Analysis

February 23, 2025

Final Thoughts

Written by Michael Cowden

The US steel market has whipsawed upward on the prospect of expanded Section 232 tariffs of 25% being applied to imported steel – including downstream goods – on March 12.

I don’t want to go down a rabbit hole here on the separate, blanket tariffs of 25% on Canada and Mexico that could go into effect in early March. Will the threat be lifted from Canada but not Mexico? Could both see another reprieve? I don’t know.

But it seems pretty clear that domestic steel mills have the ear of the Trump administration when it comes to Section 232. The result? The much-anticipated Trump bump has finally arrived – and then some.

In fact, the results of our latest steel market survey reflect one of the biggest inflection points the market has seen in years. I’ll go through some of that below. And I’ll illustrate it with what some of you had to say.

So, without further ado, let’s dive into the data. (By the way, our premium subscribers can find the full survey results here. And if you want to upgrade from premium to executive, please contact SMU sales executive Luis Corona at luis.corona@crugroup.com.)

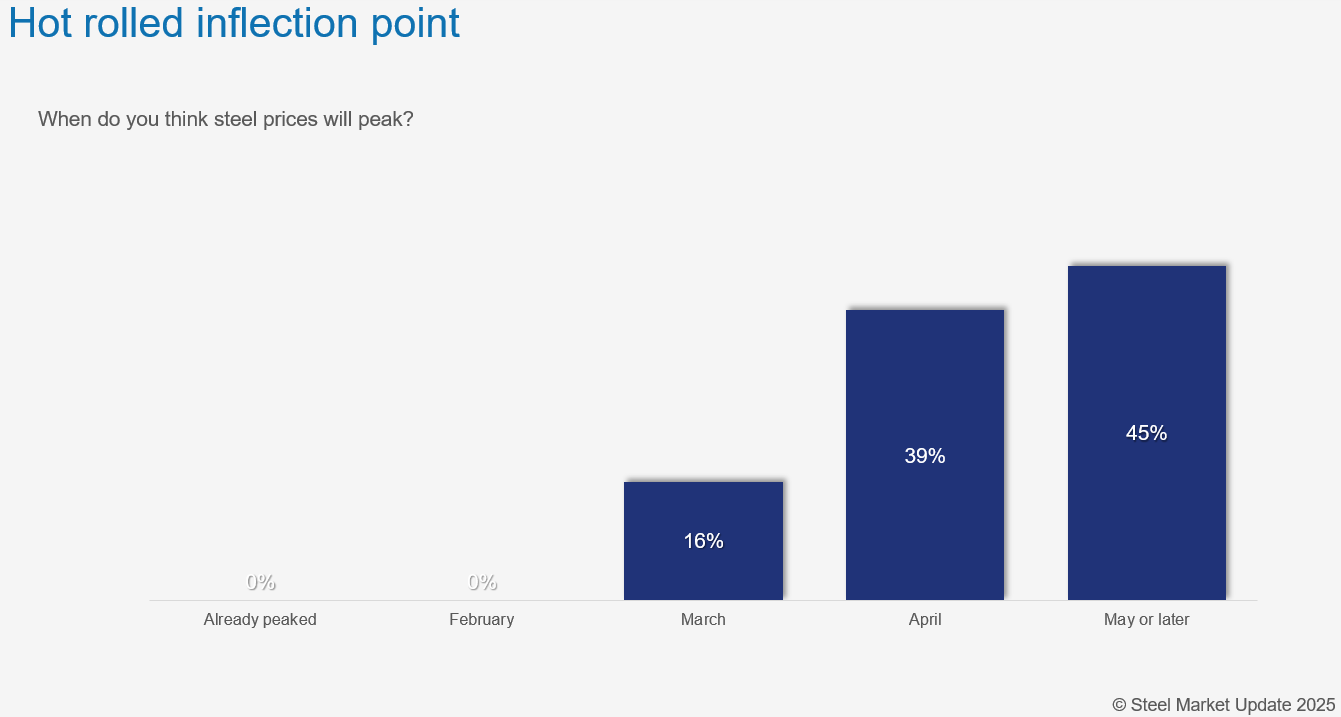

Survey says the market has legs into Q2

For starters, no one – and I mean no one – thinks sheet prices will peak this month. About 39% think the peak won’t happen until April. Another 45% think the market could have legs into May or later. And only 16% think it will peak next month. (Editor’s note: You can click on any of the images below to expand them.)

