Market Data

January 18, 2024

SMU survey: Steel mill lead times mostly slipping

Written by Laura Miller

The slipping lead times for flat-rolled steel were not just due to the holiday slowdown, it seems, as production times for four out of five products contracted again this week.

Meanwhile, galvanized lead times were flat compared to two weeks ago. Buyers of galvanized sheet have reported supply issues to SMU.

With prices declining and lead times slipping, many buyers in SMU’s survey this week said they feel a peak has been reached in this market cycle, barring some unforeseen event.

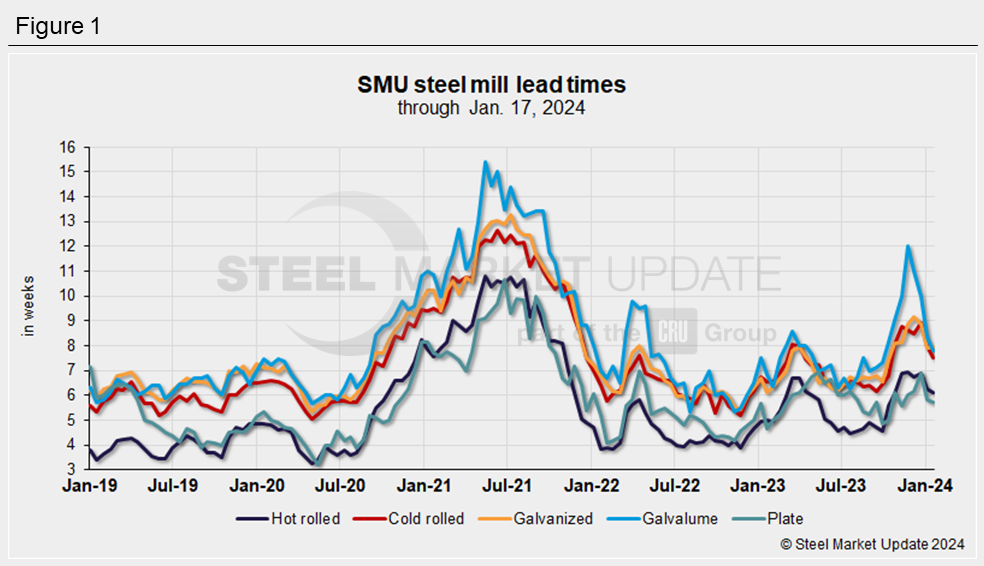

Steel mill lead times this week

Buyers of hot-rolled coil this week reported a lead time range of 4 to 8 weeks. The average of 6.14 weeks was 0.12 weeks shorter than the 6.26-week lead time reported two weeks ago. At this time last year, HRC lead times were just under 5.0 weeks.

In this week’s market check, lead times for cold-rolled coil were between 6 and 10 weeks. The average of 7.53 weeks is almost half a week shorter than the 8.00 week lead time reported during the week of Jan. 3. CRC lead times were nearly a week shorter at this time last year.

Buyers reported lead times for galvanized sheet ranging from 5 to 11 weeks. This week’s average of 7.95 weeks was comparable to the 7.93-week lead time in our last market check. Galvanized lead times are extended by almost two weeks compared to this time last year, when they were 6.1 weeks on average.

Galvalume lead times contracted for the fourth consecutive market check with a 5 to 11-week range. The average of 7.80 weeks reported this week is down by 0.53 weeks from two weeks prior and down from a recent high of 12.00 weeks at the end of November. Lead times for Galvalume are still extended compared to the same time in 2023, when they averaged 6.83 weeks.

Note that our data for Galvalume is more volatile due to the smaller sample and market size. If you are a buyer of Galvalume and would like to share your lead time and pricing data with SMU, please contact david@steelmarketupdate.com.

Plate lead times were reported by buyers in this week’s survey to be between 4 and 8 weeks. The average of 5.73 weeks contracted from the 5.8 weeks reported during the week of Jan. 3 and the recent high of 6.89 weeks during the week of Dec. 20.

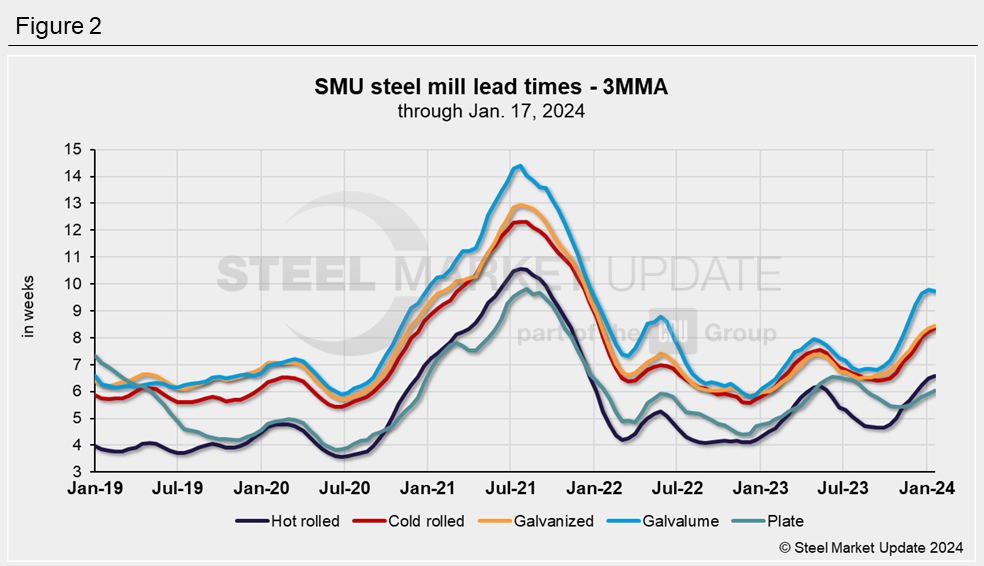

3MMA lead times

To smooth out the variability in SMU’s biweekly readings, let’s look at lead times on a three-month moving average (3MMA) basis.

The 3MMA lead times for hot-rolled, cold-rolled, and galvanized sheet pushed out this week vs. two weeks earlier to 6.57 weeks, 8.35 weeks, and 8.44 weeks, respectively. The 3MMA of Galvalume lead times contracted slightly from 9.79 weeks two weeks ago to 9.73 weeks this week.

For plate, the 3MMA of lead times extended slightly, from 5.93 weeks in the Jan. 3 market check to 6.03 weeks. This is the first time plate’s 3MMA lead time has been above 6 weeks since mid-August.

SMU’s survey results

When asked if lead times will be extending, flat, or contracting two months from now, buyers in SMU’s survey this week were again split between flat (45%) and contracting (42%). Still, 13% said they will be extending.

Here are a few comments from survey respondents on that same question:

“I am saying flat because that will be mid-March, and demand will recover seasonally.”

“Mills can’t keep pushing out lead time if the price is falling.”

“With prices falling, lead times will come down.”

“I think domestic lead times and imports will be two keys to watch as we potentially start a reversal.”

“They will slightly contract in the next 2-3 weeks but then will extend again.”

“Again, being out of sync with global markets puts caution into inventory decisions.”

“Lower demand and more offshore is arriving.”

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.