC total lots open positions on CME HRC with M1 and M3 rolling prices

Source: Bloomberg, CFTC

The key takeaway isn’t that HRC prices are destined to double, but rather that volatility and liquidity have returned. This offers traders more incentive to carry positions and engage in new exposure.

Take import arbitrages, for example: (basis close of business March 4. On paper, the Apr’25 US HRC over Euro HRC spread implies a $323 per metric ton (mt) differential.

Breaking this down:

- Apr’25 Euro HRC futures price ex-works Northern Europe: €647/mt

- Estimated freight: €50/mt, yielding €697/mt landed

- Converted to short tons: €632.31/st

- Converted to USD using a 1.063 forward rate

- Adding a 25% tariff: $743.55/st landed in the US

- Comparing with Apr’25 US HR futures at $970/st, this leaves a $226.45/st spread. That’s plenty of margin to account for additional port, stevedoring, and transport costs. At minimum, this warrants closer investigation.

On the flip side, US HRC vs. LME FOB China presents a different picture (basis close of business March 4).

- Apr’25 LME FOB China settled at $472/mt

- Factoring in container freight of $174/mt (basis WCI Shanghai to Los Angeles), landed costs on the West Coast amount to $645.85/mt

- A 35% tariff on Chinese-origin steel brings the final price to $871.89/mt ($790.98/st).

- Compared to West Coast CSP pricing at $960/st, the $169.01/st spread appears less enticing than the EU differential but remains relevant given the US HRC curve structure.

While these arbitrage scenarios seem attractive on paper, the feasibility of executing such trades remains low given the inherent risk in physical transactions of this nature. However, they provide insight into why the CME HR curve is structured as it is.

Beyond pricing, geopolitical risk continues to add layers of complexity. Speculation around $1 million levies on Chinese-flagged ships docking at US ports could further disrupt import flows, while tariffs extending to raw material inputs especially in North America could upend even scrap trade dynamics.

With these evolving factors, the market is at an inflection point. Futures remain reactive to new developments, and the next significant move could be dictated by policy shifts rather than traditional supply-demand fundamentals. As the interplay between tariffs, trade routes, and domestic production costs intensifies, staying ahead of these developments will be critical for navigating the evolving landscape.

Marex CDD Report Disclaimer:

This report was approved and issued by Marex Financial, a company within the Marex group. Marex Financial is incorporated under the laws of England and Wales (company no. 5613061 and VAT registration no. GB 872 8106 13), is authorised and regulated by the Financial Conduct Authority (FCA registration number 442767) and is a member of the London Stock Exchange. Marex Financial’s registered address is at 155 Bishopsgate, London, EC2M 3TQ. Nothing in this report constitutes (i) an offer of services, (ii) an offer to purchase or sell investments or any other product or (iii) investment, tax or legal advice. The report has been approved and issued on the basis of publicly available information, internally developed data and other sources believed to be reliable. It has been prepared for the general information of Marex’s institutional clients, is not directed at retail customers and does not take into account particular investment objectives, risk appetites, financial situations or needs. Recipients should make their own trading decisions based upon their own financial objectives and financial resources. This report is a marketing communication. It is not investment research and has not been prepared in accordance with legal requirements designed to promote investment research independence. The report is not subject to any prohibition on dealing ahead of the dissemination of investment research. Whilst reasonable care has been taken to ensure that facts stated are fair, clear and not misleading, Marex does not warrant or represent (expressly or impliedly) their accuracy or completeness. Any opinions expressed are those of the author of the report as at the date of the report and not necessarily those of Marex and, in any event, may be subject to change without notice. Marex accepts no liability whatsoever for any direct, indirect or consequential loss or damage arising out of the use of all or any of the data or information in this report. This report is not intended to be an offer to buy or sell any securities of any company referred to herein nor any other transaction or investment. This report is not intended for use by any other person than the addressee. If you are not the addressee, please delete it and immediately notify the Group Compliance department at Marex. This report may not be distributed in any jurisdiction where its distribution may be restricted by law. Additional material relating to any security, transaction or investment referred to in the report may be made available on request. No part of this report may be redistributed, copied or reproduced without the prior written consent of Marex. You must not distribute any part of this report to any other person without attaching a copy of this information.