Prices

February 20, 2024

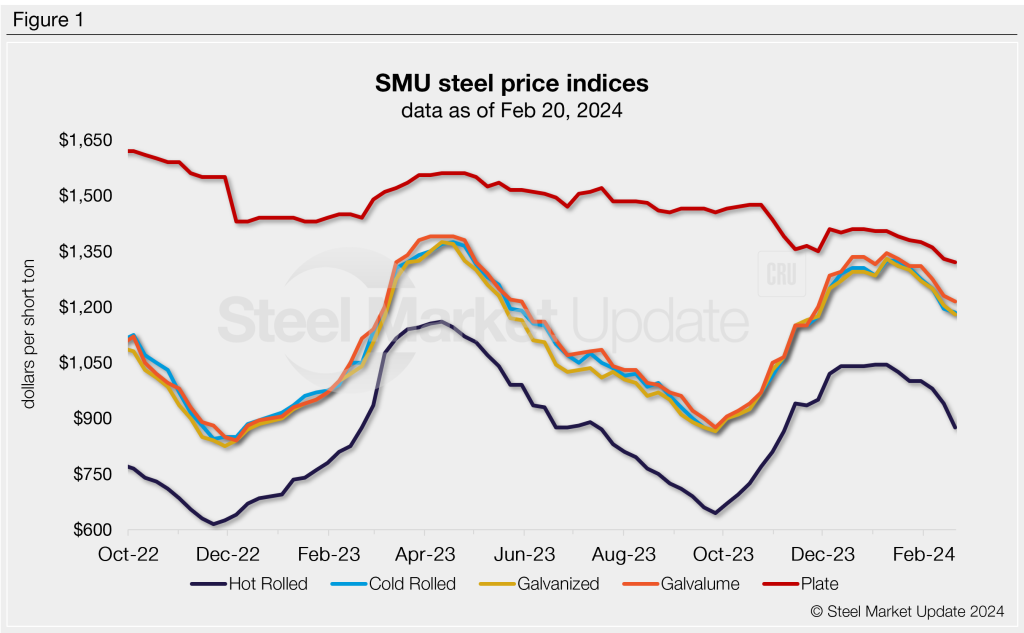

SMU price ranges: HR falls below $900/st as market seeks floor

Written by David Schollaert & Michael Cowden

US hot-rolled (HR) coil prices have fallen below $900 per short ton (st) on average for the first time since early November.

SMU’s HR price stands at $875/st on average, down $65/st from a week ago and down $170/st from the beginning of the year.

We haven’t recorded such a steep week-over-week (w/w) decline since June 2022, when prices rapidly retreated following a spike earlier in the year stemming from Russia’s invasion of Ukraine.

There is no obvious external shock that sparked the decline this time. Instead, it appears to be a collection of smaller issues – higher service center inventories, weaker-than-expected scrap prices, increased import competition, and a normalization of US prices with world prices.

Cold-rolled (CR) and coated prices held up somewhat better but still fell. SMU’s CR price stands at $1,185/st on average, down $10/st from a week ago. Galvanized base prices are at $1,180/st, down $25/st from last week. And Galvalume prices are at $1,215/st, down $15/st from a week ago.

The result: Spreads between HR and CR/coated base prices are more than $300/st on average – much higher than the $200/st spread the market has become accustomed to in recent years. Several sources said they expect that spread to narrow as prices for tandem products follow HR lower on a lag.

Plate, meanwhile, stands at $1,320/st on average, down $10/st from last week.

SMU’s price momentum indicators for all sheet and plate products continue to point lower.

Hot-rolled coil

The SMU price range is $820–930/st, with an average of $875/st FOB mill, east of the Rockies. The bottom end of our range was down $80 per st vs. one week ago, while the top end of our range was down $50/st w/w. Our overall average is $65/st lower from last week. Our price momentum indicator for HRC remains lower, meaning SMU expects prices will move lower over the next 30 days.

Hot rolled lead times: 3–8 weeks

Cold-rolled coil

The SMU price range is $1,120–1,250/st, with an average of $1,185/st FOB mill, east of the Rockies. The lower end of our range was flat vs. the prior week, while the top end of our range was down $20/st. Our overall average is down $10/st from last week. Our price momentum indicator for CRC remains lower, meaning SMU expects prices will move lower over the next 30 days.

Cold rolled lead times: 6–9 weeks

Galvanized coil

The SMU price range is $1,110–1,250/st, with an average of $1,180/st FOB mill, east of the Rockies. The lower end of our range was down $30/st vs. the prior week, while the top end of our range was $20/st lower w/w. Our overall average is $25/st lower than the week prior. Our price momentum indicator for galvanized remains lower, meaning SMU expects prices will move lower over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,207–1,347/st with an average of $1,277/st FOB mill, east of the Rockies.

Galvanized lead times: 5–10 weeks

Galvalume coil

The SMU price range is $1,160–1,270/st, with an average of $1,215/st FOB mill, east of the Rockies. The lower end of our range was flat w/w, while the top end of our range was down 30/st from the prior week. Our overall average was down $15/st when compared to the previous week. Our price momentum indicator for Galvalume remains lower, meaning SMU expects prices will move lower over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,454–1,564/st with an average of $1,509/st FOB mill, east of the Rockies.

Galvalume lead times: 7–8 weeks

Plate

The SMU price range is $1,260–1,380/st, with an average of $1,320/st FOB mill. The lower end of our range was down $20/st vs. the week prior, while the top end of our range was flat w/w. Our overall average is down $10/st vs. one week ago. Our price momentum indicator for plate remains lower, meaning SMU expects prices will move lower over the next 30 days.

Plate lead times: 4-7 weeks

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert