Mexico

April 24, 2025

HR Futures: Nascent rally in HRC futures settles above 6-week downtrend

Written by David Feldstein

David Feldstein is the President of Rock Trading Advisors. Rock Trading Advisors is a National Futures Association Member Commodity Trade Advisory. It provides commercial clients with price risk solutions in ferrous, energy, and interest rate derivatives markets.

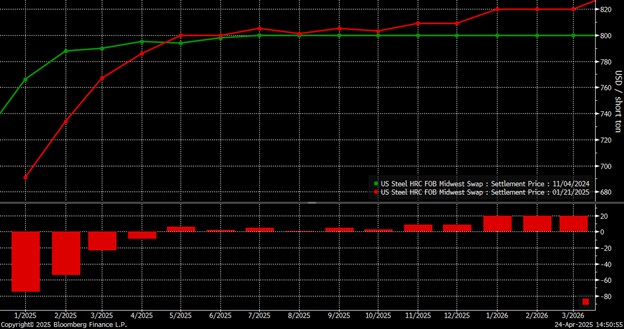

The CME Midwest HRC futures market’s response to Trump’s election and subsequent comments about blanket 25% tariffs on Canada and Mexico was surprisingly counterintuitive.

In fact, from the day before the election until the day after his inauguration, the HRC futures curve declined in the front three months of 2025. During that time, the February future dropped $54 to $734 per short ton (st) and the March future $23 to $767/st. From there, the February future expired up $45 at $779/st and the March future up $167 at $934/st. Given this information, do you think the curve priced in the 25% tariffs on steel?

CME hot-rolled coil futures curve $/st

Frankly, how could they. The announcement on Super Bowl Sunday was a surprise, to say the least. This chart shows the settlements on Feb. 7, the Friday before the Super Bowl, March 4, and today.

The market response to Trump’s 25% tariffs finally occurred as one would expect. At its peak on March 4, the curve had opened into a steep backwardation with increases of $109, $160, $135, and $106, in the months of March through June, respectively, and gains ranging from $44-$73 in the months of the second half.

What is more, the rally was on heavy volume with open interest surging 170,000 tons in roughly five weeks to its highest since January 2022. Open interest is the number of outstanding futures contracts, or tons in this case, across a product’s curve.

What happened after March 4 was rather unexpected. The futures curve from June forward drifted back down on light volume to about where it was before the 25% tariffs were announced. In other words, one could lock in a fixed priced steel purchase at the same price today as they could before the tariffs, but now they know there are 25% steel tariffs! But….that is not happening. Go figure.

CME hot-rolled coil futures curve $/st

Last year, the weekly CRU monitor hit a low of $656/st on July 24: 125% times $656 equals $820. HRC in Asia is trading around $450/st. Add a 25% tariff and shipping costs and you are at roughly $760. So, does this indicate a floor for Midwest HRC in the $760-$820 area?

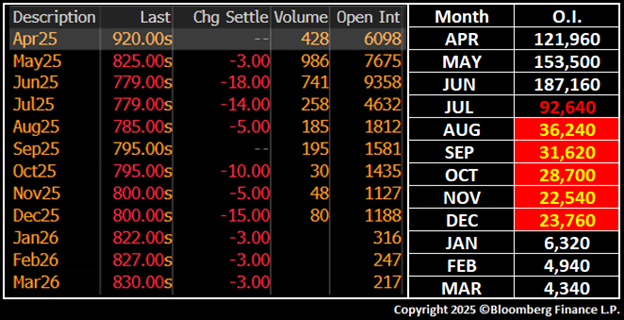

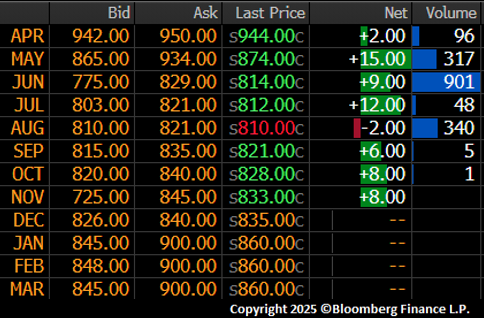

This table shows the settlements and open interest for the Midwest HRC futures curve on April 9. HRC futures were already in oversold territory on the relative strength indicator for four days when the June and July futures started trading below $780 around April 9. They didn’t stay there for long. The futures appeared to have found a floor and have since traded roughly $35 higher in the months of June and July.

CME hot-rolled coil futures curve w/open interest

Here is a question. Were the gains of the past few weeks a dead cat bounce or the start of a new leg to the 2025 rally?

The open interest data in the table above is interesting. Notice the drop-off in open interest from 187,000 tons in June to 92,000 tons in July to 36,000 tons in August. The trend continues in the months after that through December. Note the settlement prices that day of $780 to $800 through year-end.

If buyers used the futures to lock up fixed-priced deals for the second half, then one would expect open interest in those months would be much higher. The conclusion is that buyers have not entered into fixed priced deals at these prices en masse. That leaves us with a number of questions.

- Is this because the buying community writ large expects lower prices, perhaps that the tariffs will be reversed?

- Or is it because the buying community has no orders to back up with fixed-priced deals?

- Or is it because the buying community has procrastinated placing their orders for the third quarter?

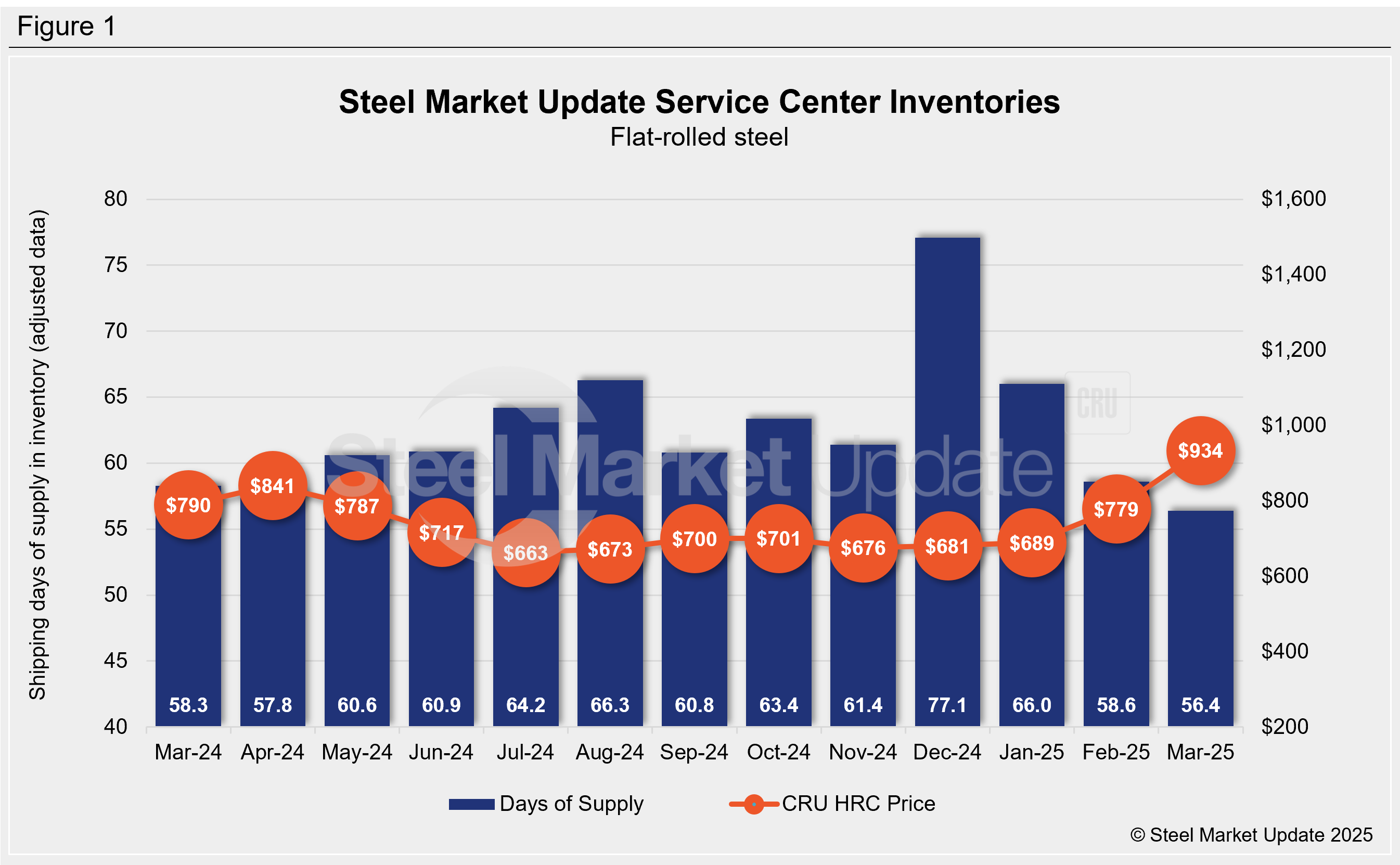

Someday, we might have an answer. However, if it is number three, and there is a large wave of physical purchase orders that are queuing up, then the supply side of the equation is one with 56.4 days of flat rolled inventory, according to the Steel Market Update Service Center Inventories data below. And sharply lower flat rolled imports with March’s flat rolled imports down 177,000 tons, or 18.7%, year over year, according to the US Department of Commerce website.

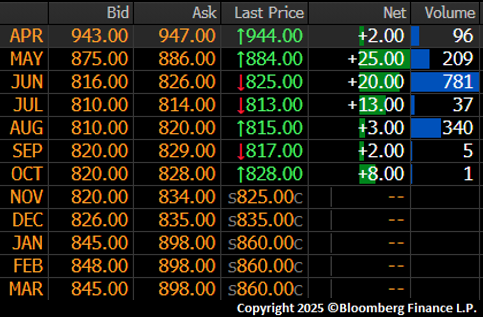

As noted, Midwest HRC futures have been percolating over the past couple of weeks. Today, the market popped with the day’s highs taken from the curve around 11 am CT shown here.

The CME settlement team chose to peel back some of the gains when it posted today’s settlements.

Even still, the May future settled clearly on the other side of its six-week downtrend. With the trend line broken, the May future turning from oversold back toward a more neutral reading and the M.A.C.D. in positive territory, the chart pattern is representing that the answer is that yes, a new leg in the rally has just begun.

May CME Midwest hot-rolled coil future $/st

While that is all well and good, I am obligated to mention that there is downside risk as well with a number of sentiment readings in bearish territory. Moreover, after 25 years of technical analysis, I can confidently say that technical analysis is reliably correct 50% of the time.

So, will this nascent reversal manifest into a new leg of the 2025 rally, or will it fizzle out, proving to be yet another failed rally? Tune in next time.

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Mr. Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.