Prices

January 2, 2024

SMU price ranges: Sheet mixed as market awaits post-holiday direction

Written by David Schollaert & Michael Cowden

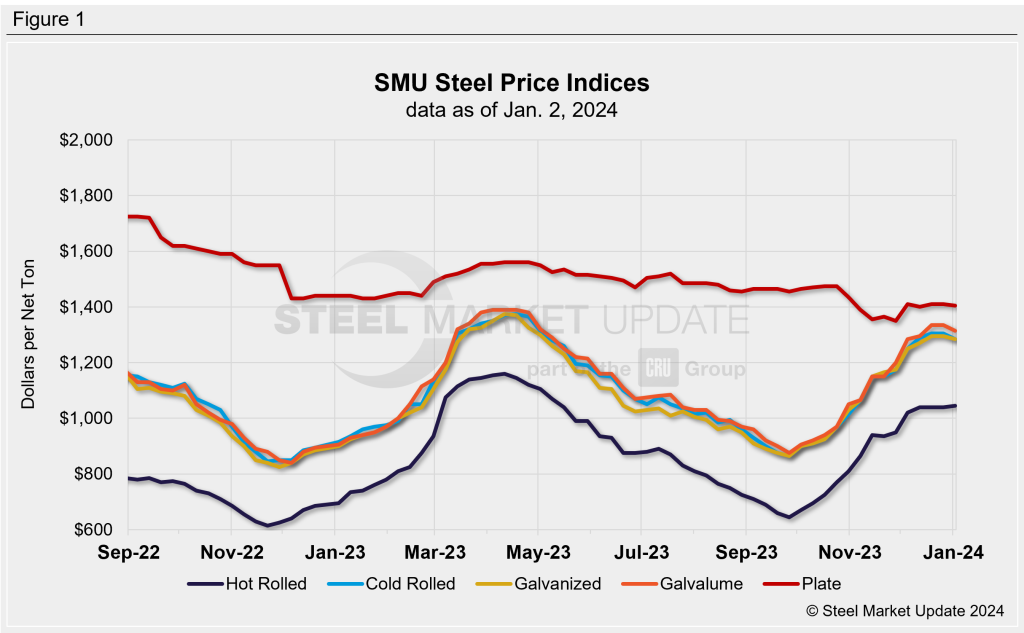

Sheet prices were mixed in SMU’s first assessment of the market in the New Year. Hot-rolled coil (HRC) prices inched up modestly while prices for cold-rolled coil (CRC) and coated products slipped.

SMU’s HRC price now stands at $1,045 per net ton on average, up $5 per ton from our last assessment in December. CRC and galvanized base prices both average $1,285 per ton. That’s down $20 per ton for CRC and down $10 per ton for galv. Galvalume averages $1,315 per ton, also down $20 per ton from our prior assessment.

Plate prices, meanwhile, average $1,405 per ton on, down $5 per ton for our last assessment.

Market commentary was also mixed. Some sources voiced concern about sheet lead times not extending or extending only modestly at one major sheet mill. They said that could point toward domestic supply increasing and prices plateauing.

Some also noted that foreign CRC from Southeast Asia is cheaper than domestic HR. That material might not arrive until Q2, a lead time that might be too long for some domestic buyers. The price might still appeal to buyers along the coasts, something that could chip away at domestic mill order books.

But others pointed to an uptick in CME HRC futures for February and March as evidence that a feared January inflection downward might not happen. Some suggested that another round of mill price hikes might be imminent. Even if they don’t succeed in raising prices, they should at least stabilize them, these sources said.

Recall that we also saw mixed directions in sheet prices in our last check of the market in December. We have therefore adjusted our sheet price momentum indicator to neutral. That’s the first time since Oct. 3 that it has not been at higher. Our plate price momentum indicator is also at neutral.

Hot-rolled coil

The SMU price range is $990–1,100 per net ton, with an average of $1,045 per ton FOB mill, east of the Rockies. The bottom end of our range was up $10 per ton, while the top end of our range was unchanged vs. one week ago. Our overall average is up $5 per ton week on week (WoW). Our price momentum indicator for HRC moved from higher to neutral, meaning SMU is unsure of the direction prices will move over the next 30 days.

Hot rolled lead times: 6–8 weeks

Cold-rolled coil

The SMU price range is $1,240–1,330 per net ton, with an average of $1,285 per ton FOB mill, east of the Rockies. The lower end of our range was down $20 per ton vs. the prior week, while the top end of our range was also down $20 per ton. Our overall average is down $20 per ton vs. the week prior. Our price momentum indicator for CRC moved from higher to neutral, meaning SMU is unsure of the direction prices will move over the next 30 days.

Cold rolled lead times: 6–12 weeks

Galvanized coil

The SMU price range is $1,240-1,330 per ton, with an average of $1,285 per ton FOB mill, east of the Rockies. The lower end of our range was down $20 per ton vs. the prior week, while the top end of our range was unchanged. Our overall average is down $10 per ton vs. the week prior. Our price momentum indicator for galvanized moved from higher to neutral, meaning SMU is unsure of the direction prices will move over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,337–1,427 per ton with an average of $1,382 per ton FOB mill, east of the Rockies.

Galvanized lead times: 6-11 weeks

Galvalume coil

The SMU price range is $1,280–1,350 per net ton, with an average of $1,315 per ton FOB mill, east of the Rockies. The lower end of our range was down $20 per ton vs. the prior week, while the top end of our range was also down $20 per ton. Thus our overall average is down $20 per ton vs. the week prior. Our price momentum indicator for Galvalume moved from higher to neutral, meaning SMU is unsure of the direction prices will move over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,574–1,644 per ton with an average of $1,609 per ton FOB mill, east of the Rockies.

Galvalume lead times: 6-15 weeks

Plate

The SMU price range is $1,370–1,440 per net ton, with an average of $1,405 per ton FOB mill. The lower end of our range was unchanged WoW, while the top end of our range was $10 per ton higher. Our overall average is down $5 per ton vs. one week ago. Our price momentum indicator for plate moved from higher to neutral, meaning SMU is unsure of the direction prices will move over the next 30 days.

Plate lead times: 4-7 weeks

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert