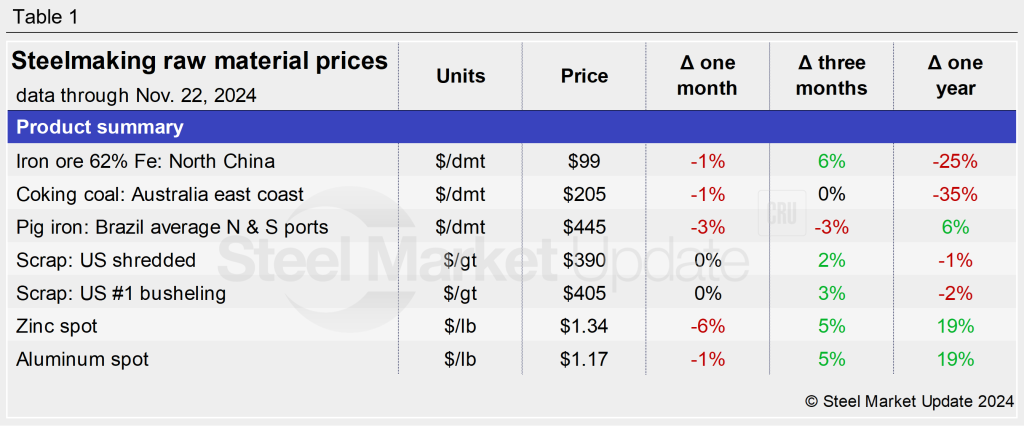

Prices

November 25, 2024

Steelmaking raw materials prices ease in November

Written by Brett Linton

Prices were stable to down in November for all seven steelmaking raw materials tracked by SMU, according to our latest analysis.

Through Nov. 22, prices for zinc, pig iron, iron ore, coking coal, and aluminum all declined month over month (m/m), while steel scrap prices held steady.

Prices for six of the seven raw materials are the same or higher than they were three months ago, with some products rising as much as 5-6% in that time. Table 1 summarizes the percentage changes from one month, three months, and one year ago for each product.

Iron ore

The import price of 62% Fe Chinese iron ore fines eased slightly following a three-month high in mid-October. As of Nov. 20, the weekly spot price was $99/dmt delivered North China (Figure 1). Iron ore prices are 6% higher than they were three months ago, yet still 25% below this time last year.

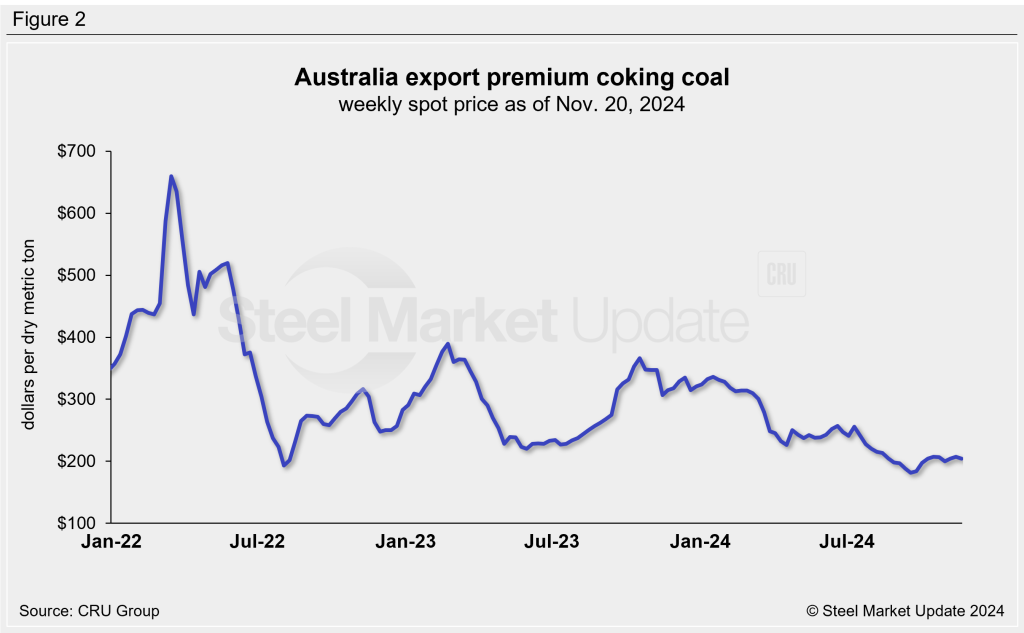

Coking coal

Prices for premium hard coking coal have generally declined across the last year, reaching a three-year low of $182/dmt in mid-September. Prices have ticked higher over the past two months, coming in at $205/dmt as of last week (Figure 2). Coking coal prices are now similar to those seen three months ago, but are 35% lower than they were one year prior.

