Sheet

June 12, 2024

SMU Steel Demand Index edges up, remains near a 12-month low

Written by David Schollaert

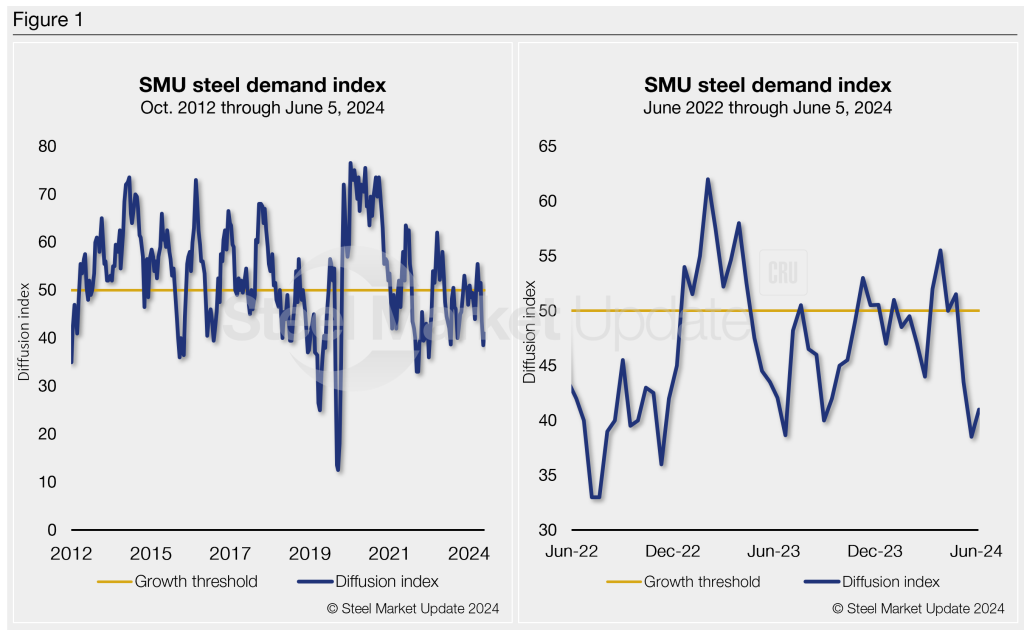

Steel Market Update’s Steel Demand Index moved up 2.5 points last week, though it remains in contraction territory and at one of the lowest readings in nearly a year, according to our latest survey data.

SMU’s Steel Demand Index now stands at 41, up from a reading of 38.5 at the end of April. The increase was marginal, keeping the index to its lowest measure since August 2023.

The reading – down 14.5 points from a recent high of 56 in March – keeps signaling lower demand, as prices and lead times continue trending lower.

Methodology

The index, which compares lead times and demand, is a diffusion index derived from the market surveys we conduct every two weeks. This index has historically preceded lead times, which is notable given that lead times are often seen as a leading indicator of steel price moves.

An index score above 50 indicates rising demand and a score below 50 suggests declining demand. Detailed side by side in Figure 1 are both the historical views and the latest Steel Demand Index trend.

Current dynamics

Declining prices and slumping demand turned the index to contraction and an 18-month low last month. And it came after a brief stint of growth from early Q2 buying and mill price hikes. The short-lived boost has given way to a bearish undertone with prices and lead time ticking down.

Some may even suggest that the summer doldrums came knocking early this year.

The trend is aided by sheet buyers continuing to find mills willing to talk price, and SMU’s Current Buyers’ Sentiment recovering slightly after dropping last month to its lowest mark since August 2020.

Lead times continue to hover around five weeks on average – where they’ve been for the better part of the past four months – while hot-rolled (HR) coil ticked down to $710 per short ton (st) FOB mill, east of the Rockies. That’s down $20/st week on week and down $135/st from a recent high of $845/st in early April, according to SMU’s latest check of the market on Tuesday, June 11.

It’s not all bad news. Despite the lower reading, 71% of survey respondents still report stable or improving demand. But, 29% are reporting declining demand, a one-percentage point decrease from late last month.

Despite that, it’s notable to highlight index has been in growth territory only a handful of times since late April 2023. All those gains have been short-lived bumps when the market responded to mill price hikes over the past year.

Apart from those short-lived rallies, SMU’s Steel Demand Index has trended downwards and into contraction territory for significant clips over the past year.

