Market Data

August 15, 2024

SMU survey: Lead times remain short, slight uptick on HRC and plate

Written by Brett Linton

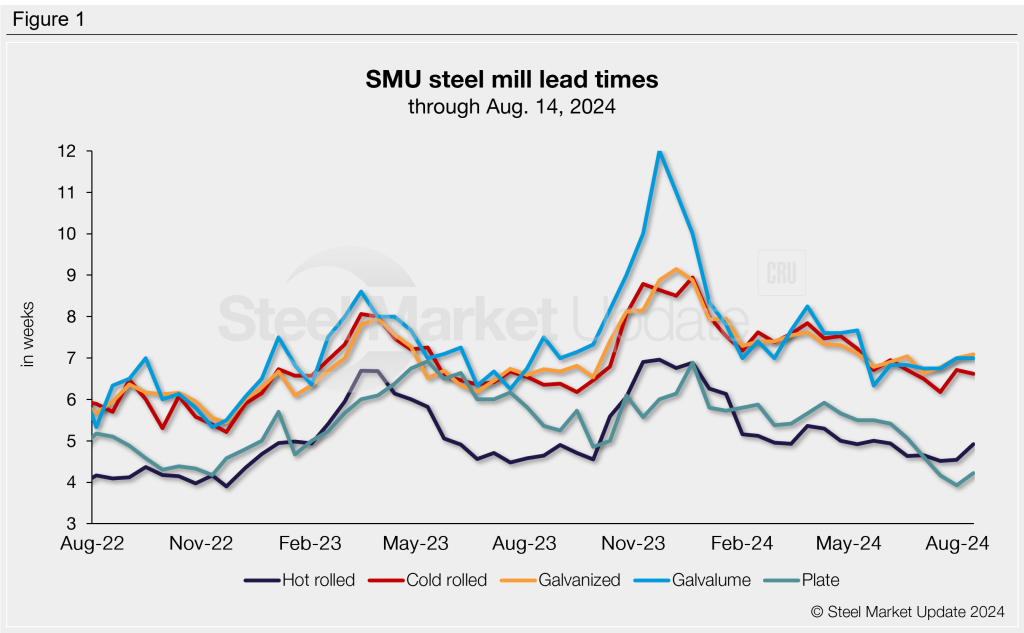

Steel buyers continue to report short mill lead times for both sheet and plate products, according to SMU’s latest canvass of the market. Lead times for hot-rolled and plate products marginally increased from our late July survey, likely due to limited restocking in anticipation of upcoming mill outages for scheduled maintenance. Lead times for tandem products saw little change from our previous market check. While lead times on all products are slightly extended compared to levels of a month ago, they remain near historical lows.

Table 1 below summarizes current lead times and recent trends.

The upper and lower limits of our lead time ranges have extended for all products compared to our late July data. The longest lead time in our HR range has increased from six weeks to seven weeks. The upper range for all tandem product lead times has extended from eight weeks to nine weeks. And the bottom end of our plate lead time range has risen from two weeks to three weeks.

Survey results

Just over half of the companies we surveyed this week remarked that current mill production times were shorter than usual. The remainder responded that lead times were within normal levels, while 3% commented they were slightly longer.

We also asked buyers where they think lead times would be two months from now. The majority of our respondents (66%) believe lead times will be flat through October (vs. 62% in our prior survey). Only 29% forecast production times will extend in that time (down from 33% previously), while 5% expect them to shrink further (unchanged from late-July).

Here’s what respondents are saying:

“Flat, unless mills reduce capacity to match poor demand…”

“Lead times will remain short. Some outages at Nucor pushed out lead times but demand has not improved. Still decent demand but the lead-time adjustment had more to do with supply.”

“Lead times are leveling off.”

“Contracting, all based on lighter demand in Q4.”

“There remains too much available capacity out there with more coming online. No reason to see things extended from here.”

“I don’t think Q4 will have long lead times, mills will want to fill tonnage.”

Figure 1 below tracks lead times for each product over the past two years.

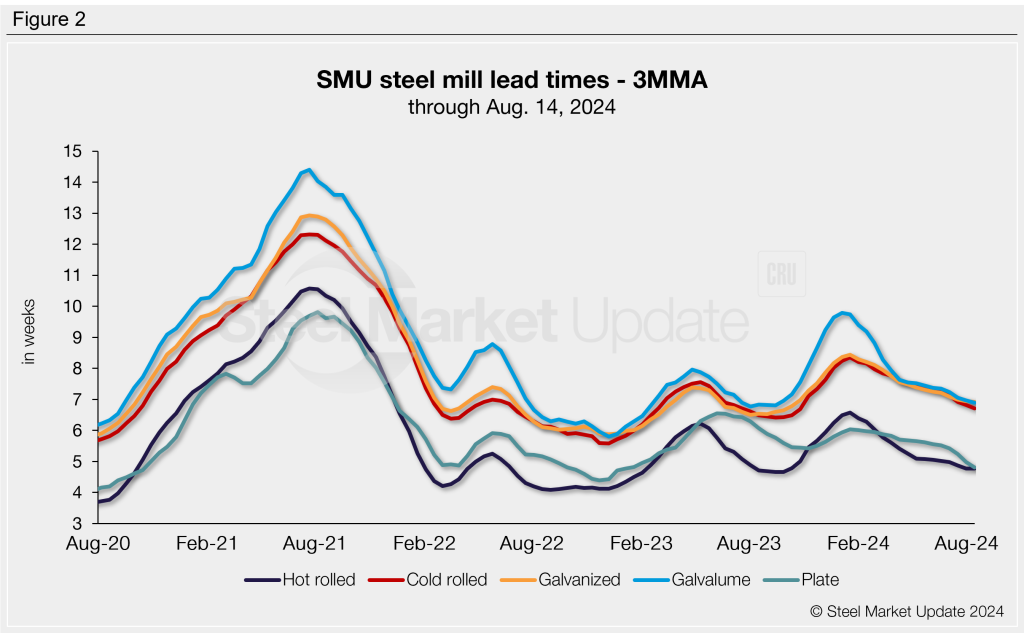

3MMA lead times

To better highlight trends, we can view lead time data on a three-month moving average (3MMA) basis and smooth out the variability seen in our biweekly readings. Through this week, 3MMA lead times ticked lower for all products, now at low levels not seen since September and October 2023. This downward trend has been evident for the last six months.

The HR 3MMA lead time is now down to 4.77 weeks, cold rolled is at 6.70 weeks, galvanized at 6.92 weeks, Galvalume at 6.90 weeks, and plate at 4.80 weeks.

Figure 2 highlights lead time movements across the past four years.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.