Market Data

February 6, 2025

SMU Survey: Mill lead times fluctuate, extensions expected

Written by Brett Linton

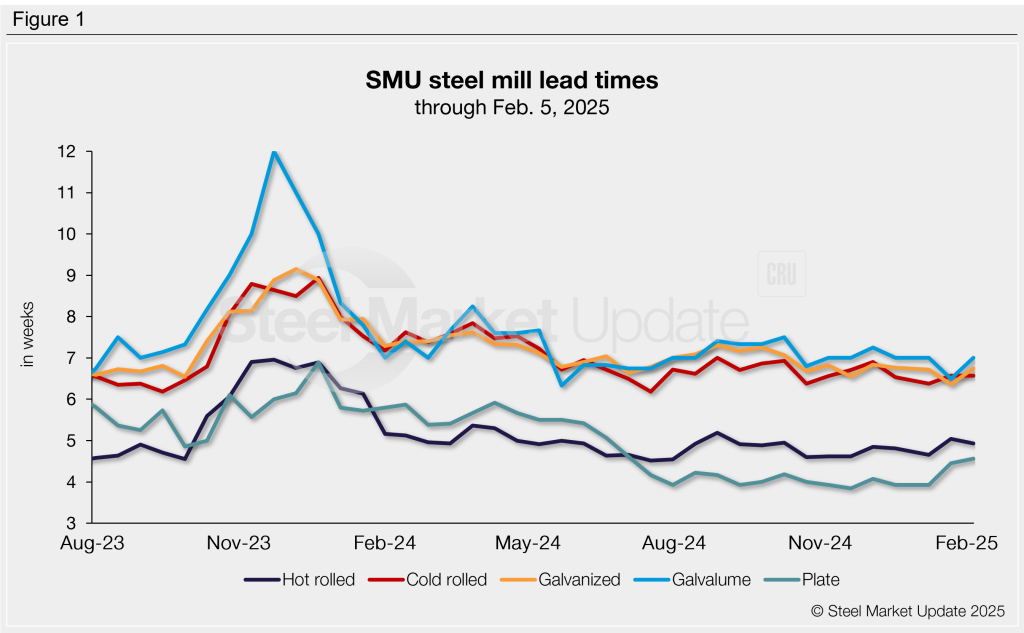

Buyers responding to our latest market survey reported that steel mill lead times were relatively flat this week for most of the sheet and plate products tracked by SMU. While we have seen some movements in recent weeks, production times remain within a few days of the lows observed over the last two years, a trend observed since mid-2024.

Following the mild extensions seen in our Jan. 22 survey, lead times for hot-rolled, cold-rolled, and plate products saw little change this week. Meanwhile, lead times on galvanized and Galvalume products increased by almost half a week each, both previously at multi-month lows.

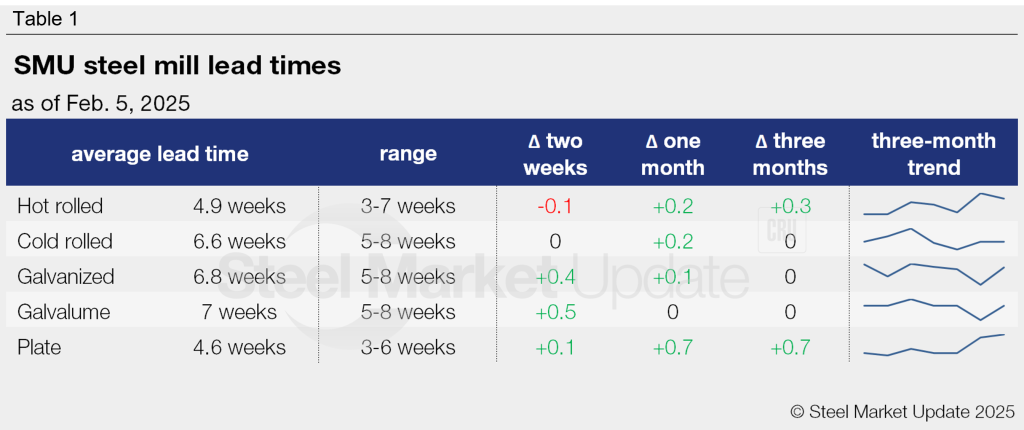

The average lead time for hot-rolled steel is just under five weeks. Tandem product lead times range from six and a half to seven weeks. Plate lead times now average four and a half weeks.

Table 1 summarizes current lead times and recent trends.

Compared to our Jan. 22 market check, all of our lead time ranges have shifted this week:

- Hot rolled: Our range widened from four to six weeks to three to seven weeks.

- Cold rolled, galvanized, and Galvalume: The shortest lead time in each range increased from four weeks to five weeks.

- Plate: The shortest lead time in our range rose from two weeks to three weeks.

Future predictions

The majority of the respondents we surveyed this week (62%) foresee longer lead times two months from now, up from 51% two weeks ago. Just over a third (36%) expect production times to hold steady, down from 47% previously. A small remainder continues to believe lead times could contract further. (The full results of our survey are available here for our Premium members).

Here are some of the comments we collected:

“There must be a little pent-up demand that will cause prices and lead times to increase in the next few months.”

“Prices and lead time usually go in lockstep. As prices increase, lead times are likely to edge out, but I expect movements to be moderate.”

“If prices rise and more orders are placed lead times could extend.”

“As prices go up, mill leads should extend. If they don’t, price increases will not stick.”

“Extending, demand increase with less supply from offshore.”

“I think lead times will extend in the next month and then flatten.”

“We have not been able to get any mill to quote [galvanized] pricing or lead times in the past week. Everyone has been waiting for the market to react to tariffs (and now the lack of immediate tariffs).”

“Too much open capacity currently with more slated to come online.”

“Domestic lead times are still short in historical terms and mills seem hungry too.”

Trends

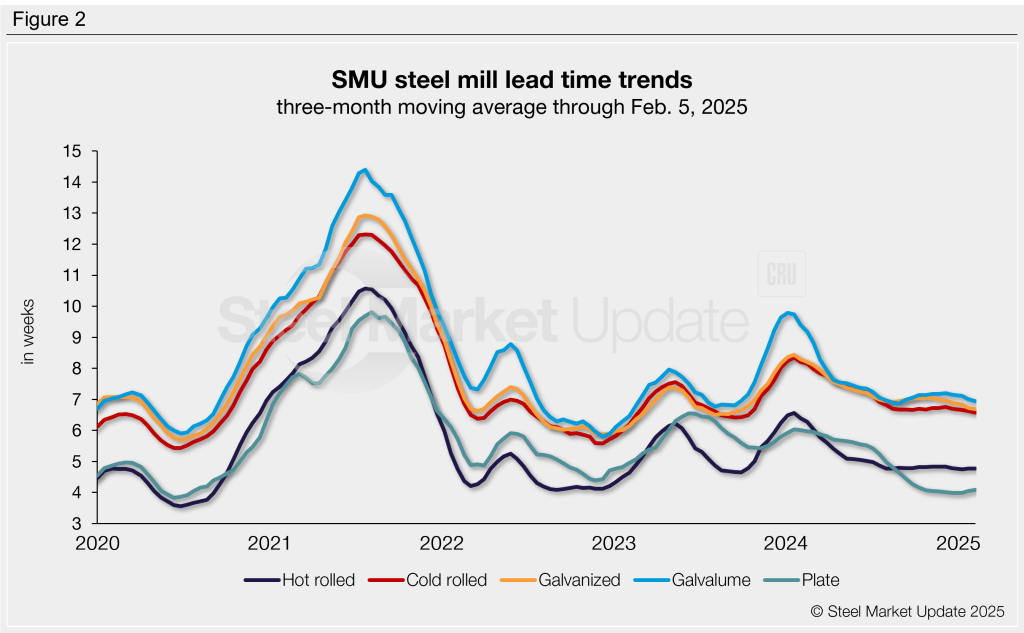

To smooth out variability seen in our biweekly data and highlight trends, lead times can be calculated on a three-month moving average (3MMA) basis. Through this week, 3MMA lead times for both sheet and plate products saw little movement from January. Overall, 3MMA lead times have trended lower across the past year, flattening out in the last few months, and remaining at or near one-year lows (Figure 2).

The hot rolled 3MMA is now at 4.77 weeks, cold rolled at 6.57 weeks, galvanized at 6.69 weeks, Galvalume at 6.94 weeks, and plate at 4.09 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.