Overseas

April 14, 2022

Foreign vs. Domestic Hot-Rolled Coil Price Update

Written by Brett Linton

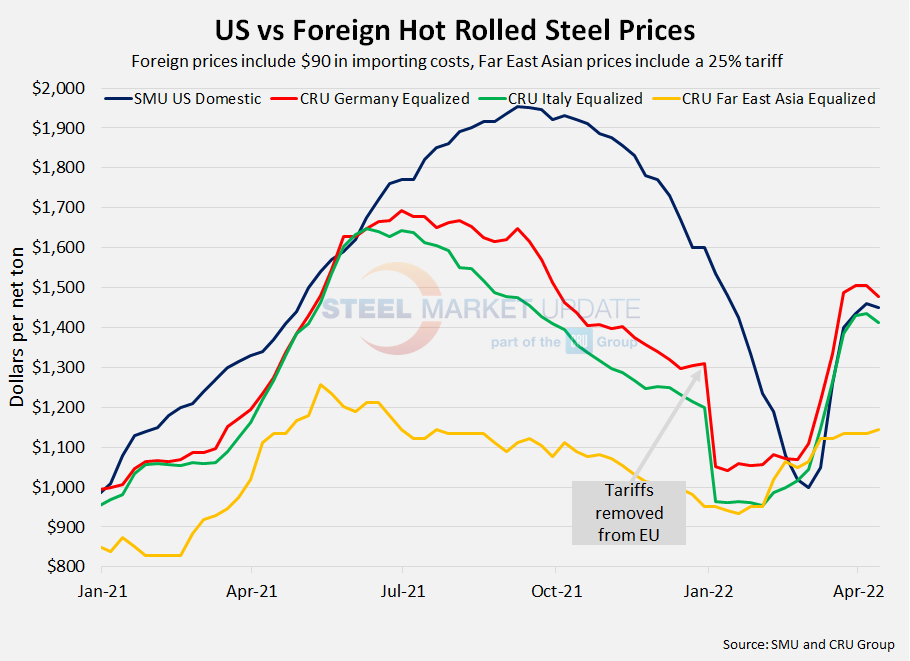

The competitive advantage foreign import prices hold over domestic steel is relatively unchanged from our previous update, with most prices moving just $10-$20 from last week, according to SMU’s latest foreign versus domestic hot-rolled coil (HRC) price comparison. Select foreign HRC prices range from $305 per ton cheaper than domestic prices to $27 per ton more expensive, after taking freight costs, trader margins and tariffs into consideration. Recall that the price differentials between domestic HRC compared to foreign imports had narrowed since peaking last summer, with domestic prices briefly holding a competitive edge in late February through mid-March.

The following calculation is used by Steel Market Update to identify the theoretical spread between foreign HRC prices (delivered to US ports) and domestic HRC prices (FOB domestic mills). This is only a “theoretical” calculation because freight costs, trader margins, and other costs can fluctuate, ultimately influencing the true market spread. This compares the SMU US HRC weekly index to the CRU HRC weekly indices for Germany, Italy and Far East Asian ports.

![]()

In consideration of freight costs, handling, trader margin, etc., we add $90 per ton to all foreign prices to provide an approximate “CIF US ports price” that can be compared against the SMU US HRC price. Recent spot checks show freight on SE Asian imports into Houston costing between $100-110 per ton and costs on European products between $85-90 per ton. Buyers should use our $90-per-ton figure as a benchmark and adjust up or down to their own shipping and handling costs as necessary.

Note that effective January 1, 2022, the traditional Section 232 tariff no longer applies to most imports from the European Union. It has been replaced by a tariff rate quota (TRQ). Therefore, the German and Italian price comparisons in this analysis no longer include a 25% tariff. SMU still includes the 25% S232 tariff on foreign prices from other countries. We do not include any antidumping (AD) or countervailing duties (CVD) in this analysis.

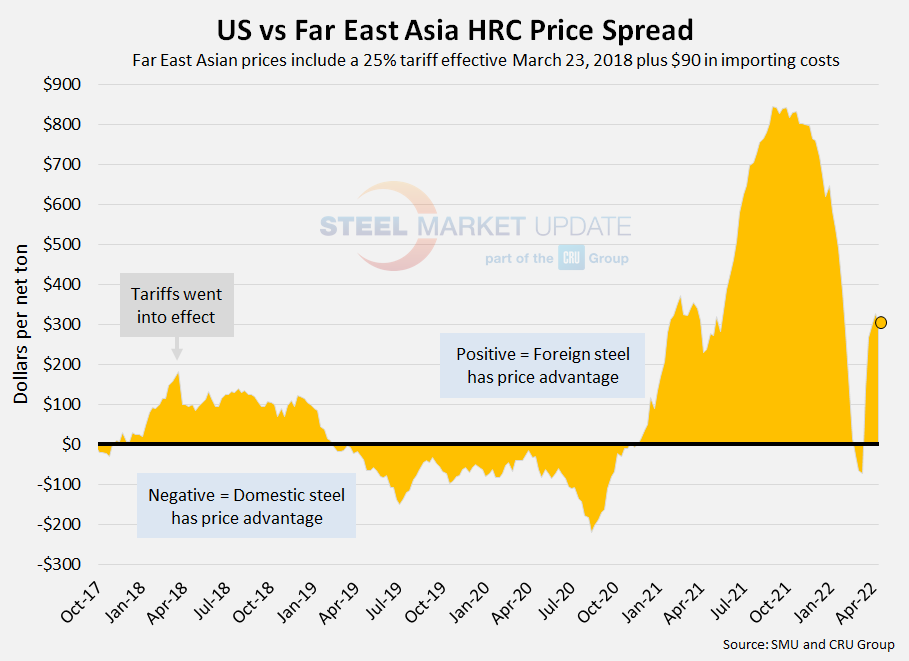

Far East Asian HRC (East and Southeast Ports)

As of Wednesday, April 13, the CRU Far East Asian HRC price rose $9 per ton over the previous week to $844 per net ton ($930 per metric ton), up $18 per ton from one month prior. Adding a 25% tariff and $90 per ton in estimated import costs, the delivered price of Far East Asian HRC to the US is $1,145 per ton. The latest SMU HRC price average is $1,450 per ton, down $10 from one week prior, but up $190 from one month ago. Therefore, US-produced HRC is now theoretically $305 per ton more expensive than imported Far East Asian HRC. That differential was $327 per ton last week and $302 per ton two weeks prior. This is the fifth consecutive week foreign steel prices have held this price advantage. We briefly saw the opposite in late February through mid March when domestic HRC was $28-72 per ton cheaper than Far East Asian prices. The largest price spread between these regions was $847 per ton in September 2021, when Far East Asian prices held a considerable advantage.

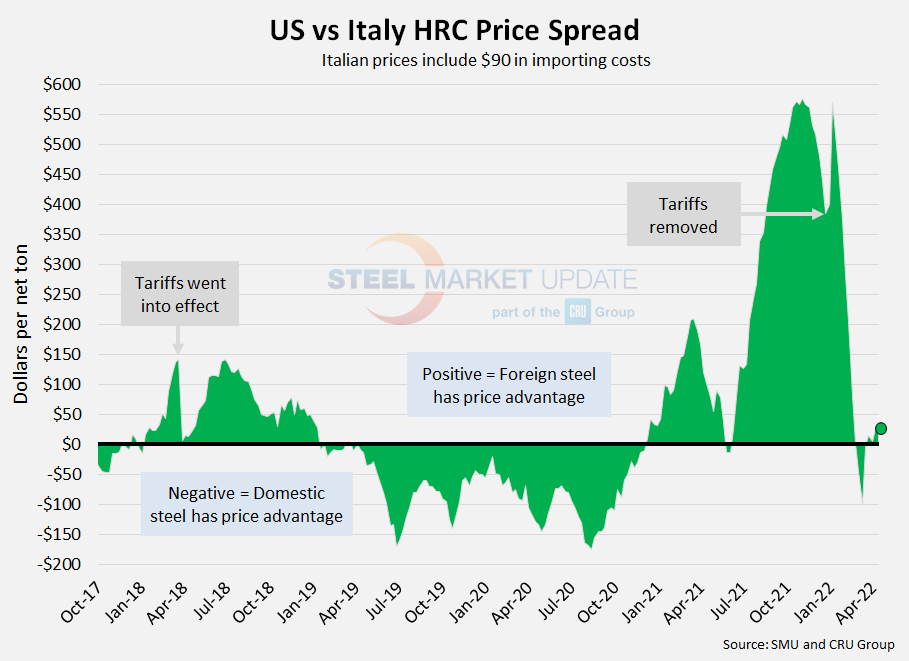

Italian HRC

CRU published Italian HRC prices at $1,323 per net ton ($1,459 per metric ton), down $21 per ton from last week, but up $149 per ton from one month ago. After adding import costs, the delivered price of Italian HRC is approximately $1,413 per ton. Accordingly, domestic HRC is now theoretically $37 per ton more expensive than imported Italian HRC, compared to $26 per ton one week prior and $5 per ton two weeks ago. This is the fourth consecutive week foreign steel prices have held this price advantage. We briefly saw the opposite in the first half of March, when imported Italian HRC offered a theoretical savings of $4-98 per ton. Prior to removal of the 25% Section 232 tariff, the November 2021 spread of $577 per ton was the largest seen in SMU’s data history.

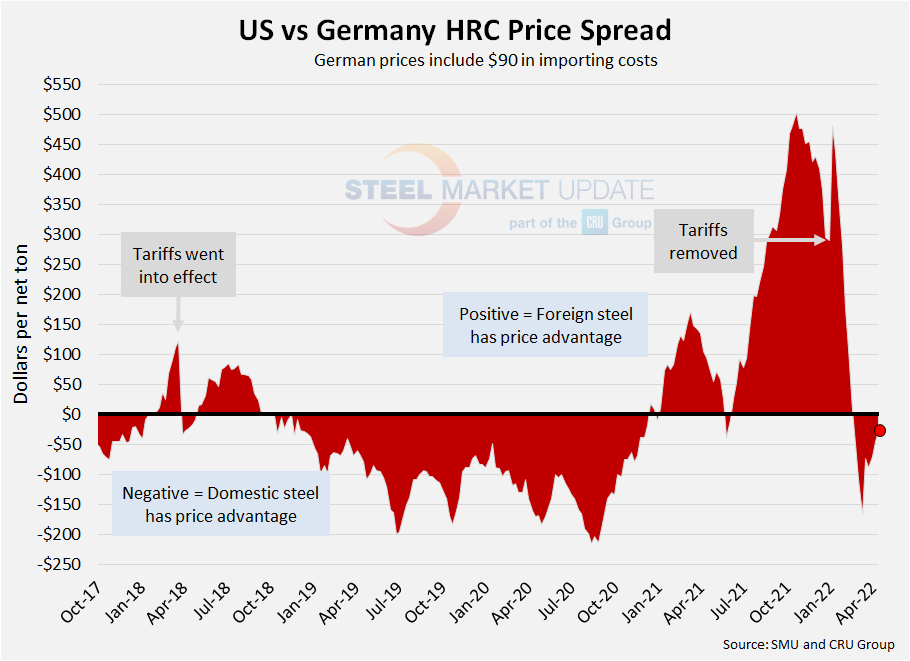

German HRC

The latest CRU German HRC price is $1,387 per net ton ($1,529 per metric ton), down $29 per ton from last week, but up $144 per ton from one month ago. After adding import costs, the delivered price of German HRC is approximately $1,477 per ton. Accordingly, domestic HRC is theoretically $27 per ton cheaper than imported German HRC, down from $46 per ton last week. One month ago, German prices were $74 per ton more expensive than domestic steel. This is the eigth consecutive week that domestic steel prices have held this price advantage. Prior to removal of the 25% tariff, the October 2021 spread of $504 per ton was the largest seen in SMU’s data history.

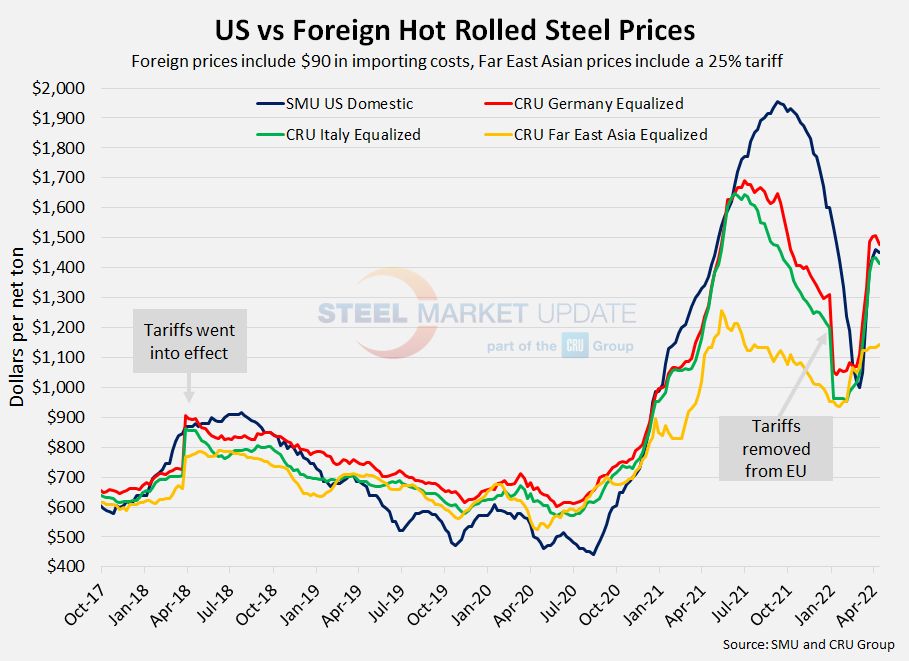

The graph below compares all four price indices and highlights the effective date of the tariffs. Foreign prices are referred to as “equalized,” meaning they have been adjusted to include importing costs (and tariffs in some cases) for a like-for-like comparison against the US price. The second graphic shows the same data but focuses on prices over the last 16 months.

Note: Freight is an important part of the final determination on whether to import foreign steel or buy from a domestic mill supplier. Domestic prices are referenced as FOB the producing mill, while foreign prices are FOB the Port (Houston, NOLA, Savannah, Los Angeles, Camden, etc.). Inland freight, from either a domestic mill or from the port, can dramatically impact the competitiveness of both domestic and foreign steel. When considering lead times, a buyer must take into consideration the momentum of pricing both domestically and in the world markets. In most circumstances (but not all), domestic steel will deliver faster than foreign steel ordered on the same day.

By Brett Linton, Brett@SteelMarkeUpdate.com