Government/Policy

July 9, 2024

May steel exports slip to 4-month low

Written by Brett Linton

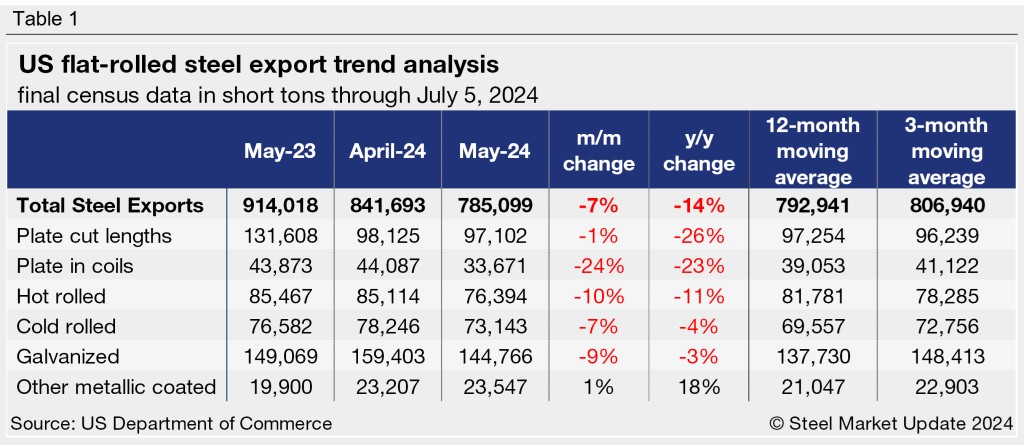

Total US steel exports slipped 7% month-on-month (m/m) to 785,000 short tons (st) in May, according to the latest Department of Commerce data. Following April’s eight-month high, May represents the second-lowest monthly export rate of the year, only greater than January’s 771,000-st level.

Steel exports averaged 806,000 st per month in the first five months of 2024, 1% lower than the same period last year. Total May exports are 14% lower than the same month last year, when we saw a near five-year high rate of 914,000 st.

Monthly averages

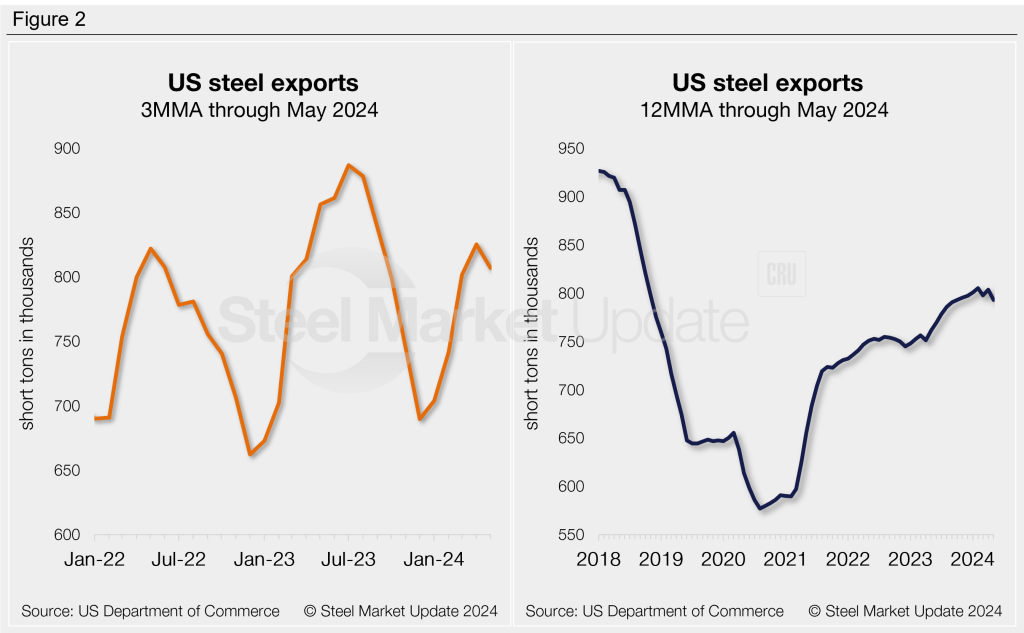

Looking at exports on a 3-month moving average (3MMA) basis can smooth out the monthly fluctuations. Exports had trended downward throughout the second half of 2023, falling to an 11-month low in December. The 3MMA changed course as it entered 2024, rising each month through April. The latest 3MMA through May remains strong at 807,000 st, down 2% from April’s seven-month high.

Exports can be annualized on a 12-month moving average (12MMA) basis to further dampen month-to-month variations and highlight historical trends. From this perspective, steel exports have steadily trended upwards since bottoming out in mid-2020. The 12MMA reached a 5.5-year high in February at 805,000 st. This measure remains elevated through May at 793,000 st.

