Analysis

November 20, 2024

CRU: Trump tariffs could stimulate steel demand

Written by Josh Spoores

Now that the dust has settled from the US election, as have the immediate reactions in the equity, bond, and commodity markets, this is a prime opportunity to look at how a second Trump presidency might affect the US steel market. The focus of this Insight is to look past the near-term disruptions and reactions surrounding the return of President Trump and analyze the potential for a meaningful impact that might come over the next two to four years of his presidency.

On the campaign trail, President Trump consistently spoke of using tariffs as the primary tool of his economic platform. He advocated for the liberal use of tariffs as a means to support manufacturing and economic growth in the US, as well as a way to lower or end income taxes. While the latter of these is not economically feasible, the former does have the potential to create a positive impact, though it will take time and patience. That said, per CRU’s initial comments at the time of the election, tariffs have the potential to stoke inflation and damage longer-term prospects for spending. Equally, retaliatory behavior and a ‘trade war’ would have a seriously negative impact on global and US growth. However, the US impacts would be less due to trade being a much smaller proportion of its economy.

Trump is no stranger to tariffs

Maslow’s hammer states, “If all you have is a hammer, everything looks like a nail.” Tariffs are President Trump’s hammer. In 2018, during Donald Trump’s first presidency, he implemented a 25% tariff on nearly all steel imports based on the grounds of national security via Section 232 (S232) of the Trade Expansion Act of 1962. Implementing these tariffs immediately led to higher prices, as they restricted the steel supply for US buyers. Steel prices then fell back as y/y growth of durable goods in the US fell from a monthly average of 3.1% in 2018 to -2.8% in 2019.

Tariffs on steel face diminishing marginal utility

Over the past several years, the S232 tariffs did ease for some ally countries and some buyers that were able to gain an exclusion. However, restricted steel supply and the fallout from the Covid-19 pandemic combined, allowing domestic steel mills in the US to earn record profits through the early 2020s. These tariffs and subsequent pandemic-era profits led to many mills building new capacity in a very strategic manner. This new capacity was designed to produce value-added products efficiently, at a competitive cost, and in a geographically relevant location.

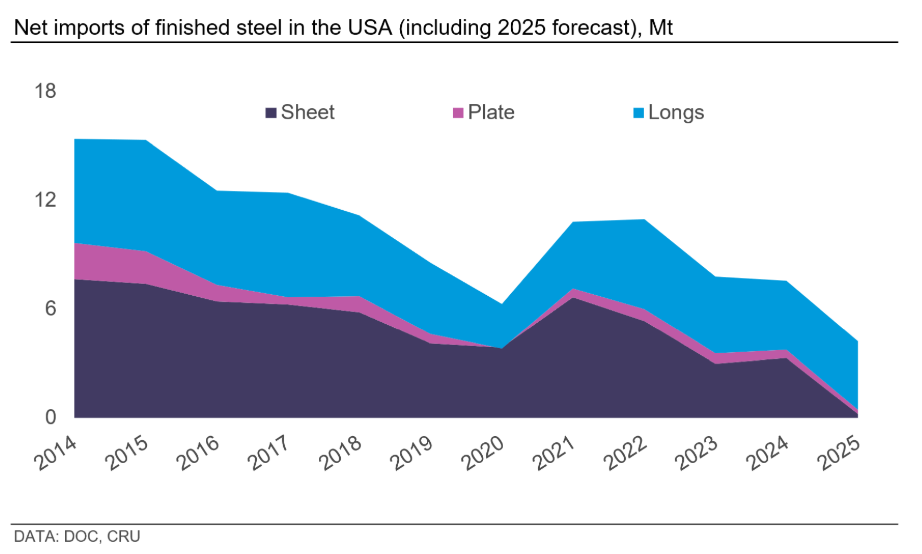

Today, this new capacity continues to come online while more is under construction. Due to the rise of this competitive capacity, domestic mills have been taking market share away from foreign imports. So while President Trump could reimpose some steel tariffs, the rapid buildout of new steel capacity in the US has already shifted market share gains to domestic mills, per the following chart. This gain in domestic market share clearly shows the diminishing marginal utility of further tariffs on steel.

Trump will continue to wield tariffs as his Maslow Hammer

On the campaign trail, President Trump continued promising the use of tariffs. However, we expect they will be used differently and instead support steel consumption via manufacturing rather than just the steel producers. Tariff-related campaign promises centered around a broad use of tariffs, such as a 20% blanket tariff on all imported items and a 60% tariff on all imports from China. During one speech, President Trump talked about implementing 200% tariffs on all John Deere products imported into the US. In that same speech, he said he would also apply this style of tariffs on all vehicles imported from Mexico.

Manufacturing-based tariffs could create a significant structural shift in steel demand

Where tariffs on steel lead to restricted supply and higher steel prices, this ultimately drives more imports of steel-intensive goods. President Trump is now looking at an alternative option that would support demand for steel. That option is to wield Maslow’s hammer and implement tariffs on imported manufactured goods with the goal of driving the production of these goods back to the US.

Additionally, he spoke about BYD, the world’s largest EV maker. BYD is building a manufacturing facility in Mexico, and while President Trump has threatened BYD, he was also very quick to propose that BYD build a factory in the US.

President Trump is unique in terms of the scale of approach used to encourage new foreign direct investment into steel-intensive manufacturing alongside pressuring companies to reshore. If reshoring investments in the US do take place, we could see domestic demand for steel rise at a faster rate than expected. One caveat to this is that this style of investment and shifting of supply chains will take time. A wave of investment is likely to first stimulate demand for steel-containing capital-intensive goods as new factories are built. A structural shift in steel demand for domestic manufactured goods is expected to take longer. That said, this shift could be undermined if inflationary pressure rises significantly.

There is considerable uncertainty over the level and scope of any tariffs, although steel-containing goods from exporting regions with a trade surplus to the US are most likely to be targeted and be areas of opportunity for US manufacturers to capture market share.

In summary, expect tariffs with the potential to generate demand-side support

A second Trump presidency carries the possibility of invigorating manufacturing in the US via both reshoring and stimulating foreign direct investment. This end goal may be achieved through a variety of means, but most importantly via tariffs on imported goods, particularly from specific manufacturing hubs that enjoy a trade surplus with the US, such as China and Mexico. Coupled with the Republican sweep of the Senate and House, President Trump may have a tremendous amount of political will to drive through significant policy. The first impact may be on capital goods as factories are built, with demand for steel from manufacturing output following later. That said, the wider impact of domestic inflation and retaliation by trade partners has the potential to limit any upside and could, indeed, lead to a more negative outcome.

This Insight was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.