Here is what some survey respondents had to say:

“When tariffs were applied during Trump’s first tenure, steel prices jumped over $400/t as steel plants took advantage of higher steel import prices.”

“We are in for a supply crunch over the next few months.”

“Tariffs will be in full swing, and mills have open turf to raise prices with seasonal demand kicking in.”

“With the disruption created by threat of tariffs, we could see the market peak moving deeper into Q2.”

“There will be a lot of panic until we see how the tariffs play out and what exceptions are made.”

“Prices are headed north for the foreseeable future.”

“They have not peaked and where they will peak, no one knows.”

Speaking of peaks, not everyone thinks we’re climbing a mountain without one. It might be hard to see the peak right now among the clouds of trade policy uncertainty. But some folks caution that the rules of gravity still apply to the US steel market. Here is what some of them had to say:

“More room to run upwards. But policy is moving very fast and creating a lot of confusion in the short-term.”

“I think the movement so far is gaining traction and by April should be peaked for the summer.”

“Mills are pushing too high, too fast, which will shorten this market cycle.”

“There is a chance it could be May or June. Summer almost always kills a price rally.”

“I think this run has ‘legs’. It is all supply-drive obviously. But the domestic mills will keep raising until they force in imports (with the 25%) and/or more capacity domestically. Neither of which is good long term.”

“Tariffs and sentiment will hit a high. But the reality of excess auto and ag inventories will settle in by April/May.”