Exports by product

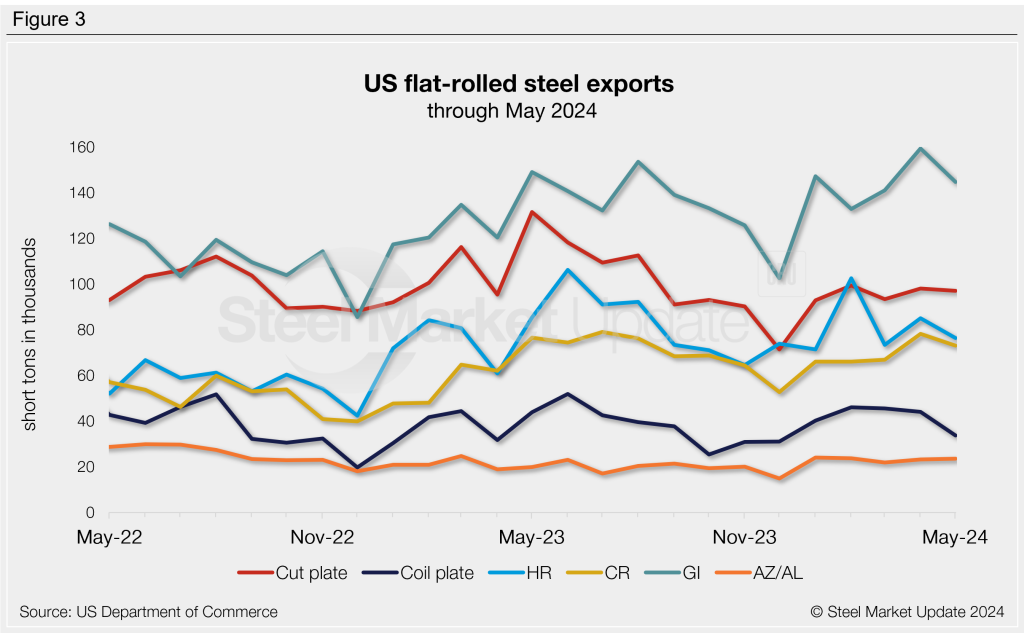

Exports of most major flat-rolled steel products saw m/m declines. The biggest monthly movers were plate in coils (-24%), hot rolled (-10%), galvanized (-9%), and cold rolled (-7%). The only product to increase from April was other-metallic coated (+1%).

Significant year-on-year (y/y) decreases were seen in exports of plate cut lengths, plate in coils, and hot rolled, with all experiencing double-digit declines. Other-metallic coated steel was the only product with a y/y increase.

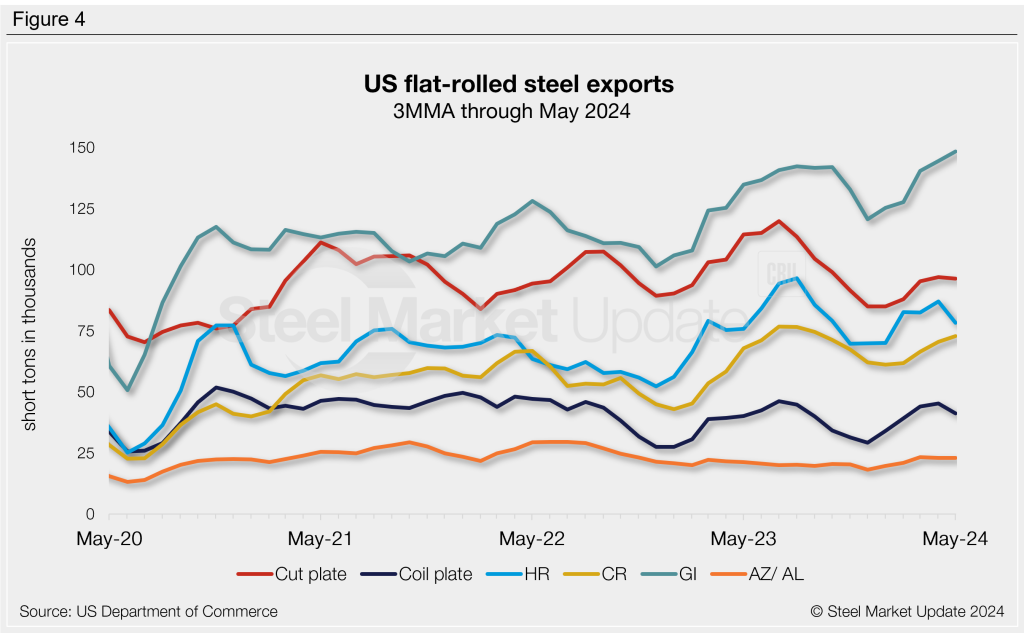

On a 3MMA basis, export levels were mixed across the sheet products we track. Exports of hot rolled, plates in coils, and plate cut lengths eased from April to May. Other metallic coated exports were flat m/m, while cold rolled and galvanized products increased. Recall that a month ago, 3MMA rates for all products other than other metallic coated were at multi-month highs.

Note that most steel exported from the US is destined for USMCA trading partners Canada and Mexico. In May, 48% of all exports went to Mexico, followed by 44% to Canada. The next largest recipients were Brazil, China, and the Dominican Republic at less than 1% each.