Canada

February 23, 2025

Price: Should billions in Section 232 revenue go to foreign manufacturers or to the American people?

Written by Alan Price & Ted Brackemyre

On February 10, 2025, President Trump signed executive orders imposing enhanced import duties on steel and aluminum products under Section 232 of the Trade Expansion Act of 1962.

Building on the Section 232 duties originally imposed by the president during his first term, these orders eliminate country-wide exemptions and product-specific exclusions. They also expand the scope to cover certain downstream derivative products. Section 232 in addition raises the duties on aluminum imports from 10% to 25%.

Principally, these executive actions will restore the Section 232 program. They do that by eliminating the byzantine web of exemptions, quotas, and exclusions that led to a sharp decline in the program’s effectiveness. The strengthened and expanded duties take effect March 12, 2025.

No cookies for foreign producers

Almost immediately following President Trump’s announcement, lobbying campaigns were launched by several of the world’s largest steel and aluminum producers. In conjunction with the foreign governments working at their behest, they want to once again secure exceptions to the Section 232 duties. It is imperative that we keep their hands out of the cookie jar.

While the president has been adamant that the restored duties will not be subject to exemptions or exclusions, foreign manufacturers have sought to soften that ground with arguments about supply chains and product availability. They are hiding their true agenda and the real question facing policymakers. Do we want the benefits of the Section 232 tariffs to flow to the bottom lines of foreign steel and aluminum producers or to the US government and, ultimately, domestic manufacturers and their workers?

In our view, the answer is simple. Section 232 exceptions do nothing more than lead to underserved profits for foreign manufacturers who are harming the US industrial base. And they do so at the direct expense of the federal treasury. That revenue could be used to pursue the Trump administration’s other policy priorities – such as deficit reduction or expanded tax cuts.

The aluminum story

Take the aluminum industry as an example. Primary aluminum prices in the United States are largely determined by adding the London Metal Exchange price and the Midwest premium. (The latter accounts for the premium to supply aluminum to the US Midwest.)

Functionally, the Midwest premium tracks the level of the Section 232 aluminum tariffs. It also roughly represents the available profits or tariff rents in the market. This means there is a trade-off between the revenue that could be collected by the US government and the additional profits won by foreign manufacturers who take advantage of exemptions and exclusions. While the pricing mechanisms are not the same, the steel industry follows a similar pattern.

You do not have to take our word for it either. Rio Tinto CEO Jakob Stausholm explained in an earnings call last week that “{i}f all countries are getting a tariff, the impact for us is zero.” He also said that the previously granted exemption for Canada “gave a favorable position to our Canadian {aluminum} smelters.” Rio Tinto in addition noted that with US tariffs in place, it could simply redirect shipments to different markets, and other producers would supply the United States. In short, there is no supply chain problem.