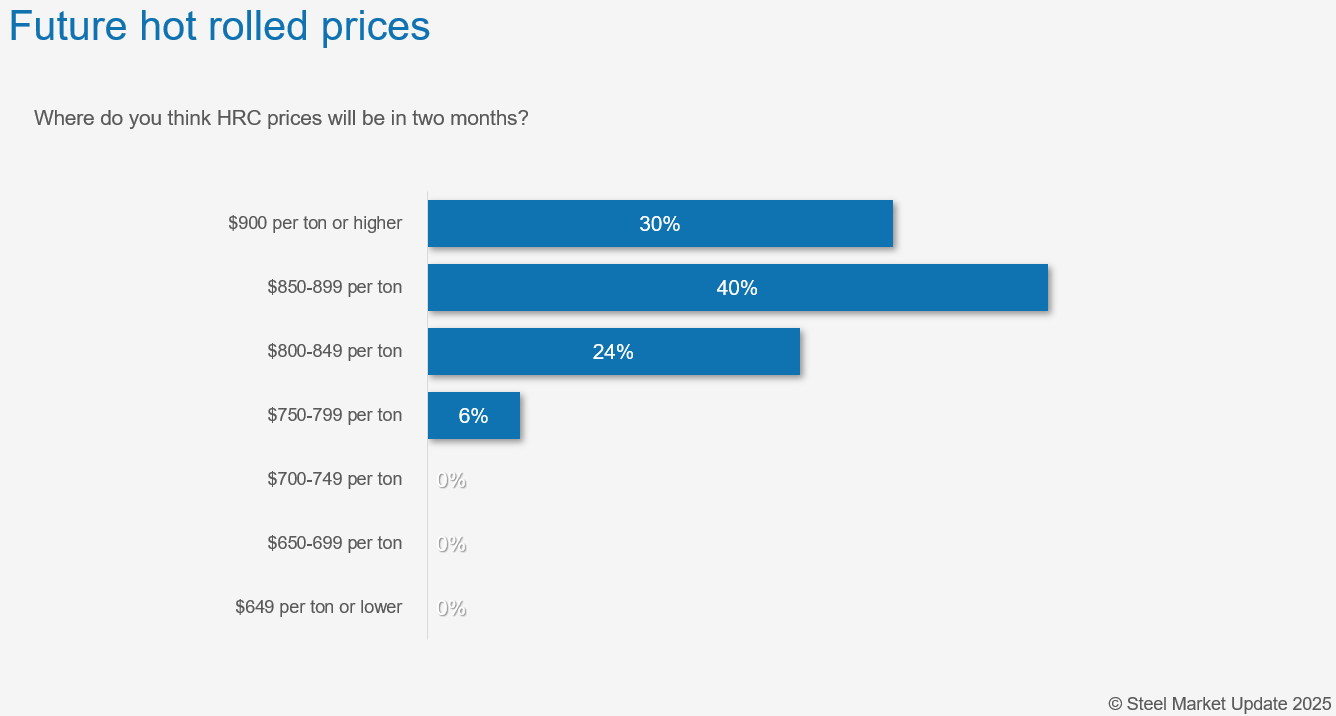

$900/ton – here we come! (Right?)

Next up: How high might HR prices rise over the next two months? This represents another example of the whipsaw we’ve all just experienced.

Nearly 30% of survey respondents think that HR price will be over $900/st two months from now. Rewind to the beginning of the year, and only 5% thought we’d be above $800/st come in early March.

So, let’s appreciate the wisdom of crowds in the comments below. (Let’s also be humble and note that it’s human nature to assume that tomorrow will look more or less like today – which isn’t always the case.)

“They are already transacting in the mid-8s, so around $900.”

“I don’t think the mills will be able to stop raising their prices.”

“Check the pricing from last time tariffs were instituted.”

“Upward pressure from scrap and the market in general.”

“Replacement of USMCA steel and imports – service centers will buy domestic for now.”

“Mills have reported low profits or losses in recent earnings calls. They will use any leverage to increase pricing as far as they can.”

“Tariff contagion is driving market higher.”

“That time of year when certain segments start to take off – i.e., construction, grain bin, culvert, etc. Mill lead times will push out and prices will push up.”

“Could still get over $850. Mill lead times will get pushed out 2 to 3 weeks from all of the buying on CRU based deals. Buyers will want to take advantage of the lower CRU-based deals spurring additional buying – especially on CRU quarterly deals. None of those tons will go unpurchased for March or April based on the lower price pervious months.”

“Prices are headed north for the foreseeable future.”

While most folks remain bullish, some warned that such high prices couldn’t last. Here is what some of them had to say:

“I honestly wouldn’t be shocked if we see things get to or above $1,000/ton. Granted, the inevitable collapse will be just as grotesque.”

“Fundamental demand has not changed, and tariff fearmongering will have run its cycle.”

“Momentum is there now, but resistance will build.”

“Domestic mills really want to push the pricing up. However, the market cannot withstand $900/st +.”

“Turkish HRC is $560 per net ton (nt) ex works. With $80/nt handling/freight, that equals $640/nt times 1.25 tariff = $800/nt for imports.”

Meanwhile, more than 80% of survey respondents tell us they are active buyers. Only 19% say they are on the sidelines. We haven’t seen a result that lopsided in a long time.

