Prices

September 12, 2024

HR futures: Higher on news of Cliffs furnace idling

Written by Mark Novakovich

It had been a relatively quiet and steady CME HRC futures market since the end of August. That was upended by Thursday’s news that instead of a two-week maintenance outage, Cleveland-Cliffs would hot idle the C-6 blast furnace at its Cleveland Works for an uncertain period of time.

HR futures up!

The CME October HRC contract, HRCV4, gained $22 per short ton (st) on the day to provisionally close at $744/st on Thursday. The first and second quarter futures strips of 2025 gained $25/st and $24/st to provisionally settle at $823/st and $829/st, respectively.

Despite today’s rally and firmer tone, front-month futures still remain below the 30-day highs reached in mid-August, when October HRCV4 settled $765/st. But the December HRZ4 has gained approximately $35/st since last writing to provisionally close at $810/st on the day.

Futures volumes saw some healthy days toward the end of August. A two-month high of 72,000 st traded on Aug. 21. But the momentum was largely short-lived as market participants attended the SMU Steel Summit in Atlanta on Aug. 26-28.

The first half of September had been relatively quiet until the past few days, with daily average traded volumes failing to break 35,000 st for all but two days since Aug. 22. And several days saw less than 18,000 st traded. But Wednesday saw the biggest volume day since August 21, with over 50,000 st trading as financial players came in to sell March through May positions in 2025.

Open interest now stands at just over 490,000 st. Commercial participation remains lackluster, as physical trading is also said to be subdued. End-user buyers remain cautious amid weak manufacturing demand and sufficient existing inventories at service centers.

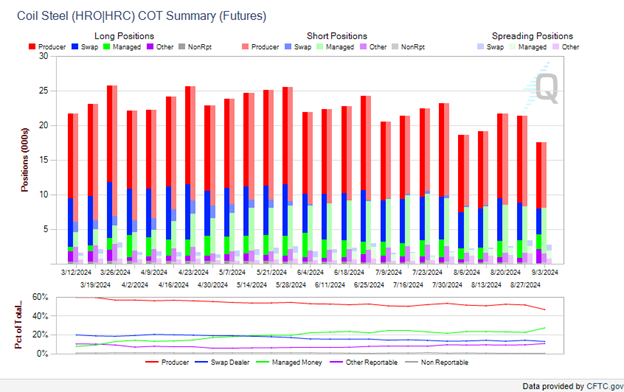

As noted in the table below, the CME’s Commitment of Traders (COT) report shows not only a decline in overall net open positions in the HRC contract over the past six months but also declining commercial open interest. Meanwhile, the managed-money category of traders continues to increase its share of open interest.

Wildcards: Coated trade case and USS furnaces

It remains to be seen whether the Cleveland-Cliffs furnace idling proves to be a bullish catalyst. The fundamental background on the demand side remains somewhat bearish. But fresh concerns about the supply side are supporting the futures curve and may provide some weight to mill price hikes.

There are also worries about the scope of the recent trade case, filed jointly by US mills and the United Steelworkers (USW) union, against imports of coat flat-rolled steel. All that comes in addition to ongoing uncertainty over the fate of U.S. Steel’s blast furnaces. Those factors combined have given futures sellers higher targets for the time being.

Scrap futures kaput?

The CME’s busheling scrap contract (BUS) continues to suffer from illiquidity and declining interest. The most recent September settlement price was disputed by several market participants as not being representative of the underlying physical market, which reportedly saw cash prices as flat or lower in many markets – notably Chicago and Detroit. With only 43,00 gross tons of open interest and long stretches of trade inactivity, numerous participants have disregarded the futures as they await CME Group’s proposed changes to the contract’s specifications.

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed should not be treated as a specific inducement to make a particular investment or follow a particular strategy. Views and forecasts expressed are as of date indicated. They are subject to change without notice, may not come to be, and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.