Market Data

December 21, 2023

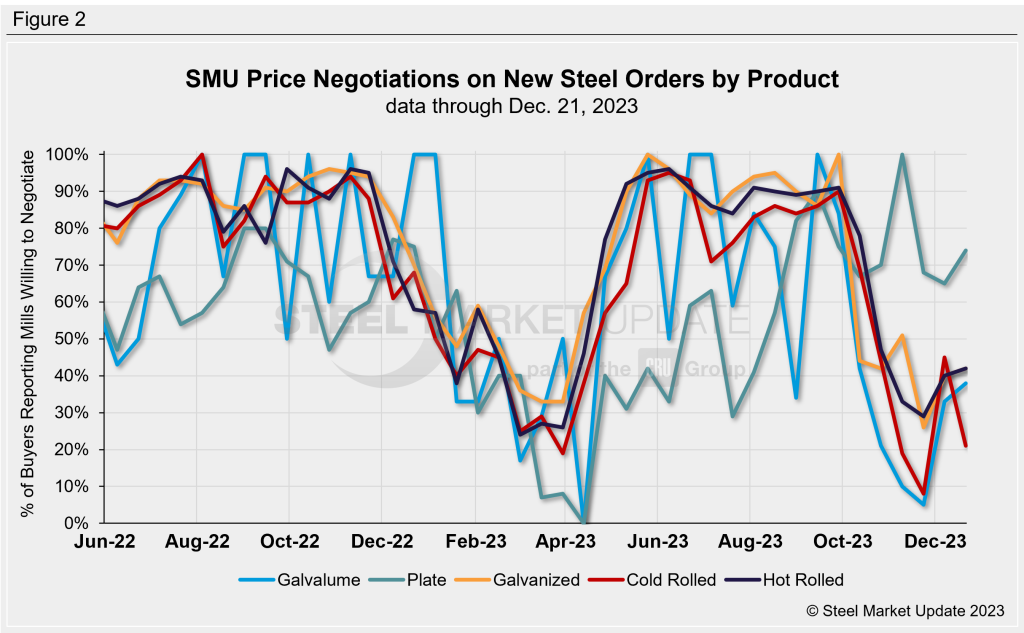

SMU survey: Mills more willing to negotiate price on all products - except cold rolled

Written by Ethan Bernard

Almost all of the products SMU surveys notched an increase in the percentage of buyers saying mills were willing to negotiate spot pricing. The lone exception was cold rolled, according to our most recent survey data.

The negotiation rate for cold rolled tumbled 24 percentage points to 21% vs. 45% two weeks earlier. Meanwhile, steel plate’s mill negotiation rate jumped nine percentage points to 74% in the same comparison.

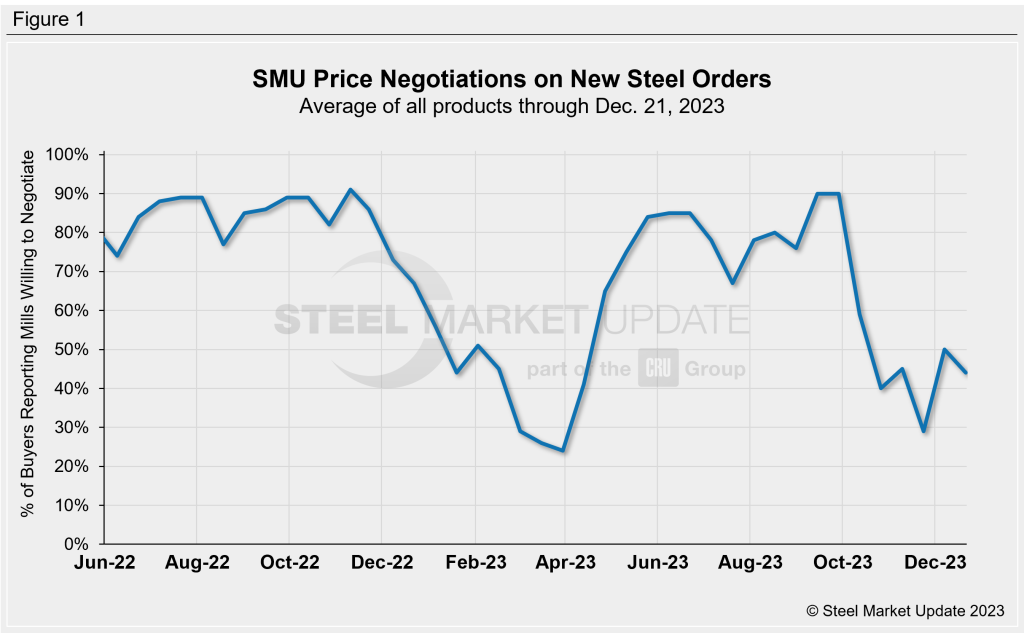

Every two weeks, SMU asks steel buyers whether domestic mills are willing to negotiate lower spot pricing on new orders. This week, 44% of participants surveyed by SMU reported mills were willing to negotiate prices on new orders, down from 50% from two weeks prior (Figure 1). The final reading of the year marks the lowest point since the end of October.

Figure 2 below shows negotiation rates by product. Hot rolled’s rate rose to 42% of buyers saying mills were willing to talk price, up from 40% at the previous market check. Galvanized also increased two percentage points to 42%. And Galvalume increased five percentage points to 38%. We have averaged Galvalume with the previous market check because of fewer market participants and to reduce volatility.

Here’s what some survey respondents had to say:

“Yes, we have secured tons (on hot rolled) well below published prices.”

“Extremely limited spot tons for Galvalume.”

“Sales reps are following up more quotes (on plate) lately. Therefore, business is not as robust as hoped.”

“We haven’t had any meaningful conversations on (hot rolled) pricing, but we have had several reps reach out wanting to engage about tons.”

Note: SMU surveys active steel buyers every other week to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website.