Market Data

December 19, 2024

SMU Survey: Buyers report mills are slightly less flexible on pricing

Written by Brett Linton

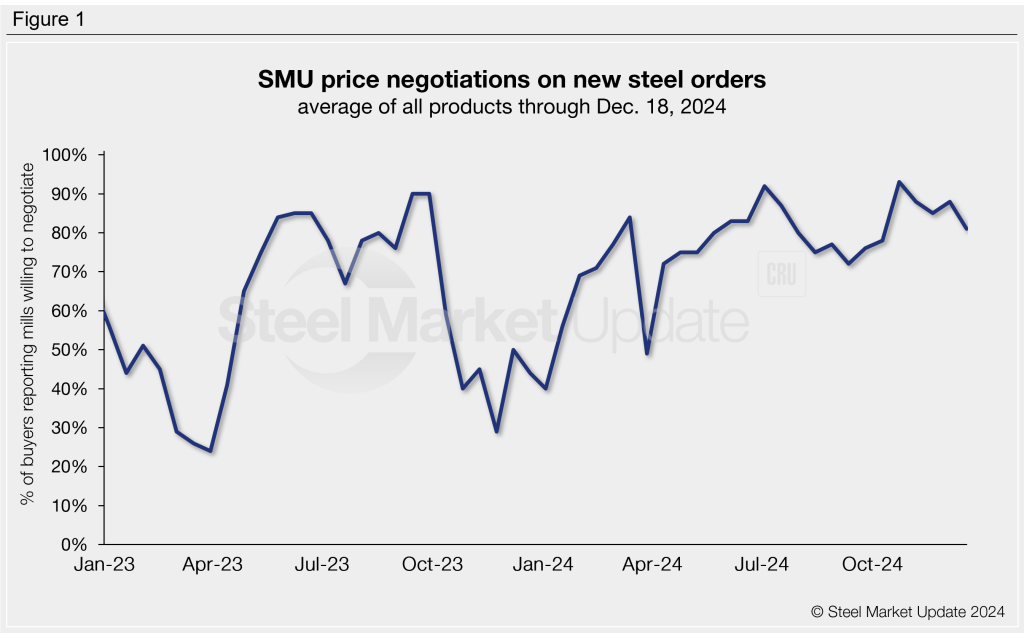

Steel buyers of sheet and plate products say mills are still willing to bend on spot pricing this week, though not quite as much as they were two weeks prior, according to our most recent survey data. Negotiation rates have been high for the majority of 2024, especially in the latter half of the year.

SMU polls hundreds of service center and manufacturer buyers every other week asking if domestic mills are open to negotiation on new spot order prices. This week, about four out of every five buyers we surveyed reported that mills would talk price to secure a new order (Figure 1). This 81% rate has marginally declined since reaching a multi-year high of 93% in late October. At this time last year, we saw much lower negotiation rates (40-50%).

Negotiation rates by product

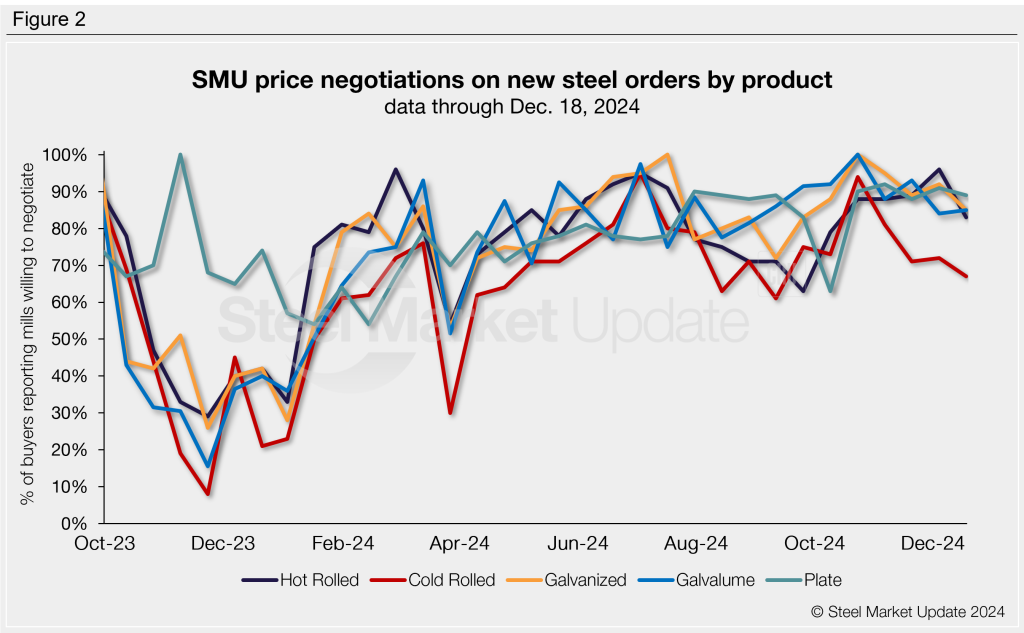

Negotiation rates on sheet and plate products remain high, as seen in Figure 2. Rates were highest for hot rolled, coated, and plate products. Cold rolled negotiation rates have marched to the beat of a different drum since the start of November. Negotiation rates by product this week are:

- Hot rolled: 83%, down 13 percentage points from Dec. 4, and the lowest rate recorded since early October.

- Cold rolled: 67%, down five percentage points to a three-month low.

- Galvanized: 85%, down seven percentage points to a near-three-month low.

- Galvalume: 85%, up one percentage point.

- Plate: 89%, down two percentage points.

Here’s what some survey respondents had to say:

“Willing to move hot rolled to get orders.”

“Not all mills are negotiable on galvanized, but there are three or four willing to offer deals.”

“Negotiable on plate with tons.”

“One mill negotiated on galvanized, two others did not, multiple transactions.”

“Some, but not all, flexible on hot rolled prices.”

“All based on how much and who you are buying from, major mills seem to be less willing to negotiate on hot rolled.”

“Selectively on plate and perhaps short lived.”

“The main plate mills we deal with have all been asking for orders these past few weeks.”

Note: SMU surveys active steel buyers every other week to gauge their steel suppliers’ willingness to negotiate new order prices. The results reflect current steel demand and changing spot pricing trends. Visit our website to see an interactive history of our steel mill negotiations data.