Prices

September 26, 2023

SMU Price Ranges: Sheet Declines Moderate – Meaning or Noise?

Written by David Schollaert & Michael Cowden

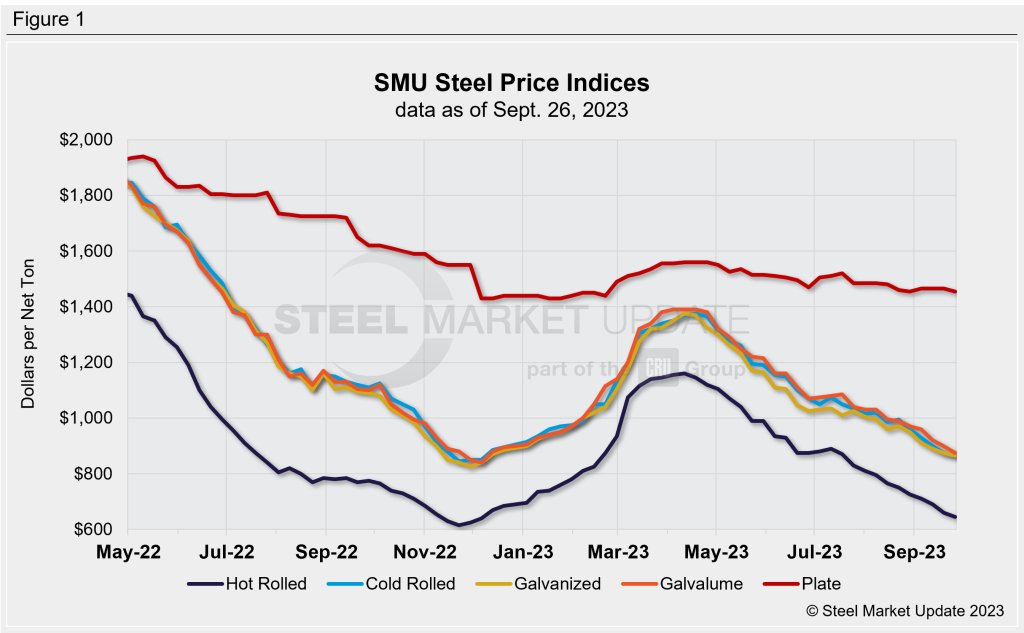

Hot-rolled coil prices were down again this week, continuing a streak of week-over-week (WoW) declines that began in early/mid-July.

Recall that’s when a round of price hikes announced in June faltered after briefly stabilizing the market.

While HRC prices slipped, the $15-per-ton (0.5 per cwt) w/w decline SMU recorded this week was modestly less than the ~$25-per-ton w/w declines we’d averaged previously.

Take a look at SMU’s pricing tool. You’ll see it was a similar story for cold-rolled and galvanized base prices, which were both down $10 per ton w/w. Cold-rolled and galvanized WoW declines had been averaging ~$15-20 per ton previously.

Some market participants will tell you that those changes are significant and potential evidence of a sheet market nearing a bottom.

They might tell you that lower inventories, uncompetitive imports, and mostly steady demand outside of automotive will support a new floor. They might also note that capacity has been tightened by U.S. Steel idling a blast furnace, by fall maintenance outages (some of which have been extended), and by certain EAF mills quietly ratcheting back capacity.

Other sources will tell you that it’s just noise. They might tell you that it’s hard to handicap prices without knowing how long the UAW strike might last and how many assembly plants it might impact. Both of those factors are unknows as of now.

All told, however, sheet sentiment was more positive this week than in prior weeks. That was not the case in plate, where prices slipped $10 per ton and where sentiment soured.

SMU is in the meantime keeping its price momentum indicators pointed lower. While there is talk of a price bottom in sheet, we will not move our sheet price indicator to neutral until we see more evidence of a stable floor.

Hot-Rolled Coil

The SMU price range is $600–690 per net ton ($30.00–34.50 per cwt), with an average of $645 per ton ($32.25 per cwt) FOB mill, east of the Rockies. Both the bottom end of our range decreased $20 per ton vs. one week ago, while the top end of our range was $10 per ton lower WoW. As a result, our overall average is $15 per ton lower compared to the prior week. Our price momentum indicator for hot-rolled coil is still pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Hot-Rolled Lead Times: 3–7 weeks

Cold-Rolled Coil

The SMU price range is $830–900 per net ton ($41.50–45.00 per cwt), with an average of $865 per ton ($43.25 per cwt) FOB mill, east of the Rockies. The lower end of our range was unchanged WoW, while the top end was $20 per ton lower compared to a week ago. Our overall average is down $10 per ton WoW. Our price momentum indicator on cold-rolled coil is still pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Cold-Rolled Lead Times: 5–8 weeks

Galvanized Coil

The SMU price range is $830–900 per net ton ($41.50–45.00 per cwt), with an average of $865 per ton ($43.25 per cwt) FOB mill, east of the Rockies. The lower end and top end of our range were down $10 per ton vs. last week. As a result, our overall average is down $10 per ton vs. the prior week. Our price momentum indicator on galvanized steel is pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $927–997 per ton with an average of $962 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-9 weeks

Galvalume Coil

The SMU price range is $850–900 per net ton ($42.50–45.00 per cwt), with an average of $875 per ton ($43.75 per cwt) FOB mill, east of the Rockies. The lower end of our range was down $10 per ton vs. last week, while the top end of the range was $40 per ton lower WoW. Our overall average was down $25 per ton compared to one week ago. Our price momentum indicator on Galvalume steel is still pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,144–1,194 per ton with an average of $1,169 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 6–8 weeks

Plate

The SMU price range is $1,390–1,520 per net ton ($69.50–76.00 per cwt), with an average of $1,455 per ton ($72.75 per cwt) FOB mill. Both our lower end and top end of our range were down $10 per ton compared to the week prior. Thus, our overall average is down $10 per ton vs. one week ago. Our price momentum indicator on steel plate shifted to lower from neutral, meaning SMU expects prices will decline more over the next 30 days.

Plate Lead Times: 3–8 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert