Prices

September 12, 2023

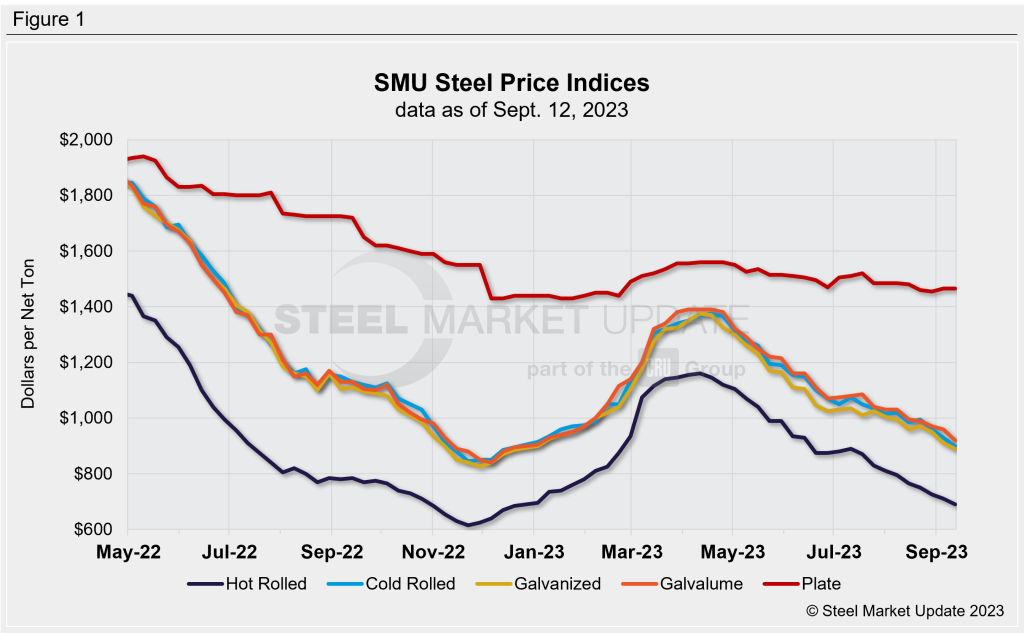

SMU Price Ranges: Sheet Slips Again on UAW Strike Fears

Written by David Schollaert & Michael Cowden

Sheet prices fell across the board ahead of what many market participants predict will be a strike by the United Auto Workers (UAW) later this week.

Some sources said a deal might be reached. But others maintained that the main question was whether the strike would be brief and against one automaker, or extended and potentially against all three Detroit-area car and truck producers.

SMU’s average hot-rolled coil (HRC) price slipped to $690 per ton ($34.50 per cwt), down $20 per ton from last week, and marking the lowest point for HRC prices so far this year.

HRC was last below current levels in late December 2022, before an unexpected production stop at Mexican steelmaker AHSMA – and aggressive price increases by US mills – sent tags soaring in Q1’23.

It was a similar story for value-added products.

Cold-rolled stood at $900 per ton on average, down $30 per ton week on week (WoW), and marking its lowest point since late December 2022. Galvanized weighed in at $890 per ton, down $20 per ton WoW and its lowest point since late last year. We recorded Galvalume at $920 per ton, down $40 per ton WoW.

Our average plate price is unchanged. But the high end of our range is at $1,530 per ton, down from $1,570 per ton last month following Nucor’s $40-per-ton price decrease.

The price momentum indicators for all our sheet and plate products continue to point lower.

Hot-Rolled Coil

The SMU price range is $650–730 per net ton ($32.50–36.50 per cwt), with an average of $690 per ton ($34.50 per cwt) FOB mill, east of the Rockies. The bottom end of our range declined $30 per ton vs. one week ago, while the top end of our range was $10 per ton lower week on week (WoW). Our overall average is $20 per ton lower compared to the prior week. Our price momentum indicator for hot-rolled coil is still pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Hot-Rolled Lead Times: 3–7 weeks

Cold-Rolled Coil

The SMU price range is $880–920 per net ton ($44.00–46.00 per cwt), with an average of $900 per ton ($45.00 per cwt) FOB mill, east of the Rockies. The lower end of our range was down $20 per ton WoW, while the top end was down $40 per ton compared to a week ago. Our overall average is down $30 per ton WoW. Our price momentum indicator on cold-rolled coil is still pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Cold-Rolled Lead Times: 5–8 weeks

Galvanized Coil

The SMU price range is $860–920 per net ton ($43.00–46.00 per cwt), with an average of $890 per ton ($44.50 per cwt) FOB mill, east of the Rockies. The lower end of our range was unchanged vs. last week, while the top end of our range was down $40 per ton compared to one week ago. Our overall average is down $20 per ton vs. the prior week. Our price momentum indicator on galvanized steel is pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $957–1,017 per ton with an average of $987 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-9 weeks

Galvalume Coil

The SMU price range is $860–980 per net ton ($43.00–49.00 per cwt), with an average of $920 per ton ($46.00 per cwt) FOB mill, east of the Rockies. The lower end of our range was down $60 per ton vs. last week, while the top end of the range was $20 per ton lower WoW. Our overall average was down $40 per ton compared to one week ago. Our price momentum indicator on Galvalume steel is still pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,154–1,274 per ton with an average of $1,214 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 6–8 weeks

Plate

The SMU price range is $1,400–1,530 per net ton ($70.00–76.50 per cwt), with an average of $1,465 per ton ($73.25 per cwt) FOB mill. The lower end of our range was unchanged compared to the week prior, while the top end of our range was also sideways vs. last week. Our overall average is unchanged WoW. Our price momentum indicator on steel plate remains at neutral, meaning we are unsure of what direction prices will go over the next 30 days.

Plate Lead Times: 3–8 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert