Market Data

January 24, 2025

SMU Survey: Steel Buyers' Sentiment Indices slip

Written by Brett Linton

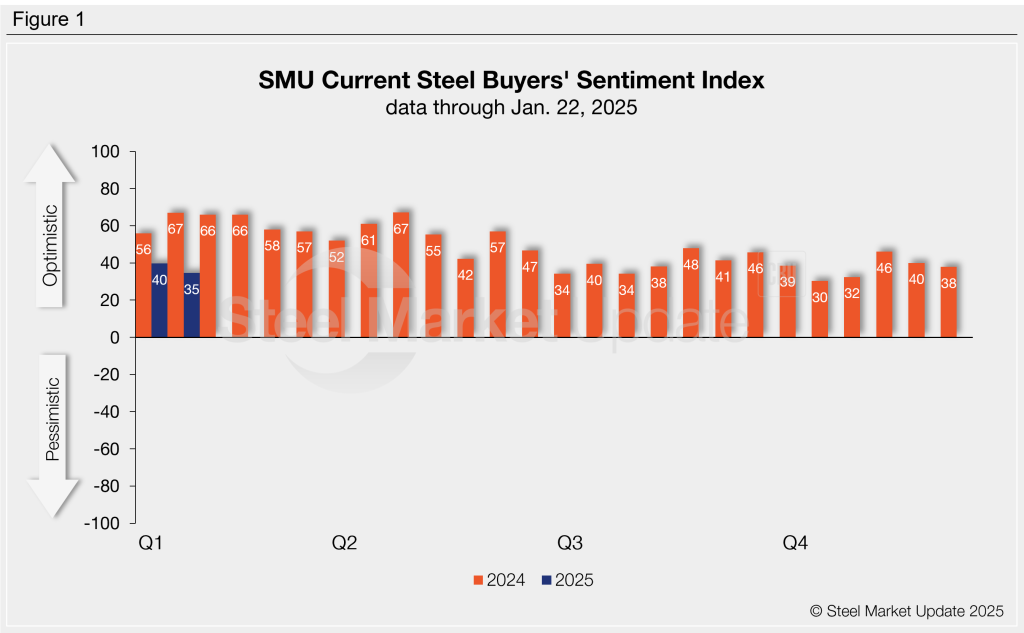

SMU’s Steel Buyers’ Sentiment Indices saw a slight decline this week, slipping to levels last observed in early November. Despite the dip, both of our Sentiment Indices remain in positive territory and indicate that steel buyers remain optimistic about their businesses’ prospects.

Every two weeks, we survey hundreds of steel buyers asking how they rate their companies’ chances of success in today’s market and their expectations for three to six months down the road. From this data we calculate our Current Steel Buyers’ Sentiment Index and our Future Sentiment Index, metrics tracked since 2008.

Current Sentiment

SMU’s Current Buyers’ Sentiment Index indicates that buyers remain optimistic, though slightly less confident than they were over the two prior months, and significantly less than this time last year.

Current Sentiment fell five points this week from early January, now standing at +35 (Figure 1). Since July 2024, Sentiment has consistently hovered within a few points of a multi-year low. Across 2024, we saw Current Sentiment average +48.

Future Sentiment

SMU’s Future Buyers’ Sentiment Index also reflects that buyers maintain a positive outlook for early 2025, slightly better than they felt at this time last year.

This week, Future Sentiment eased two points from early January to +66, the lowest mark recorded since early November’s +56 (Figure 2). Recall that back in mid-December Future Sentiment rose to a one-year high of +73, having averaged +65 across 2024.

What SMU survey respondents had to say:

“I think the change of the guards will help the momentum of our industry.”

“The threat of Trump tariffs on Canadian goods is causing a downturn.”

“We are forecasting increased activity in H2.”

“Weak demand is still the case, weak prices too.”

“Winter slowdown in part, plus waiting for President Trump to take office and stimulate the economy in multiple ways.”

“Price-cost squeeze.”

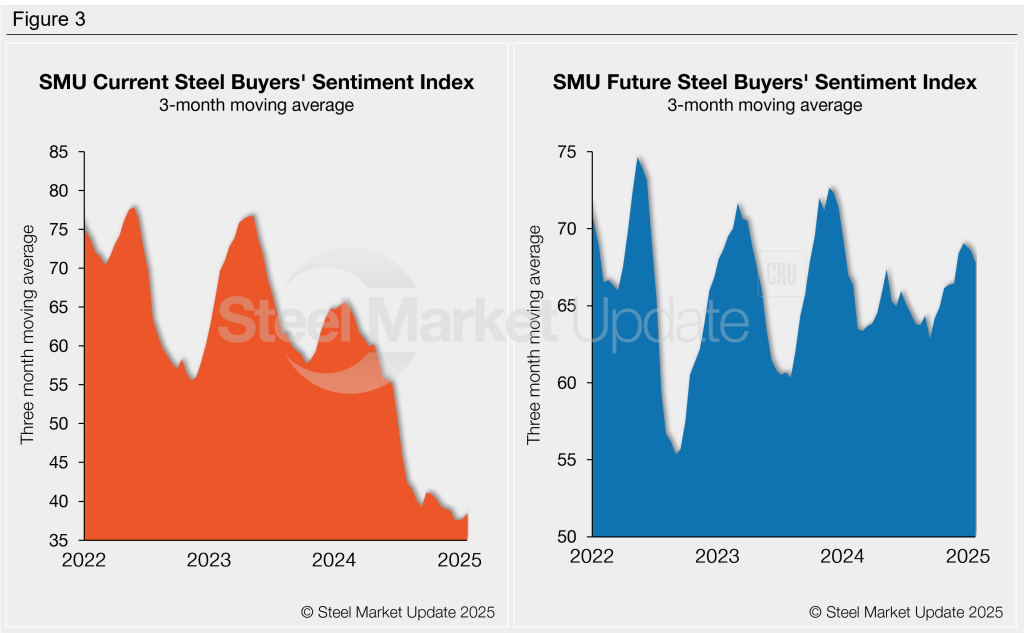

Sentiment trends

When analyzed as a three-month moving average, Steel Buyers’ Sentiment moved in opposing directions this week compared to two weeks prior (Figure 3).

The Current Sentiment 3MMA rose to +38.44 as of Jan. 22, less than one point higher than the four-year low recorded in mid-December. This marks nearly a yearlong downward trend.

Meanwhile the Future Sentiment 3MMA continued its gradual decline from mid-December’s 11-month high, easing to +67.79 this week.

About the SMU Steel Buyers’ Sentiment Index

The SMU Steel Buyers Sentiment Index measures the attitude of buyers and sellers of flat-rolled steel products in North America. It is a proprietary product developed by Steel Market Update for the North American steel industry. Tracking steel buyers’ sentiment is helpful in predicting their future behavior. A link to our methodology is here. If you would like to participate in our survey, please contact us at info@steelmarketupdate.com.