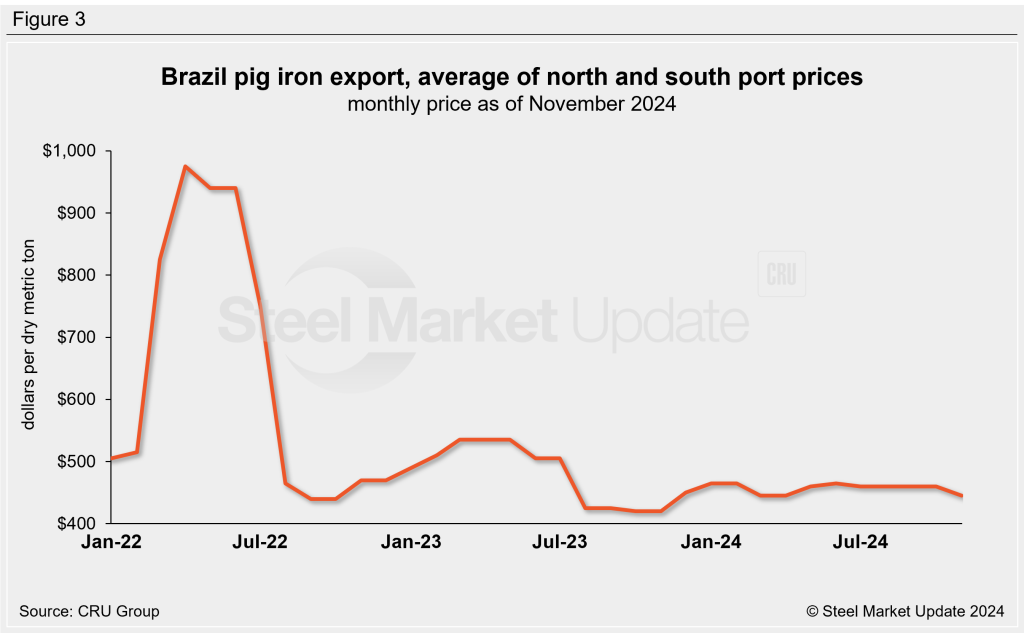

Pig iron

Pig iron prices have stabilized throughout the past year, hovering within a $35/dmt range in the past 15 months. Prices eased 3% from October to November to a seven-month low of $445/dmt, previously unchanged since July (Figure 3). Pig iron prices are 6% higher than levels one year ago.

Recall that pig iron prices jumped more than 60% in April 2022 following the invasion of Ukraine by Russian forces, reaching a historic high of $975/dmt. Most of the pig iron imported to the US had come from Russia, Ukraine, and Brazil. This report uses Brazilian prices, averaging north and south port prices.