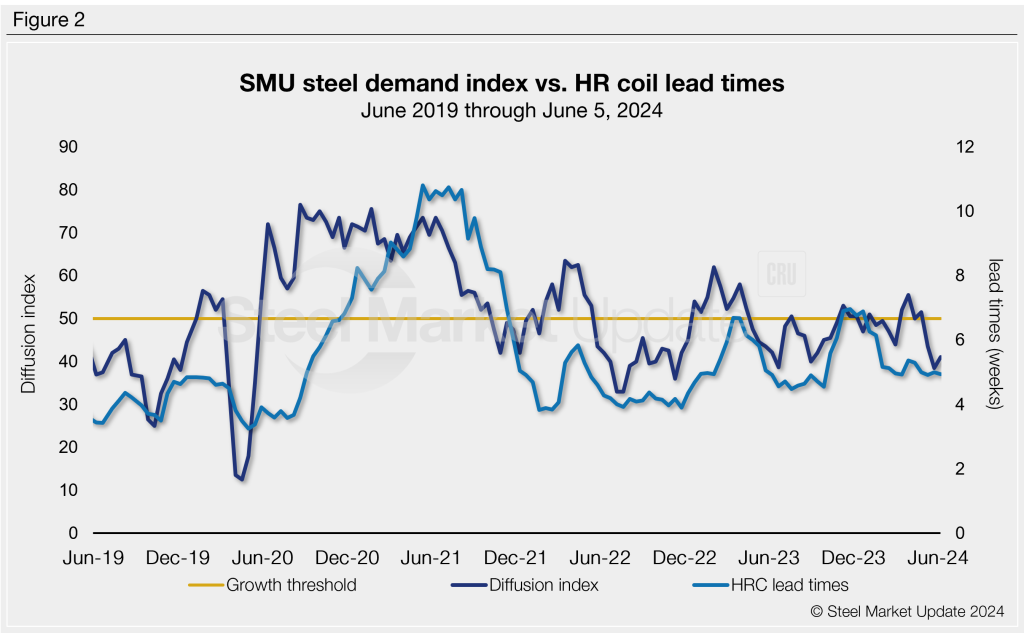

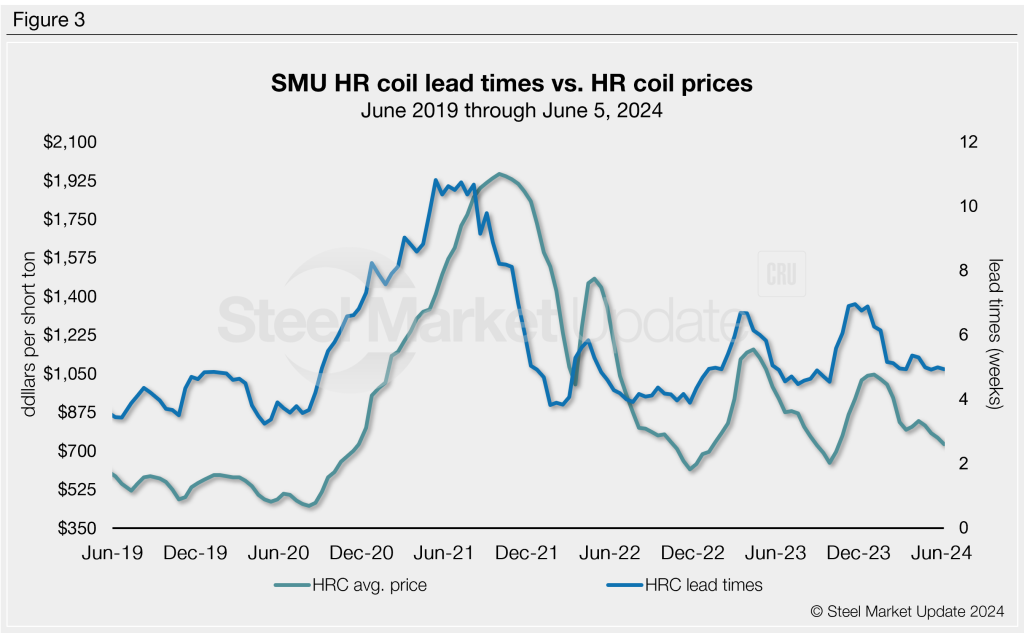

SMU’s demand diffusion index has, for nearly a decade, preceded moves in steel mill lead times (Figure 2), and SMU’s lead times have also been a leading indicator for flat-rolled steel prices, particularly HRC (Figure 3).

What some SMU survey respondents had to say

“Steady but still tenuous.”

“Not up but at least holding the line.”

“Customers are cautious now. The economy is slowing and projects delaying.”

“Transactional has seen a decline, contract has been stable.”

“Just meeting contract minimums, so not leaving anything for spot.”

“Tough to tell for certain, but we think of it as near-term softness.”

“It has seemed to be declining all year.”

“Stable to declining, no big bright spots out there right now.”

“Seeing a slowing of the market on contract business now. Spot sales are essentially non-existent.”

“We saw a decline for June with spot buyers on the sidelines and contract buyers more focused on July with prices resetting.”

“Our short-term forecast is strong, best YTD.”

Note: Demand, lead times, and prices are based on the average data from manufacturers and steel service centers that participate in SMU’s market trends analysis surveys. Our demand and lead times do not predict prices but are leading indicators of overall market dynamics and potential pricing dynamics. Look to your mill rep for actual lead times and prices.