Imports up, US smelters down

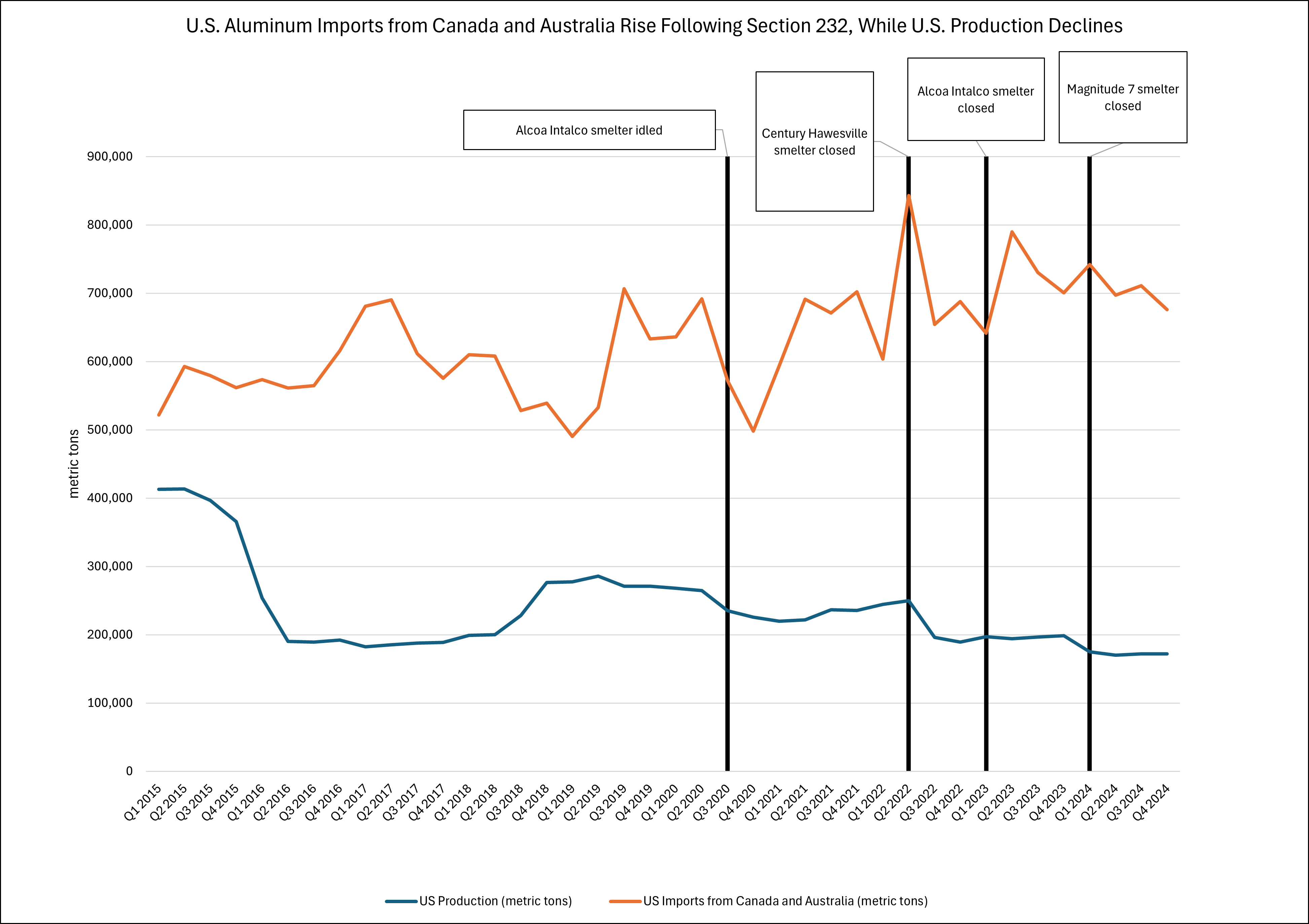

The example of Alcoa illustrates what happens when broad exceptions are provided. Since 2019, Alcoa has shut down 40% of its primary aluminum production in the United States, in favor of its Canadian and Australian production. That is production the company could have been kept in or moved back to the United States. But it did not do that.

As shown below, exemptions for Canada, Australia, and others encouraged the exact opposite. Canadian and Australian imports are represented by the orange line. The blue line is US production. The text boxes detail US smelter idlings or closure. (Source: CRU and US import statistics for HTS 7601.)

To be clear, since 2010 Alcoa has systematically closed or partially curtailed production at eight aluminum smelters in the United States. And this has been fueled in part by massive Canadian aluminum subsidies, which the OECD recognizes are among the highest in the world.

The exit of Alcoa and others from the US market should not be encouraged by exempting their Canadian and Australian production from Section 232 duties. This perversely allows foreign production to capture tariff rents at the expense of the US government while also undermining US production.

Steel – uh oh, Canada

The steel sector is no different. Canada and Australia have heavily subsidized their steel industries. It should come as no surprise that these countries and others want to keep a broken Section 232 system in place as an outlet for their subsidized production.

For instance, in the late 2000s, U.S. Steel wanted to shut down Stelco because the Canadian sheet producer was no longer economically viable. However, Canadian authorities aggressively sued U.S. Steel to keep Stelco alive.

Subsequently, Canada bailed out Stelco. Ottawa forgave CAD $4.4 billion in Stelco debt and pension liabilities. It cancelled 50% of Stelco’s tax liabilities. And it provided additional low-interest loans, without which Stelco would have likely shut down or significantly curtailed capacity. While the Canadian government was resuscitating Stelco, U.S. Steel eventually shifted toward idling its Granite City mill in Illinois. Was that timing a coincidence?

Canadian and Ontario governments have also provided CAD $900 million in funding to EU-based ArcelorMittal to convert one of its outdated blast furnace mills into a new, 2.5 million metric ton (mt) DRI-EAF mill. Likewise, Algoma Steel, Canada’s sole producer of cut-to-length plate, recently received as much as CAD $420 million in government assistance to build a new EAF mill. It will increase Algoma’s production capacity by approximately one million mt per year. As these investments show, when the Canadians and others argue for Section 232 exceptions, they are really fighting for a payout for their own subsidized industries and to exploit the US market.

Enough is enough

If the seven-year history of the Section 232 program has taught us anything, it is that massive exemptions and exclusions have discouraged the reshoring of steel and aluminum production. Admittedly, that is a process that takes time. However, nearly seven years have passed, and foreign steel and aluminum producers are resorting to the same types of supply chain arguments without actually moving production back to the United States.

With a myriad of exemptions and exclusions in place, the Section 232 tariffs have discouraged reshoring US production or closing the US trade deficit. It is not credible to think that foreign manufacturers and importers will start reshoring production now if Section 232 exceptions are reinstated.

The Section 232 program works best if it is broadly applied. That means no quotas, no country-wide exemptions, no product-specific exclusions, and no other exceptions. The national security concerns and worldwide overcapacity crises that precipitated the steel and aluminum Section 232 investigations are global concerns. And they can only be properly addressed with a global remedy – not one that has been hollowed out with exception after exception. Steel producers around the world need to right-size their production capacity. Until that happens, they should not be permitted to offload their non-economic capacity in the US market.

With extensive exceptions in place, steel capacity and production simply get shuffled around global markets. As a result, large volumes of imports still flow to the United States without paying any Section 232 duties. For example, for many steel products, there is broad availability of product exclusions and country-wide exemptions for some of the United States’ largest trading partners. That has led to Section 232 duties being applied to less than 20% of imports. If little or no tariffs are collected, then no protection is provided to the US industry. It also means that no incentive is given to address the ongoing, global overcapacity crisis.

Downstream concerns are overblown

Concerns about the effects of Section 232 tariffs on downstream industries without exemptions and exclusions in place are also overstated. For example, Constellium, a producer of rolled and extruded aluminum products, recently stated that the Section 232 duties will have “both some positive and negative impacts” and “are structured . . . {to} create opportunities for us.” Similarly, Kaiser Aluminum, characterizes the recent Section 232 actions as “a neutral to positive thing.”

The US International Trade Commission (ITC) has also studied the impact of the Section 232 program on prices. The ITC found that the program contributed to a less than 1% annual increase in domestically produced steel prices. Further, with the expansion of the program to cover derivative products, manufacturers of steel- and aluminum-containing products can now petition to have their products covered by the tariffs. Put simply, there is no reason why downstream production cannot also be kept in or brought back to the United States.

US steel, aluminum shouldn’t be geopolitical pawns

The US sought to replace a couple hundred thousand tons of Russian aluminum in the domestic market following Russia’s invasion of Ukraine in 2022. But that does not explain the significant and continued surge of aluminum imports into the United States. Rather, as shown in the chart above, Canadian and Australian import volumes started increasing after Section 232 exemptions were granted and well before the beginning of the war in Ukraine in February 2022.

To its credit, the Trump administration repeatedly addressed Australian and Canadian violations of informal and formal government-to-government commitments not to increase exports above historical levels. The Biden administration stopped enforcing these commitments on aluminum when it took office. The failure to uphold those commitments and the continued expansion of country-wide carve outs on both steel and aluminum for a larger group of “allies” to achieve other objectives have substantially undermined the Section 232 program’s benefits to the domestic industry and reduced federal government revenues.

In short, it is time to end the era of Section 232 exemptions and exclusions. Watering down Section 232 simply provides incentives for foreign steel producers to undermine US production and reshoring. Strengthening and expanding the Section 232 program is a necessary step to charting a sustainable path forward for the American steel and aluminum industries. It’s also necessary to address global excess capacity.

The financial benefit of tariff revenues should flow to the federal government and domestic industries. They should not help foreign producers who want to profit by undermining the goals of the Section 232 program. And let’s be clear on what those goals are: a stronger and more resilient American steel and aluminum industry.

Editor’s note

This is an opinion column. The views in this article are those of an experienced trade attorney on issues of relevance to the current steel market. They do not necessarily reflect those of SMU. We welcome you to share your thoughts as well at info@steelmarketupdate.com.

Alan Price

Read more from Alan Price