Analysis

February 11, 2025

Final Thoughts

Written by Michael Cowden

If you’re a mill with melt capacity in the United States, it’s Christmas in February. Section 232 is back – no quotas, no exclusions – and then some.

Before we dive into the details here, I encourage you to check out the official documents posted on the White House website. The text of the executive order (EO) that President Trump signed late on Monday is here. And a fact sheet summarizing the EO is here.

Key dates and features

Let’s start with a key date: Wednesday, March 12, at 12:01 am ET. That’s when these changes to Section 232 go into effect. (That’s assuming there is no last-minute reprieve, as there was with blanket tariffs on Canada and Mexico last week. And that there are no negotiations in the interim for, say, new but lower quotas.)

A lot of the changes basically entail rolling back what I’ll call, for fun, Section 232 Lite. S232 Lite resulted from the watering down of what I’ll call OG S232 – the one first imposed in March 2018. You know, the exemptions and exclusions that accumulated over the years. Now, OG Section 232 is back with its across-the-board 25% tariffs against everyone.

Here are a few key points when it comes to the return of OG S232:

- Mexico and Canada – the United States’ USMCA partners – face 25% tariffs just like everyone else

- Kaput are the quotas that Argentina, Brazil, and South Korea agreed to (or were compelled to accept) in exchange for exemption from the 25% tariff

- Zapped are the TRQs, negotiated under the Biden admin, with the European Union, Japan, and the UK

- No more special exemptions for Ukraine, even though its war with Russia rages on

- Raw materials – whether scrap, iron ore, pig iron, or coking coal – are exempt, despite some initial fears that they might not be

One big change to OG 232 and a key feature of what I’ll call New S232 is this: 25% tariffs will apply not only to semi-finished and finished steel. They will also apply to downstream goods such as fabricated structural steel, prestressed concrete strand, and “others.” That’s according to the White House docs noted above.

MTAGA!

That “others” part is a key detail. Like a lot of you, I was still waiting for clarity about that list of “others” when this article went to press. It is expected to be detailed in annexes that should be published in the Federal Register. So, stay tuned for that.

Here are some other interesting details about New S232.

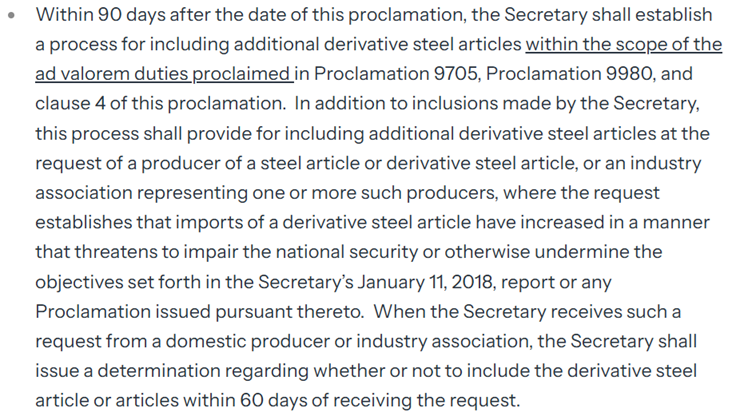

Look at this part of the EO, for example:

That’s basically the opposite of an exemption process. Domestic mills (or groups that lobby for them) can ask that tariffs be applied to downstream goods. Even ones the Trump administration might not have initially thought to include.

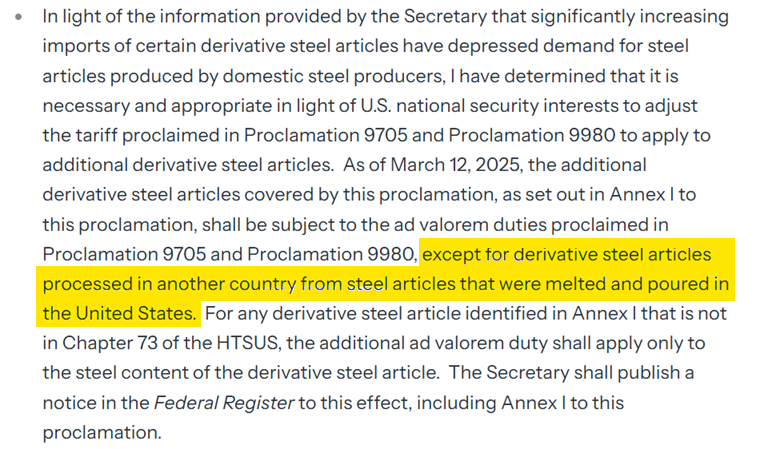

Then there is this one:

Basically, tariffs don’t apply to downstream goods if the material is initially melted in the US, shipped abroad for additional processing, and then shipped back to the US. I’m assuming that was designed with Canada, Mexico, and closely linked North American supply chains in mind.

But what’s to stop someone from, say, exporting US melted product to Greenland (or should I say Red-White-and-Blue Land?), transforming it there, and then shipping it back to the US?

These are the sorts of things – along with the question of “others” – that I can see trade lawyers having a field day with.

Let’s following that train of thought to the end of the line. And let’s say that downstream was to encompass manufactured goods that aren’t made entirely out of steel.

I don’t think it will come to this. But let’s say there was a 25% tariff on passenger vehicles. Would that tariff be based on the value of the car? The value of imported steel and aluminum in the car? Or, idk, the value of a headlight imported from Mexico in a car otherwise made in the US?

What ever happens, this kind of stuff has the potential to Make Trade Attorneys Great Again – MTAGA!

And we look forward to the great coverage that the trade attorneys who write for SMU will have in the weeks and months ahead.

Unintended consequences?

It goes without saying that New S232 will overhaul the steel landscape as we’ve come to know over the last few years.

US slab converters have come to rely on semis from Brazil, which had been subject to a quota but exempt from the 25% tariff. What happens to foreign slabs that are on the water now? What happens to the mills that roll those into sheet and the jobs they support?

Also, it’s hard to overstate how important South Korea, also subject to a Section 232 quota, is as a key supplier to the US market. At first glance, you’d think that a 25% tariff on South Korean material would make prices go up. With South Korea now subject to a 25% tariff, US mills – especially those on the West Coast and Gulf Coast, where import competition is fiercer – should see orders flowing in, right?

But let’s explore another theory. When the quota was in place, it incentivized South Korean producers to charge a premium for the tons sold to the US. Let’s take welded pipe as an example. Couldn’t South Korea take advantage of lower substrate prices in East Asia and send even more pipe (because there are no more quota limits) to the US. And at competitive prices – even with the 25% tariff included?

And what about countries – Turkey, for example – that didn’t have many S232 exemptions and so struggled to compete with countries and regions that had plenty of them. Let’s say the EU, Japan, and the UK with their soon-to-be-gone TRQs. Maybe this New S232 is a net positive for Turkey. Was that the intent? Or an unintended consequence?

Of course, for other regions and countries, perhaps not much has changed – at least not on the steel side. Let’s say you’re a steel mill in Taiwan, which was subject to both steel and aluminum tariffs. Your steel was subject to a 25% tariff… and it still is. It’s a different story on aluminum, however. Your tariff is going from 10% to 25%. You probably have to make up that 15% by raising prices – like, now.

And then there is the question of whether this is all the start of a negotiating process. Sort of like what happened in 2017-2018. Maybe this time the goal is to try to get better terms for the US when USMCA comes up for review in 2026? Or perhaps it’s to get countries such as Brazil and South Korea to accept lower quotas?

Even as more details emerge, so much is still unknown. Love him or hate him, Trump has given us no shortage of things to write about. It is a gift that will keep on giving when it comes to steel news.

The rumor mill

I’d gotten some questions from some of you about why it took so long to get written confirmation of what Trump said on Sunday (while flying to the Super Bowl on Air Force One) about steel and aluminum tariffs. Apparently, POTUS got ahead of his skis on Sunday. And his staff had to scramble to backfill his words with the requisite paperwork. (If you covered OG S232 in 2017-18, this is déjà vu all over again.)

As far as rumors go, there had been one that New S232 would come on top of OG S232 – leading to cumulative duties of 50%. Looks like that was fake news. But 50% can still in theory be imposed if circumstances are deemed to warrant it – as happened with Turkey in August 2018.

SMU Ferrous Scrap Survey

SMU unveiled the results of its inaugural ferrous scrap survey in February. We’ll be conducting others every month from here on out.

The scrap survey adds to our suite of “premium” products. That includes our steel market survey (sentiment, lead times, negotiation rates, etc.) as well as our data on service center flat-rolled steel inventories. You can see the latest results here.

Think of our surveys as an early-warning system for market inflection points. We let you know when the big waves are coming before they crash into shore. And we now offer that service all along the ferrous supply chain.

If you’d like to learn more, or to upgrade from executive to premium, please contact SMU senior account executive Luis Corona at luis.corona@crugroup.com.

And thanks, from all of us at SMU, for your continued business. We really do appreciate it.