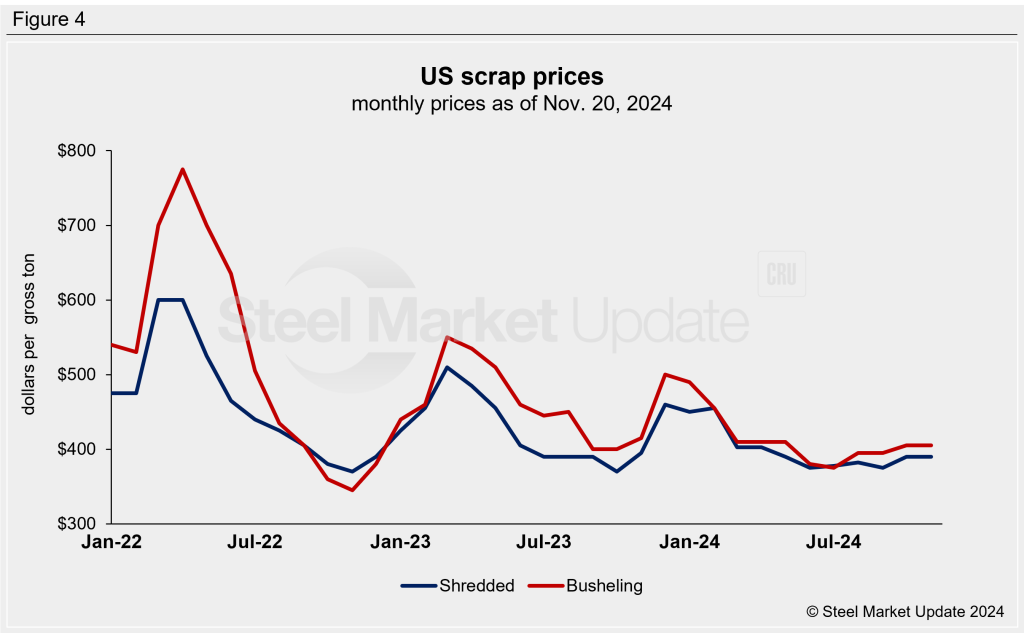

Scrap

Following a peak last December, steel scrap prices trended lower across the first seven months of this year, but have shown some signs of recovery more recently. SMU’s busheling and shredded scrap indices marginally increased from September to October and remained steady in November. Busheling scrap is at $405 per gross ton (gt) and shredded scrap is at $390/gt (Figure 4). Scrap prices are 2-3% higher than three months ago, but 1-2% lower than they were at this time last year.

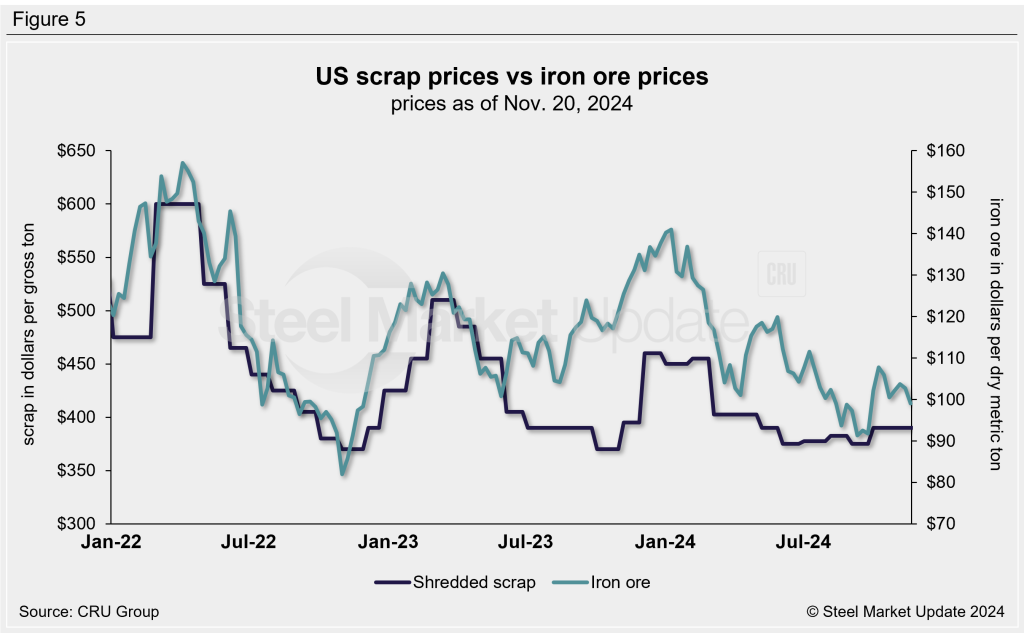

Changes in the relationship between scrap and iron ore prices offer insights into the competitiveness of integrated (blast furnace) mills, whose primary feedstock is iron ore, compared to mini-mills (electric-arc furnace), whose primary feedstock is scrap. Figure 5 compares the prices of mill raw materials over the past few years.

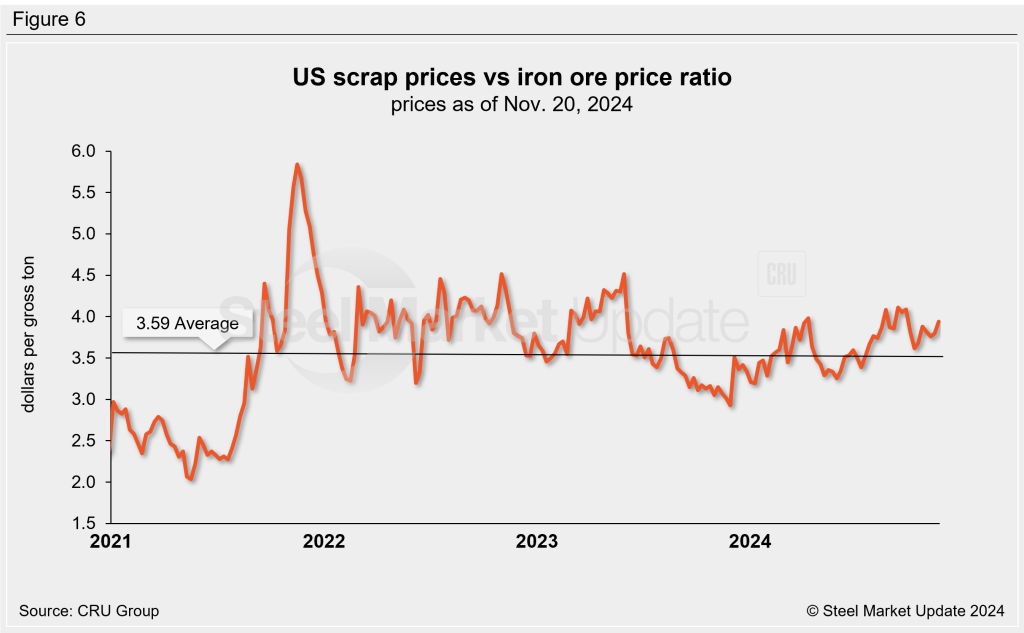

To compare these two feedstock materials, SMU divides the shredded scrap price by the iron ore price to calculate a ratio. A high ratio favors the integrated producers and a lower ratio favors the mini-mill producers.

As shown in Figure 6, integrated mills had mostly held the cost advantage between late 2021 through mid-2023. The advantage then briefly shifted to mini-mill producers in the second half of last year. After bobbing up and down this year, the ratio has favored integrated mills for the past few months. The latest ratio is up to 3.94.

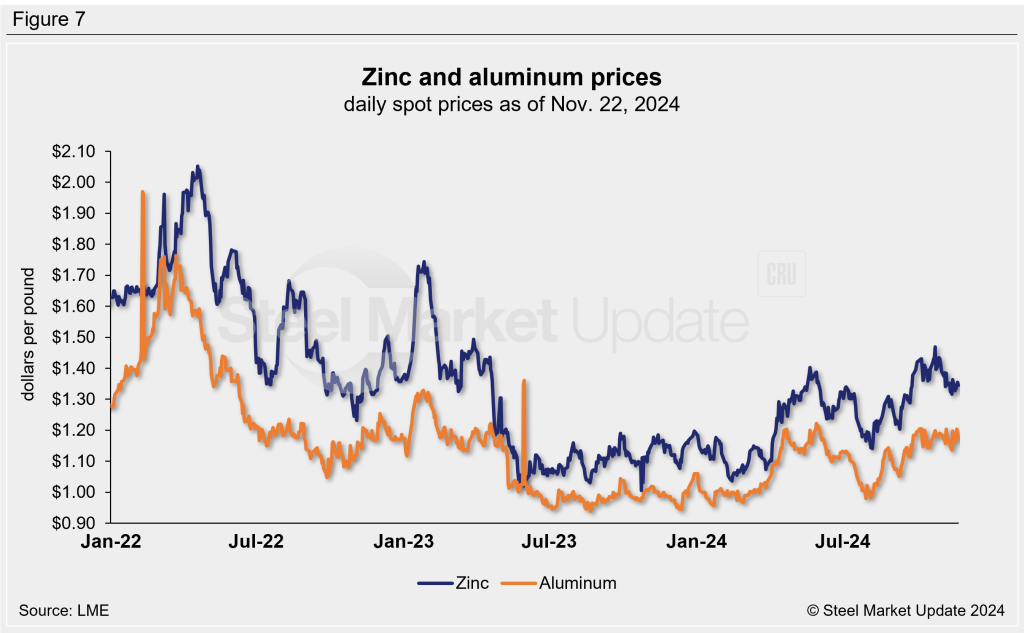

Zinc and aluminum

Zinc is used in galvanized and other coated steel products. Prior to April, zinc spot prices had been relatively stable for almost a year. Prices then surged in April and May, prompting some mills to increase their galvanized coating extras, but they then trended lower through early August. Prices have since begun to rally again, climbing to a 19-month high of $1.47/lb in late October. The latest LME cash price for zinc is down 6% m/m to $1.34/lb as of Nov. 22. Zinc prices are 5% higher than levels three months earlier and are up 19% compared to November 2023 (Figure 7).

Due to higher zinc prices, one confirmed mill, Nucor, increased its galvanized coating extras this week. We will publish an article comparing its new and previous extras in our upcoming Executive newsletter.

Aluminum prices, which factor into the price of Galvalume, have trended similarly to zinc prices. Aluminum prices climbed to a one-year high of $1.22/lb in May, receded through August, and then climbed again. The latest LME cash price of $1.17/lb has remained relatively stable since late September, down just 1% m/m. Aluminum prices are 5% higher than tags three months ago and 19% greater than levels seen this time last year. Note that aluminum spot prices sometimes have large swings and return to typical levels within a few days, as seen twice in Figure 7.