Demand reading best since 2021

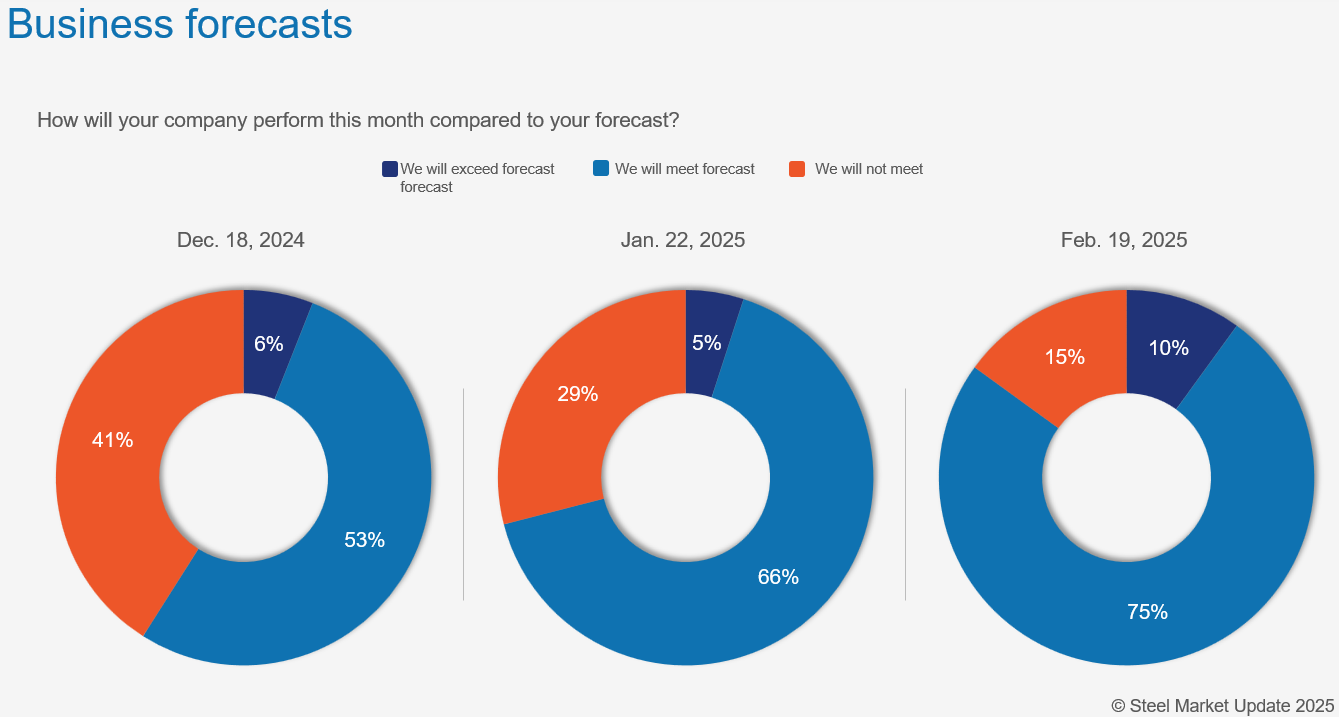

Another bullish signal? Thirty-eight percent of survey respondents tell us that demand is improving. We haven’t seen a result that strong since July 2021, according to the data history here.

What’s more, I’d been writing for most of Q4 that more and more people were reporting missing forecast. That’s no longer the case. For the first time in a while, we see more people telling us that they will meet or exceed forecast.

Here is what some of them had to say:

“Business has more than doubled since Trump was sworn in.”

“It has improved all year, and especially in the last 10 days.”

“Our customers are panic buying.”

But commentary on demand indicates some concerns

Commentary on prices was almost uniformly bullish. It was a little less so in comments about demand, which you can see here:

“Pull ahead demand.”

“We may be pulling forward demand, but our spot activity is off the charts.”

“I see a little bump in demand. But I fear that it’s only future purchases being placed now/pulled in to beat the price increases.”

“Improving relative to 2H of CY24, but typical of recent Q1s.”

“Demand is just ok. The supply side is driving market right now.”

“The forecast for ’25 was good. We’ll see how the recent policy changes affect that forecast.”

SMU Community Chat

Wiley trade attorney Alan Price has some convincing justifications for the revival of Section 232 in a column into today’s issue. And unless something changes, my guess we’re in for some big changes effective March 12.

With that in mind, SMU will host a Community Chat webinar on March 19 at 11 am ET with Alan. That will give us a week to see how the dust settles. And for you to bring some good questions to the Q&A. You can register here.