Plate

March 12, 2024

SMU price ranges: Sheet downturn pauses, plate still subdued

Written by David Schollaert

Sheet and plate prices were mostly flat this week – largely in response to the mill price blitz from last week – pausing the downtrend they’d been on for the better part of 2024.

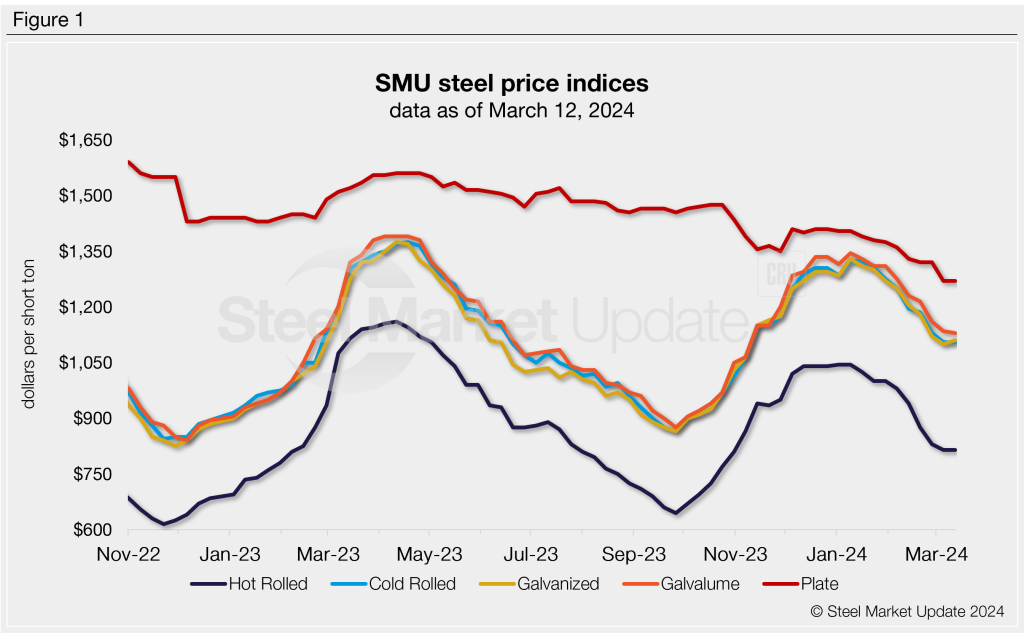

SMU’s hot-rolled (HR) coil price remains at $815 per short ton (st) on average, unchanged from last week, and down $230/st from the beginning of the year. While hot band was flat on average w/w, we did see shifts to the low end and high end of the range.

Prices for cold-rolled (CR) and tandem products saw similar dynamics week over week (w/w). SMU’s CR price is at $1,105/st on average (flat w/w). Our galvanized base price is at $1,110/st on average (+$10/st w/w). And our Galvalume price stands at $1,130/st on average (-$5/st w/w).

Reviews are mixed right now. While some have seen buyers looking to cover their pre-announcement volumes, others note a lack of buying and lower scrap prices as deterrents to price balance or gains in the near term.

Some market sources noted a rush of buyers trying to secure tons negotiated before the price announcements led to an influx of orders, keeping some mills from quoting for the time being.

“They’re not sure about pricing and availability for April ship,” an OEM executive said, “It would not be a surprise to see a new round of price increase announcements in the very near future.”

But while a wave of spring maintenance outages at domestic mills and last week’s repeated tag notices could thwart the price slide and potentially prop them up, decreased demand and lower scrap tags – roughly $50 per gross ton lower this month vs. February – could continue to apply downward pressure.

“Mills are playing games with published prices vs. actual transactions,” said a service center executive. “Demand seems to be getting worse and not better even though we are entering spring season.”

“We have a ways to go before the bottom is determined,” another source said. “Could be a long, hot spring and summer for the plate market as well as most carbon steel products. I think they have driven most buyers to the sidelines for the foreseeable future.”

Plate prices were also unchanged, largely coming to a standstill since Nucor’s publicly announced $90/st plate price cut at the end of February.

SMU’s plate price now stands at $1,270/st on average, unchanged from last week but down $135/st from the beginning of the year.

Our sheet momentum indicators continue to point upward based on strength in pricing for tandem products. But we will watch for any signs of prices plateauing in the new year. Our plate price momentum indicator remains in neutral until we see more consistent and substantial gains.

SMU’s sheet price momentum indicators have switched from lower to neutral because of last week’s mill price notices – meaning we’re unsure how prices will move over the next 30 days. Our plate price momentum remains pointing down, in line with market inputs and Nucor’s latest plate price cut.

Hot-rolled coil

The SMU price range is $790–840/st, with an average of $815/st FOB mill, east of the Rockies. The bottom end of our range was up $10/st vs. one week ago, while the top end of our range was down $10/st w/w. Our overall average is flat from last week. Our price momentum indicator for HRC shifted lower to neutral, meaning SMU is unsure where prices will move over the next 30 days.

Hot rolled lead times: 3–6 weeks

Cold-rolled coil

The SMU price range is $1,020–1,190/st, with an average of $1,105/st FOB mill, east of the Rockies. The lower end and the top end of our range were flat vs. the prior week. As a result, our overall average is unchanged from last week. Our price momentum indicator for CRC shifted lower to neutral, meaning SMU is unsure where prices will move over the next 30 days.

Cold rolled lead times: 5-9 weeks

Galvanized coil

The SMU price range is $1,040–1,180/st, with an average of $1,110/st FOB mill, east of the Rockies. The lower end and the top of our range were up $10/st vs. the prior week. Thus, our overall average is $10/st higher w/w. Our price momentum indicator for galvanized shifted lower to neutral, meaning SMU is unsure where prices will move over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,137–1,277/st with an average of $1,207/st FOB mill, east of the Rockies.

Galvanized lead times: 5–10 weeks

Galvalume coil

The SMU price range is $1,080–1,180/st, with an average of $1,130/st FOB mill, east of the Rockies. The lower end of our range was $20/st lower, while the top end of our range was up $10/st from the prior week. Our overall average was down $5/st when compared to the previous week. Our price momentum indicator for Galvalume shifted lower to neutral, meaning SMU is unsure where prices will move over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,374–1,474/st with an average of $1,424/st FOB mill, east of the Rockies.

Galvalume lead times: 6-9 weeks

Plate

The SMU price range is $1,250–1,290/st, with an average of $1,270/st FOB mill. The lower end of our range was up $10/st vs. the prior week, while the top end of our range was $10/st lower w/w. Our overall average is flat vs. one week ago. Our price momentum indicator for plate remains lower, meaning SMU expects prices will move lower over the next 30 days.

Plate lead times: 4-7 weeks

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.