Prices

February 6, 2025

HR Futures: What’s next for HRC and busheling prices?

Written by Joshua Toney

Since the publication of our last market update on Dec. 10, several notable developments have shaped the landscape. A new president has been sworn in, headlines continue to stir up concerns around tariffs, and both Nucor and Cleveland-Cliffs have announced new offer levels.

Additionally, the launch of the CME Busheling (BCH) contract, based in Chicago, adds a fresh layer to the market. How have these factors impacted HR futures? Despite the expansion in contango, the market has largely remained rangebound throughout the period.

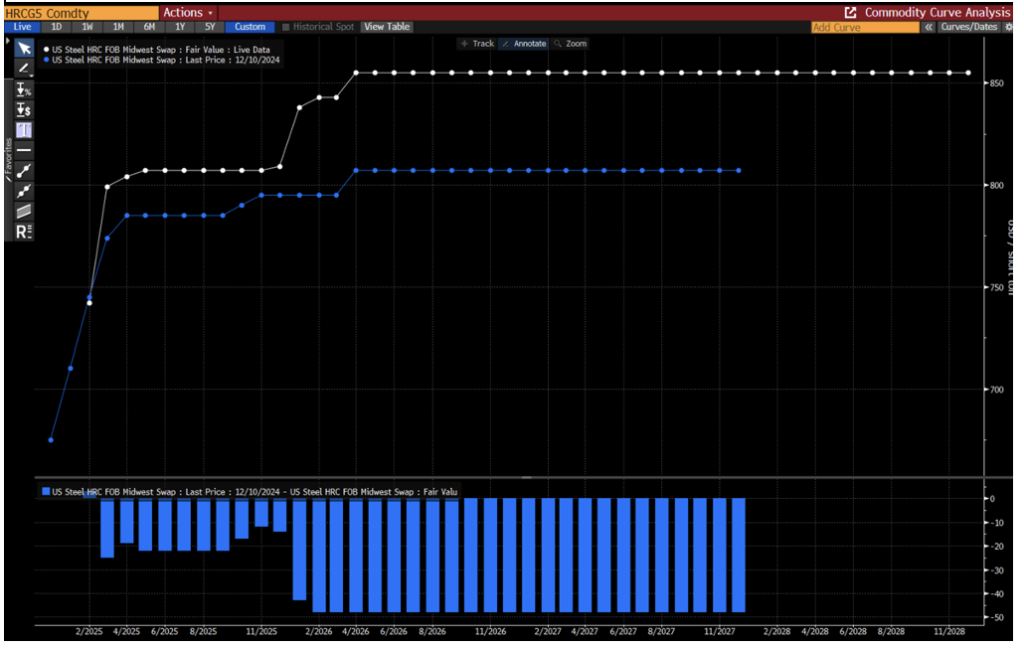

Looking at the historical curve changes from Dec. to Feb 3, there has been a modest shift, with a delta of $50 per short ton (st). This reflects a rate of change of $25/st per month, equating to a 3.3% change per month when considering M1 futures prices.

While one might expect more substantial fluctuations in times of heightened market stress – especially with tariff headlines in the mix – the HRC market has yet to see significant volatility. The underlying HRC Index has remained below $700/st, aside from the potential print expected this Wednesday.

Absent major price action, especially outside of trades from H2’25, the market is still seeking a clear catalyst. However, it’s important to note that futures markets are quick to react to new data points, and a shift could occur with little notice.

CME HRC commodity curve structure change Dec. 10, 2024. to Feb. 3, 2025

Source: Bloomberg

One significant factor driving the strength at the back end of the curve is Feb.’25 scrap strength, a result of winter weather conditions and limited mill flows. Prime scrap for Jan.’25 rose approximately $20/st. Feb.’25 physical trades are in the midst of negotiations which basis price action in BUS & BCH indicate further strength.

Tariffs remain a key focus, but as yet, there have been no significant price movements in the physical market. Cleveland-Cliffs’ offer level remains steady at $800/st, as first published on Dec. 13, while Nucor raised its offer by $15/st on Feb. 3, to $775. Considering the short month of February, a $44/st average on the weekly CRU print will be needed to bring futures and index prices in line.

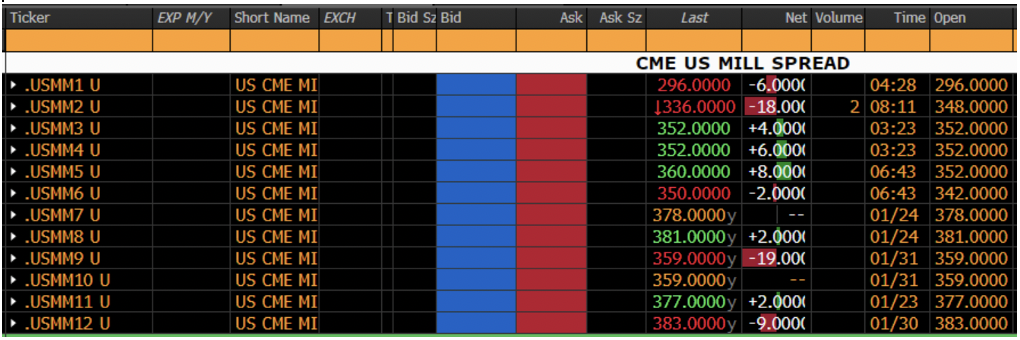

An interesting development is the relationship between Chicago and Midwest Busheling contracts. Since January 2019, the spread between these contracts has fluctuated between -$7.91 per gross ton (gt) (Chicago over Midwest) to +$40.97/gt (Midwest over Chicago).

Currently, the spread stands at approximately $15/st, with Midwest Busheling priced higher than Chicago futures. This dynamic presents a potential opportunity for market participants to capitalize on shifts in these spreads.

CME BUS/BCH curve structure Feb. 3, 2025

Source: Bloomberg

For those looking to trade futures, the BUS/BCH arbitrage strategy stands out as a potential avenue to express a view on the expansion or contraction of underlying price spreads. Additionally, positioning a BUS/BCH trade against the HRC market could allow participants to capture the mill spread, providing a further layer of potential profitability.

In summary, the market remains relatively quiet. However, there are underlying shifts that present opportunities for those willing to watch the futures pricing closely. The interaction between CME HRC and CME Busheling contracts is likely to evolve further, as traders monitor the changing dynamics of the scrap and tariff landscape. With a few key developments still on the horizon, the market could see significant movement should these factors trigger a more pronounced shift.

CME HRC – CME BCH price curve Feb. 4, 2025e

Source: Bloomberg

Marex CDD Report Disclaimer:

This report was approved and issued by Marex Financial, a company within the Marex group. Marex Financial is incorporated under the laws of England and Wales (company no. 5613061 and VAT registration no. GB 872 8106 13), is authorised and regulated by the Financial Conduct Authority (FCA registration number 442767) and is a member of the London Stock Exchange. Marex Financial’s registered address is at 155 Bishopsgate, London, EC2M 3TQ. Nothing in this report constitutes (i) an offer of services, (ii) an offer to purchase or sell investments or any other product or (iii) investment, tax or legal advice. The report has been approved and issued on the basis of publicly available information, internally developed data and other sources believed to be reliable. It has been prepared for the general information of Marex’s institutional clients, is not directed at retail customers and does not take into account particular investment objectives, risk appetites, financial situations or needs. Recipients should make their own trading decisions based upon their own financial objectives and financial resources. This report is a marketing communication. It is not investment research and has not been prepared in accordance with legal requirements designed to promote investment research independence. The report is not subject to any prohibition on dealing ahead of the dissemination of investment research. Whilst reasonable care has been taken to ensure that facts stated are fair, clear and not misleading, Marex does not warrant or represent (expressly or impliedly) their accuracy or completeness. Any opinions expressed are those of the author of the report as at the date of the report and not necessarily those of Marex and, in any event, may be subject to change without notice. Marex accepts no liability whatsoever for any direct, indirect or consequential loss or damage arising out of the use of all or any of the data or information in this report. This report is not intended to be an offer to buy or sell any securities of any company referred to herein nor any other transaction or investment. This report is not intended for use by any other person than the addressee. If you are not the addressee, please delete it and immediately notify the Group Compliance department at Marex. This report may not be distributed in any jurisdiction where its distribution may be restricted by law. Additional material relating to any security, transaction or investment referred to in the report may be made available on request. No part of this report may be redistributed, copied or reproduced without the prior written consent of Marex. You must not distribute any part of this report to any other person without attaching a copy of this information.